Trustee Sale: The Fastest Way to Buy Distressed Property Below Market Value

Trustee Sale: The Fastest Way to Buy Distressed Property Below Market Value

TL;DR: A trustee sale is a public auction held by a neutral third party (the trustee) to sell a property that has defaulted on its mortgage. Winning bidders pay the opening bid in cash immediately and receive the property with no financing contingencies. Properties at trustee sales often sell 20-40% below comparable market values, but the process carries significant legal and financial risks that most investors underestimate. DistressIQ aggregates trustee sale dates and opening bid amounts across thousands of counties, so investors can track upcoming auctions without spending hours on county recorder websites.

What Is a Trustee Sale and Why Does It Exist?

A trustee sale is the enforcement mechanism built into every deed of trust (the standard mortgage instrument used in non-judicial foreclosure states, which covers 23 states). When a borrower stops making payments, the lender initiates the foreclosure process, and the trustee, a neutral third party, is legally obligated to sell the property at public auction to recover the outstanding loan balance.

The legal framework varies significantly by state. In the 23 states that use non-judicial foreclosure, the trustee sale happens outside the court system entirely, governed by the deed of trust and state statute. In judicial foreclosure states, the process runs through the courts, and a sheriff or court-appointed officer conducts the sale instead. Texas is a hybrid: lenders use both a non-judicial foreclosure through the deed of trust and a potential judicial process if the non-judicial route fails.

The key point for investors is that the trustee's job is to recover as much of the outstanding loan balance as possible, not to maximize the sale price. This creates an inherent tension. The opening bid at a trustee sale is typically set at the outstanding loan balance plus fees and costs. If no bidder meets that price, the property goes back to the lender. Properties that fail to attract competitive bids are called "REO" (real estate owned) properties and become the lender's inventory to sell through traditional channels, often at significant discounts weeks or months later.

The Trustee Sale Process: Step by Step

Understanding the sequence matters because timing is everything. Investors who show up without knowing the process waste the opportunity or, worse, agree to terms they do not fully understand.

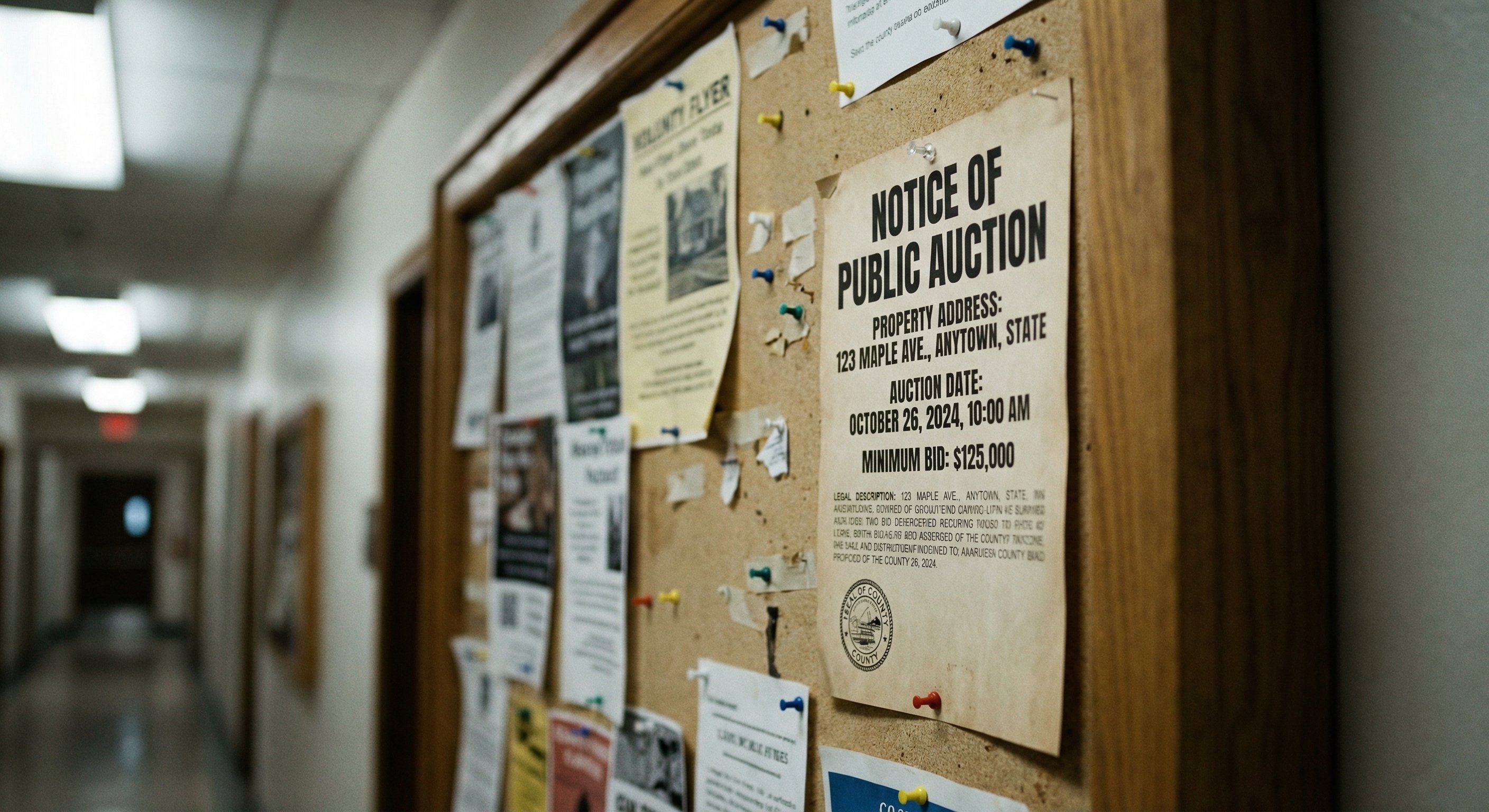

Step 1: Notice of default. The trustee records a notice of default at the county recorder's office, starting the official clock. Most states require 20 to 90 days before the auction date, giving investors time to research.

Step 2: Notice of sale. Once the reinstatement period expires, the trustee records a notice of sale with the auction date, time, and location. This document is public record and the most important research artifact investors need.

Step 3: The auction. Bidders register with the trustee, provide identification, and submit a deposit (typically $5,000 or 5 percent of the opening bid). The auctioneer calls for bids starting at the opening bid amount.

Step 4: Immediate payment. The winning bidder pays the remainder in certified funds immediately after the auction. The trustee issues a deed conveying title.

Step 5: Redemption period (state-dependent). Some states allow the foreclosed borrower to redeem the property after the sale by paying the winning bid plus costs within a defined period. Redemption periods range from 30 days to one year.

Why Properties Sell at a Discount at Trustee Sales

The discount comes down to three factors. First, the opening bid equals the loan balance plus fees, which often exceeds current market value. A property with a $350,000 loan, six missed payments, and $12,000 in accumulated fees has an opening bid around $370,000 against a current market value of $290,000. No conventional buyer bids at that price.

Second, lenders sometimes accept a lower bid rather than carry the asset. In declining markets, holding costs, property management, and opportunity cost of capital may exceed the loss from accepting a reduced price. In strong markets, lenders sometimes bid aggressively to prevent a loss, which means investors in hot markets often find the auction disappointing because the lender outbids them.

Third, properties at trustee sale have typically been vacant for months with deferred maintenance and potential code violations or tax delinquencies that add to the investor's acquisition costs.

Free Weekly Alerts

See What's Distressed in Your Market

Get free weekly alerts — new distressed properties, motivation scores, and hot neighborhoods in your area. Addresses and contact info available inside DistressIQ.

Free forever · No credit card · Unsubscribe anytime

How to Research Trustee Sale Properties Before the Auction

Most investors who lose money at trustee sales do so because they underestimated the property's condition, the encumbrances on title, or the competition. Research prevents these errors.

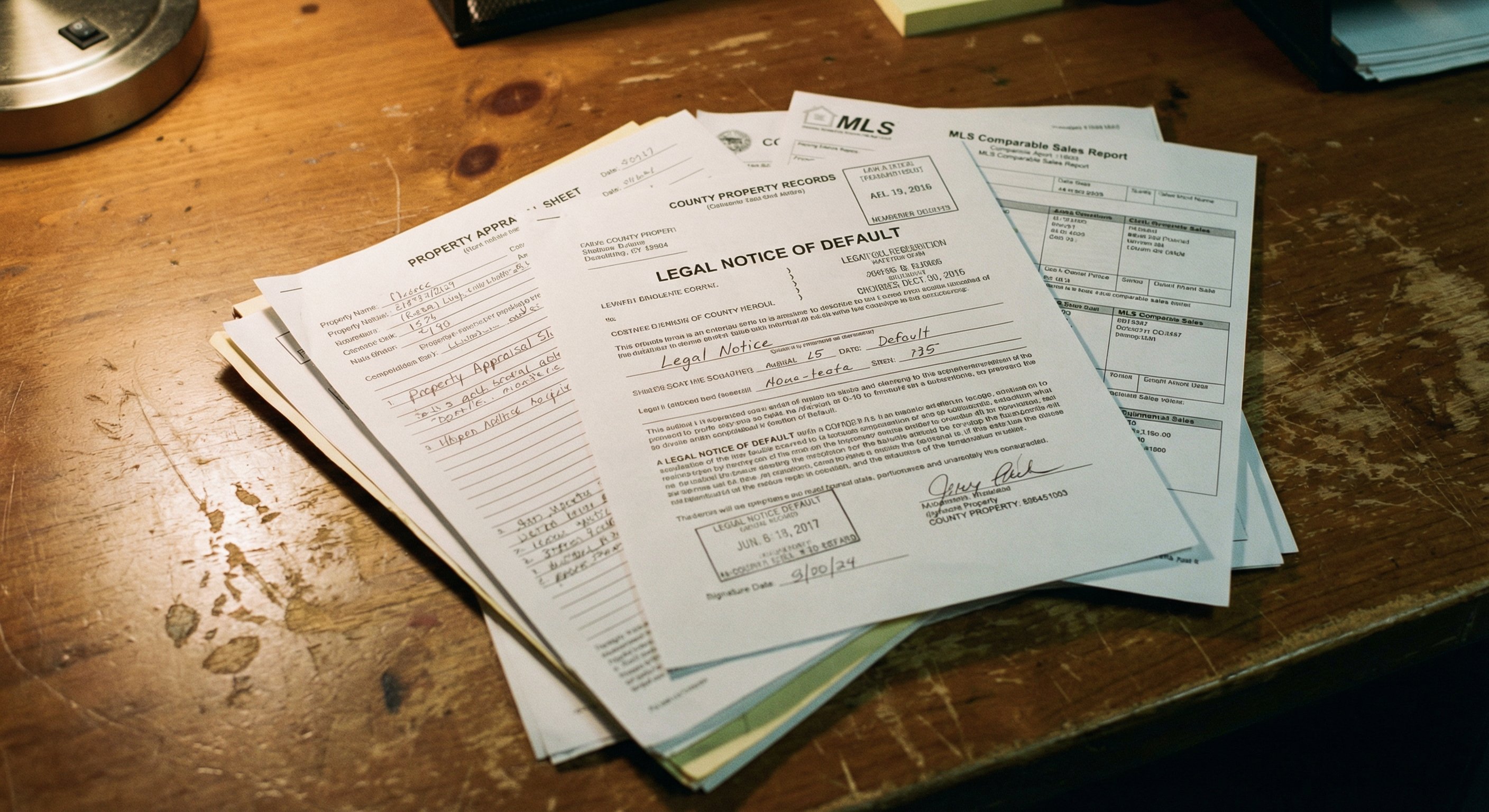

Start with the county recorder. Every notice of default and notice of sale is a public document filed at the county recorder's office. Many counties have digitized these records and offer searchable databases. Others still require in-person visits or written requests. Investors working across multiple counties need a system for tracking these filings.

Get the preliminary title report. Before bidding, order a preliminary title report from a title company. This document shows all liens, encumbrances, and easements recorded against the property. A trustee sale typically clears the senior liens but may leave junior liens (mechanics liens, tax liens, HOA liens) attached to the property.

Verify the occupant situation. Properties that appear vacant may have tenants with leases that survive foreclosure under federal and state law. In California, for example, a bona fide tenant with a lease entered before the notice of default has strong protections. Investors who bid based on "vacant" assumptions and then discover tenants face a costly eviction process.

Understand the opening bid calculation. The opening bid equals the loan balance at the time of the sale plus allowable fees, costs, and accrued interest. Some investors mistakenly assume the opening bid is a fixed amount or that it reflects current market value. It does not. Request the opening bid amount from the trustee directly before the auction.

The Risks That Kill Deals at Trustee Sales

Trustee sales are not for inexperienced investors. The following risks eliminate most retail buyers from ever bidding seriously.

Title risk is the largest and most underestimated. While a trustee's deed gives the winning bidder clear title in most situations, junior lien holders can challenge the sale in court, especially if procedural errors occurred in the notice process. Investors who buy at auction and then spend months and legal fees clearing a clouded title have not found a bargain.

Occupancy risk applies even when the property looks vacant. State and federal law protects certain tenants and, in some states, the former owner for a defined period after the sale. Investors budgeting for a 30-day renovation and then listing the property may find themselves unable to take possession for six months.

Financing risk does not exist at the auction (there is no financing) but becomes relevant immediately after. Investors who intend to renovate and flip or refinance need to understand that most lenders will not lend on a property that was purchased at auction within the past six to twelve months without substantial additional equity cushion. Hard money lenders will lend, but at significantly higher interest rates than conventional financing.

Property condition risk is real. Properties that reach trustee sale have typically gone without maintenance for months. Broken HVAC systems, water damage from deferred gutters, pest infestations, and cosmetic damage that looks minor but is actually structural are all common. Budget 15 to 25 percent above the purchase price for renovation costs, and in high-cost markets, budget higher.

How Investors Use DistressIQ to Track Trustee Sales

The most time-consuming part of trustee sale investing is the weeks of research beforehand. DistressIQ tracks distress signals across 3,200 plus counties and updates them daily, so investors can identify properties in pre-foreclosure before the auction date is even set. An investor who finds a property at the notice of default stage has more time to order the title report, verify the occupant situation, and calculate the opening bid. Waiting until the auction notice is posted may leave only three weeks of research time against competitors who have already done their homework.

DistressIQ's free browsing tier lets investors see properties with active distress signals before paying for lead details. The motivation score reflects how long a property has been in distress and how many overlapping signals it carries, helping investors prioritize which approaching auctions to research first.

Trustee Sale vs. Other Distress Signal Types

Trustee sales are one of several distress signals investors can target. Each signal type has a different risk profile, timeline, and investor skill requirement.

Sheriff sales are similar to trustee sales but are court-ordered and conducted by a sheriff or marshal, typically in judicial foreclosure states. The process differs legally but the investment calculus is similar. Sheriff sale properties also sell at a discount and may carry similar title risks.

Pre-foreclosure describes properties where the owner has received a notice of default but has not yet reached the auction stage. These properties can often be purchased directly from the owner before the auction, avoiding the risks of the auction process entirely. Pre-foreclosure deals require more marketing and outreach skill but offer more flexibility.

REO properties are properties that lenders acquired at auction and are now selling through real estate agents. REO sales eliminate the auction risks (title risk from the auction process is gone) but the discount is smaller because the lender is now a motivated seller with a real estate agent managing the process.

Tax deed sales involve properties with unpaid property taxes. In tax deed states, the winning bidder at the tax sale receives title to the property outright. In tax lien states, the winning bidder receives a lien against the property and must wait for the redemption period to expire before receiving title. Tax deed sales carry their own specific risks, including properties with hidden structural problems that previous owners neglected because they were already in financial distress.

Frequently Asked Questions

Q: Can anyone bid at a trustee sale?

Yes. Trustee sales are public auctions. Anyone can attend, register, and bid. There is no license requirement, but every bidder must pay the winning bid amount immediately in certified funds or cashier's check after the auction closes.

Q: How much below market value do properties sell for at trustee sales?

Most trustee sale properties sell 20 to 40 percent below current market value. The actual discount depends on market conditions, the property's condition, the number of competing bidders, and the lender's motivation. In hot markets, multiple bidders often drive prices near market value. In soft markets, deep discounts are common.

Q: What happens if no one bids at the trustee sale?

If no bidder meets the opening bid, the property reverts to the lender as an REO (real estate owned) property. The lender then lists it with a real estate agent at a discount. Investors who missed the auction can often buy the same property from the lender weeks or months later, often at a price not far below the opening bid amount.

Q: What is the biggest mistake investors make at trustee sales?

Bidding without a clear renovation cost estimate is the most common error. Investors see a deep discount and compete aggressively without factoring in what it costs to bring the property to market. A property that sells for 30 percent below market value is not a bargain if the renovation costs are 40 percent of the purchase price.

Q: Do trustee sale properties come with financing?

No. Trustee sales are all-cash events. The winning bidder pays the full purchase price immediately after the auction. Investors need capital lined up before attending. Hard money lenders and private lenders can fund quickly, but the arrangement must be in place before auction day.

DistressIQ tracks over 11 million active distress signals across 3,200 plus counties, including properties approaching or in the trustee sale process. Investors can browse properties with verified distress signals for free and export leads to CSV. See DistressIQ for current pricing and county coverage details.

The data behind this article

DistressIQ Monitors These Signals in Real Time

Pre-Foreclosures

NOD + NTS filings

Tax Delinquency

County treasurer records

Code Violations

Municipal inspection filings

Probate Filings

Superior Court records

Every lead is scored 0–100 for seller motivation based on signal type, duration, severity, and stacking. Nationwide coverage — every US county, updated daily.

Ready to find deals in your market?

See Live Distress Signals in Your County

Stop calling dead leads. Every lead in DistressIQ is scored 0–100 for seller motivation, with verified contact info included. Browse the free tier to see what's active in your market right now.

Browse Free Leads — No Credit Card