Probate Real Estate: The Investor's Guide to Executor Sales in 2026

Probate Real Estate: The Investor's Guide to Executor Sales in 2026

TL;DR: Probate real estate refers to property sales conducted by court-appointed executors during estate settlement. These sales often occur below market value due to urgency, multiple heirs, and carrying cost pressure. Investors succeed by understanding court timelines, contacting executors early, and distinguishing between full probate and simplified estate transfers.

Most real estate investing channels treat probate like a magic word. Say it and watch engagement spike. What they rarely explain: probate real estate operates under an entirely different rulebook than traditional transactions. The timeline is different. The decision-makers are different. The pricing psychology is different.

Investors who approach probate properties like regular motivated seller leads leave money on the table. The ones who understand executor authority, court procedures, and heir dynamics find deals that never reach public listing.

This guide explains how probate real estate actually works. Not the generic "people die and families need to sell" version you've heard a hundred times. The actual mechanics of court-supervised sales, executor authority, and the specific strategies that convert probate leads into closed deals.

What Probate Real Estate Actually Means

Probate real estate is any property transaction where the seller is an estate administrator rather than a living owner. When someone dies owning real property, that property cannot legally transfer to heirs until the estate passes through probate court.

This creates a distinct investment category with specific characteristics:

Court-involved timeline. Estates don't move on investor schedules. Creditor notice periods, court hearings, and heir consensus requirements add 3 to 12 months to the typical sale process. Investors who need 30-day closes should look elsewhere.

Authorized seller, emotional owners. The executor makes decisions. Heirs have opinions. This gap between legal authority and emotional attachment creates both opportunity and friction. The executor may want a clean, fast sale. The heirs may want top dollar, or may disagree on whether to sell at all.

Carrying cost pressure. Estates pay property taxes, insurance, maintenance, and utilities on vacant properties. These costs accumulate monthly against eventual proceeds. An executor managing an estate with three properties in three states faces genuine financial pressure to liquidate efficiently.

Information asymmetry. Executors are often navigating probate for the first time. They don't know typical timelines, reasonable offers, or standard procedures. An investor who can explain the process credibly builds immediate trust.

These factors combine to create motivated sellers who are simultaneously sophisticated (represented by counsel, following court procedure) and unsophisticated (unfamiliar with property values, timelines, and investor tactics).

The Probate Sale Process: What Investors Need to Know

Understanding the probate timeline helps investors know when to engage, what to offer, and how long to wait.

Phase 1: Court Appointment (Weeks 1–4)

Someone files a petition with the probate court to open the estate. The court appoints an executor (if there's a will) or administrator (if there isn't). Letters testamentary or letters of administration are issued, giving the personal representative legal authority to act on behalf of the estate.

Investor opportunity: Very early. Most executors haven't thought about the property yet. Early contact builds relationship before competition arrives. The best investors find filings within days of court entry.

Phase 2: Creditor Notice Period (Months 2–6)

Most states require estates to publish notice to creditors and allow 3–6 months for claims. Some states run shorter (Texas: 90 days). Others run longer (New York: 7 months). During this period, the executor has authority but may be cautious about major decisions pending creditor resolution.

Investor opportunity: Relationship building. Executors are gathering information, inventorying assets, and determining whether to keep or sell properties. Your initial contact positions you as a resource when they're ready to move.

Phase 3: Active Administration (Months 6–12)

After the creditor period closes, the executor can sell assets. This is when probate real estate deals typically happen. Executors with clear authority and accumulating carrying costs become motivated sellers.

Investor opportunity: Acquisition. Offers made during this window have the highest acceptance rates. The legal path is clear, financial pressure is mounting, and heirs have typically reached consensus on liquidation versus retention.

Phase 4: Distribution or Sale (Months 12–24)

The estate either transfers property to heirs (who may then sell independently) or sells through court-confirmed sale. Some estates drag on for years due to disputes, tax issues, or complex assets.

Investor opportunity: Depending on state law, you may still acquire properties from heirs after distribution. These aren't "probate sales" technically, but they often retain similar motivation dynamics, out-of-area owners, multiple heirs needing cash distribution, and properties with deferred maintenance.

Types of Probate Real Estate Sales

Not all probate sales are created equal. Understanding the three main types helps investors set appropriate expectations.

Independent Administration Sales

In these states, executors have broad authority to sell estate property without court involvement. The sale proceeds like a normal transaction, though the seller is an estate rather than an individual.

States with independent administration: Most states follow this model. Executors have authority granted by the will or by statute. They can list, negotiate, and close without court hearings.

Investor approach: Treat like a standard purchase with extended timeline expectations. The executor has authority. The friction comes from heir dynamics, not legal constraints.

Supervised Administration Sales

Some states require court approval for estate property sales. The executor must petition the court, obtain a hearing date, and often open the sale to overbid at the confirmation hearing.

States with supervised requirements: California (through the Independent Administration of Estates Act, many sales still require court confirmation), Florida (formal administration), and others depending on estate specifics.

Investor approach: Plan for extended timelines and potential overbid risk. Your offer may be subject to a court hearing where other bidders can appear and offer more. Building rapport with the executor matters more, since they control whether your offer goes to hearing.

Living Trust Transfers

Technically not probate, but worth mentioning. Property held in a living trust transfers to beneficiaries without court involvement. The trustee (not an executor) manages the sale.

Why investors care: Trust transfers often happen faster than probate, with less public record visibility. The "trustee sale" isn't the distressed category you're targeting unless the property has other distress signals (tax delinquency, code violations, vacancy).

Free Weekly Alerts

See What's Distressed in Your Market

Get free weekly alerts — new distressed properties, motivation scores, and hot neighborhoods in your area. Addresses and contact info available inside DistressIQ.

Free forever · No credit card · Unsubscribe anytime

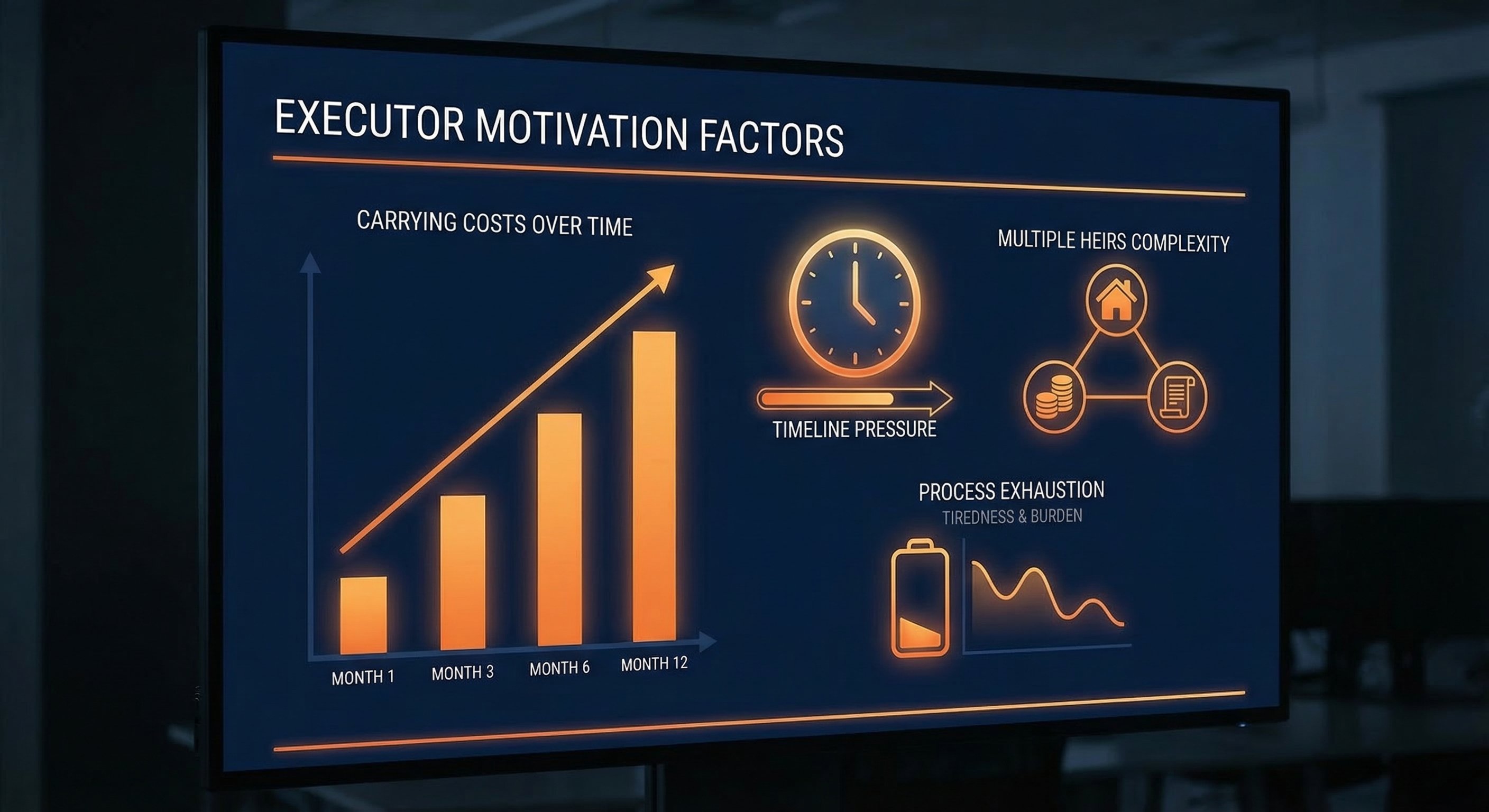

Why Executors Sell Below Market

The psychology of probate real estate differs fundamentally from traditional sales. Executors aren't homeowners upgrading for space or downsizing for retirement. They're fiduciaries liquidating assets to settle debts and distribute proceeds.

Three factors drive below-market pricing:

1. Carrying cost math. An estate holding a $300,000 property pays approximately:

- Property taxes: $3,000–$6,000/year

- Insurance (vacant property): $1,500–$3,000/year

- Utilities: $1,200–$2,400/year

- Maintenance/landscaping: $1,000–$3,000/year

That's $6,700–$14,400 annually in cash outflows against uncertain future sale proceeds. Over an 18-month probate, the estate might spend $15,000–$25,000 just holding the property. A $270,000 cash offer today can look better than a $300,000 offer in 9 months.

2. Multiple heir pressure. An estate with four heirs generates four opinions, four sets of cash needs, and four patience levels. The executor balancing these dynamics often prefers a clean sale at a reasonable price over a protracted negotiation for maximum value.

3. Process exhaustion. Probate is emotionally draining. Executors are often grieving while managing legal complexity, family tension, and financial detail. An investor who makes the process easy, with a cash offer, as-is purchase, flexible closing, and no repairs required, earns significant goodwill.

The empathy point matters here. Executors reading articles about "probate leads" and "opportunity windows" feel transactional pressure during an already difficult process. Investors who frame themselves as problem-solvers, not opportunists, build reputations that generate repeat referrals from estate attorneys.

Finding Probate Real Estate Opportunities

The best probate deals never reach the MLS. They happen through direct executor contact, estate attorney referrals, or data platforms that surface filings before public awareness builds.

Data-Driven Approach

Probate filings are public record. The challenge is finding them quickly across thousands of county court systems with varying digital access.

County court monitoring. Every county probate court maintains records. Some publish online case searches. Others require in-person access. The U.S. Courts explain that probate administration is governed primarily by state law, which is why timelines and procedures vary so sharply by jurisdiction (uscourts.gov). Sophisticated investors learn the systems in their target counties and review new filings weekly.

Signal stacking. The strongest probate opportunities combine multiple distress signals. A probate filing on a property that's also tax delinquent, vacant, or has code violations indicates genuine urgency. The executor isn't just managing an estate. They're managing a deteriorating asset with compounding financial problems.

Timeline tracking. Probate cases progress predictably. An investor tracking case status can identify when estates reach the "active administration" phase and time outreach accordingly.

Relationship-Driven Approach

Estate attorney networks. Probate attorneys who regularly handle estate administration become referral sources for investor clients. They know which executors want quick sales, which properties have heir disputes, and which estates need cash fast.

Building these relationships requires patience. Attorneys protect client interests and won't refer investors who pressure executors or lowball aggressively. The investors who get referrals are the ones who close smoothly, communicate professionally, and leave executors satisfied.

Title company relationships. Title agents handling probate transactions know which estates are selling and which investors close reliably. A title company that knows you'll perform can alert you to upcoming probate sales.

Platform Approach

DistressIQ surfaces probate filings automatically across thousands of counties. The platform identifies newly filed estates with real property, scores cases by signal strength, and provides executor contact information. Instead of monitoring multiple county portals manually, investors review a unified pipeline of probate leads ranked by opportunity quality.

The operational difference: manual researchers find cases weeks after filing when mailers have already arrived. Platform users see cases within days, making first contact before competition mobilizes.

Evaluating Probate Real Estate Deals

Not every probate property is a good investment. Executors with desirable properties in strong markets may achieve full market value (or above, in competitive court confirmation hearings).

Deal Qualifiers

Long ownership tenure. Properties owned for 20+ years typically have significant equity and deferred maintenance. High equity means the estate can accept below-market offers and still clear meaningful proceeds. Deferred maintenance means investors with rehab capabilities can add value.

Out-of-state heirs. Local heirs often want to retain family homes. Out-of-state heirs want cash distributions. Geographic distance correlates strongly with motivation to sell.

Multiple heirs. Three or more heirs typically accelerate the "sell versus keep" decision. It's easier for four people to agree on "sell and split the cash" than on co-ownership logistics.

Property condition issues. Homes needing significant repair discourage traditional buyers who need financing. Cash investors who can close as-is have structural advantage in probate acquisitions.

Deal Disqualifiers

Recent refinancing. An estate with a property refinanced two years ago may have limited equity and limited flexibility on price.

Single local heir. One heir living nearby often keeps the property or moves into it. Limited motivation for quick sale.

Estate attorney blocking contact. Some attorneys view investor contact as predatory and block outreach. While not a deal-killer, this friction reduces conversion probability.

Making Offers on Probate Properties

The offer structure for probate real estate differs from traditional purchases.

Timing

Best: Months 4–10 of the probate process. The executor has authority. Carrying costs are accumulating. Heirs have typically reached consensus on liquidation versus retention.

Acceptable: Months 2–4. Early contact builds relationship. The executor may not be ready to sell, but you'll be the first call when they are.

Challenging: Month 1 or Year 2+. Too early and the executor lacks authority. Too late and the property has already transferred to heirs or been listed traditionally.

Structure

Cash offers. Estates need certainty. Contingent offers that might fall through create risk executors avoid. Cash offers with proof of funds carry significant weight.

As-is purchases. Executors don't want to manage repairs, inspections, or contractor relationships. "As-is, where-is" language in your offer eliminates friction.

Flexible closing. Probate timelines vary. Offer flexibility on closing date so the executor can coordinate with court schedules and heir availability.

No wholesale assignments. Many probate sales require disclosure of the ultimate buyer. Assigning your contract to an end buyer may violate purchase agreements or court requirements. Buy to hold or buy to resell, but don't structure wholesale assignments without legal review.

The Ethics of Probate Real Estate

Executors have fiduciary duties to estates. Investors have opportunities to provide liquidity. The line between helpful service and predatory behavior matters.

What ethical probate investing looks like:

- Transparent offers (clear explanation of price, repair assumptions, and intended exit)

- Reasonable pricing (below-market is legitimate, drastically below market raises ethical questions)

- Professional conduct (respectful communication, no pressure tactics, honoring commitments)

- Post-close support (helping executors with utility transfers, lock changes, moving coordination)

What predatory investing looks like:

- Concealing information about property value

- Pressuring executors before they understand their options

- Renegotiating after inspection to extract additional concessions

- Targeting grieving families with aggressive urgency tactics

The investors who build sustainable probate practices work with estate attorneys, not against them. They leave executors feeling helped, not exploited. This reputation compounds into attorney referrals and repeat deal flow.

Probate Real Estate by State

Probate procedures vary significantly by jurisdiction. Three state-level factors affect investor strategy:

Creditor period length. Texas estates commonly operate under a 4-month creditor claim window after notice to unsecured creditors, while New York executors often work with a practical 7-month creditor period before final distribution planning (Texas Estates Code, New York Courts). Short creditor periods mean faster sales. Long periods mean extended holding costs.

Court confirmation requirements. California's Independent Administration of Estates Act gives many personal representatives broad sale authority, but some transactions still require additional notice or court involvement depending on the estate and granted powers (California Courts). Florida formal administration is also more court-supervised than the average independent-administration state.

Tax treatment. Some states have inheritance taxes that affect executor decisions. Others don't. Knowing whether your state taxes estate transfers helps you understand executor motivation.

Investors focusing on specific markets should study local probate procedure. Generic "probate investing" advice doesn't account for these jurisdictional variations.

Building a Probate Real Estate Pipeline

Sustainable probate investing requires systems. Manual courthouse research doesn't scale. Ad hoc relationships with attorneys don't compound. For related playbooks, investors often pair this workflow with how to find probate properties and how to find distressed properties.

Key systems:

Lead sourcing. Whether through county monitoring, attorney relationships, or data platforms, you need consistent lead flow. Target: 20–50 new probate leads monthly in your market.

Qualification. Not every lead deserves follow-up. Create criteria (minimum equity, property condition, heir situation) and filter aggressively.

Outreach cadence. Probate moves slowly. A letter at month 2, follow-up at month 4, check-in at month 6 captures opportunities as executors reach decision points.

Conversion tracking. Know your numbers. How many leads? How many contacts? How many offers? How many closes? This data improves your process over time.

Post-close reputation management. Executors talk to attorneys. Attorneys talk to other executors. Close smoothly and communicate professionally, and your reputation becomes a deal-generation asset.

How DistressIQ Tracks Probate Real Estate

The core challenge in probate investing is timing. Estates file, attorneys get appointed, carrying costs accumulate, and many investors only hear about opportunities weeks or months later when someone publishes a list.

DistressIQ organizes county-verified probate records across 3,200+ counties. New estates with real property surface in one dashboard within days of filing, with executor contact information and prioritization that helps investors focus on the highest-urgency cases.

When a probate filing stacks with tax delinquency, code violations, or vacancy status, the property moves higher on the list, so investors can focus on the deals with genuine financial pressure behind them.

Investors who also work other distress channels usually combine probate with tax delinquent properties so outreach is based on multiple signals instead of a single event.

Frequently Asked Questions

Q: What is probate real estate?

Probate real estate refers to property transactions where the seller is a court-appointed executor or administrator settling an estate. The property owner has died, and the estate requires court supervision to transfer or sell assets. These sales often occur below market value due to carrying cost pressure and executor motivation for efficient liquidation.

Q: How long does probate real estate take?

The full probate process typically runs 6 to 24 months depending on state law and estate complexity. Creditor notice periods range from about 90 days in some states to 7 months or more in others. Investors usually find their best acquisition window between months 4 and 12, when the executor has authority and carrying costs have accumulated.

Q: Can executors sell real estate without court approval?

In most states, yes. Independent administration allows executors to sell property without full court supervision. Some states, including certain California and Florida cases, require more notice, hearings, or court confirmation. Even then, executors usually retain authority to negotiate and accept offers before the final procedural step.

Q: Why do probate properties sell below market?

Three factors drive below-market pricing: carrying costs, multiple heir pressure, and process exhaustion. Executors often value certainty, speed, and a clean as-is closing almost as much as headline price.

Q: How do investors find probate real estate?

The main approaches are county probate record research, referrals from estate attorneys, and title or data relationships that surface new filings early. The best operators usually combine probate records with other property signals so they are not relying on a single event.

Q: What makes a good probate real estate deal?

Strong probate deals usually feature high equity, long ownership tenure, out-of-state heirs, multiple beneficiaries, and visible condition issues that make financed retail buyers less likely to compete aggressively.

Q: Is probate real estate investing ethical?

It can be, if the investor is transparent, fair, and easy to work with. Ethical investors explain their pricing, avoid pressure tactics, honor commitments, and help executors solve a real estate problem during a difficult period.

Ready to find probate real estate in your market? DistressIQ organizes county-verified probate records, tax delinquencies, and distress signals across 3,200+ counties, so investors can see estate sales earlier and act with better context. Explore DistressIQ.

The data behind this article

DistressIQ Monitors These Signals in Real Time

Pre-Foreclosures

NOD + NTS filings

Tax Delinquency

County treasurer records

Code Violations

Municipal inspection filings

Probate Filings

Superior Court records

Every lead is scored 0–100 for seller motivation based on signal type, duration, severity, and stacking. Nationwide coverage — every US county, updated daily.

Ready to find deals in your market?

See Live Distress Signals in Your County

Stop calling dead leads. Every lead in DistressIQ is scored 0–100 for seller motivation, with verified contact info included. Browse the free tier to see what's active in your market right now.

Browse Free Leads — No Credit Card