How to Find Pre-Foreclosure Leads in New Jersey (2026 Investor Guide)

How to Find Pre-Foreclosure Leads in New Jersey (2026 Investor Guide)

TL;DR: New Jersey's judicial foreclosure process averages over 1,000 days from first filing to sheriff's sale, producing one of the longest pre-foreclosure windows in the country. The lis pendens filing marks the starting line for every case. Investors who track these filings early gain a clear advantage in a state where Essex, Hudson, and Passaic counties lead in volume. The 2024 Community Wealth Preservation Program further shifted value toward direct homeowner negotiations before any auction takes place.

New Jersey processes every foreclosure through its Superior Court system. No non-judicial path exists. The average NJ foreclosure runs between 1,000 and 1,500 days from initial filing to sheriff's sale (1). In Essex and Hudson counties, court backlogs push timelines even longer.

For investors, this is not a problem. It is the entire opportunity. A process that takes three or four years creates three or four years of homeowners who may need a solution before any public auction.

How New Jersey's Judicial Foreclosure Pipeline Works

Every NJ foreclosure starts with a Notice of Intention to Foreclose (NOI). Under the Fair Foreclosure Act (N.J.S.A. 2A:50-56), lenders must send this notice at least 30 days before filing a complaint, but no more than 180 days before. The NOI must arrive via registered or certified mail.

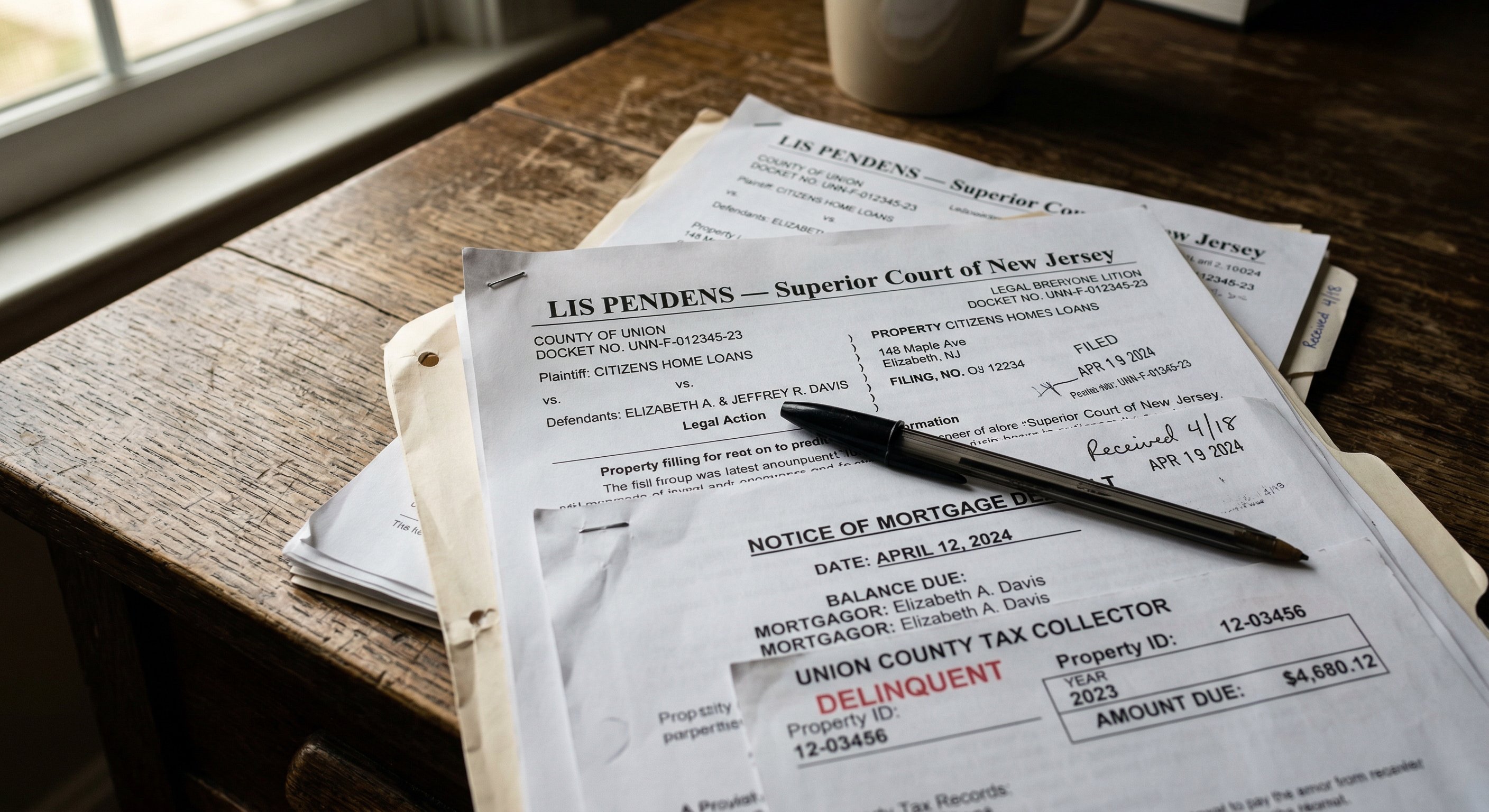

Once the NOI period passes, the lender files a complaint with the Superior Court in the county where the property sits. This triggers a lis pendens: a public notice recorded with the County Clerk indicating that a lawsuit affecting title is pending. The lis pendens is the signal.

From there the case moves through service of process, the homeowner's response, and a final judgment of foreclosure. Only after that judgment does the court authorize a sheriff's sale. Procedural protections and court volume contribute to timelines that routinely exceed three years.

Why the Lis Pendens Filing Is the Signal That Matters

An investor who finds a lis pendens on the day it is filed faces a fundamentally different deal than one who finds the same property 100 days later.

In the first weeks after filing, homeowners often believe they can secure a modification, catch up on payments, or find another path. Some are right. NJ's long timeline gives them room to try.

By day 100, the situation has shifted. The homeowner has received legal documents, likely spoken with an attorney or housing counselor, and has a clearer picture of whether modification is realistic. The shift from "this can be fixed" to "help is needed" often happens in that first 100-day window.

Investors who arrive at day one with a clear offer face less competition than those arriving at day 100 alongside every other buyer who found the same record. Earlier outreach means more trust and a higher likelihood of being the buyer the homeowner calls when ready.

In Georgia, foreclosure completes in 37 days. In New Jersey, the first weeks and months are a genuine strategic window.

County Breakdown: Where the Volume Lives

New Jersey's 21 counties each maintain separate Superior Court records. The five counties that consistently generate the most pre-foreclosure filings are:

Essex County. Newark, Irvington, and East Orange drive the highest case volume in the state. Older housing stock and a backlogged court system keep filings high. Price points are among the lowest in northern New Jersey, creating room for investor margin.

Hudson County. Jersey City, Bayonne, and Union City produce significant filings despite rising property values. Many owners here purchased near market peaks and have been underwater for years.

Passaic County. Paterson generates consistent volume at accessible price points for investors entering the market.

Camden County. Deep urban distress in Camden city alongside relative stability in suburbs like Cherry Hill. The urban core produces the majority of filings.

Atlantic County. Atlantic City's casino-driven economy creates boom-bust housing cycles and spikes in delinquency. Properties here have often been vacant for extended periods.

Bergen County offers lower volume but higher per-deal value. Middlesex generates volume through population density. Ocean and Monmouth counties combine suburban demand with Shore-market volatility that produces sudden clusters of distress.

Free Weekly Alerts

See What's Distressed in Your Market

Get free weekly alerts — new distressed properties, motivation scores, and hot neighborhoods in your area. Addresses and contact info available inside DistressIQ.

Free forever · No credit card · Unsubscribe anytime

Urban, Suburban, and Shore: Three Different Markets

New Jersey is not one housing market. The strategy that works in Newark differs from what works in Toms River.

Urban markets like Newark, Trenton, and Camden feature high volume and lower price points. Homeowners here often face multiple pressures: mortgage default, tax delinquency, code violations, and deferred maintenance. The investor who can address all of these has the strongest offer.

Suburban markets in Bergen, Morris, and Somerset produce fewer filings, but each tends to involve a single-family homeowner facing specific hardship: job loss, divorce, medical debt, or an estate situation. Outreach here requires more sensitivity. These are families in a difficult moment.

Shore markets in Ocean, Atlantic, and Cape May have a seasonal dimension. Vacation rental properties hit distress when tourism income drops or carrying costs become unsustainable. The best time to find these leads is in the months after a weak summer season.

The Community Wealth Preservation Program and What It Changed

New Jersey's Community Wealth Preservation Program (CWPP), enacted in 2024, introduced a right of first refusal at sheriff's sales for homeowners, their next of kin, tenants, and nonprofit community development corporations (2).

Even after winning a bid at auction, a qualifying party can step in and match the price. The program also imposes an 84-month residency requirement on certain buyers who acquire properties through this right, creating a seven-year lockup that eliminates flip and rental strategies.

Sheriff's sales have become a less predictable acquisition channel. The pre-foreclosure stage, where a deal is negotiated directly with the homeowner before court proceedings conclude, now offers a cleaner path. Much of the investor education content in the NJ market has not caught up to this law. Investors who understand the CWPP's implications have a structural information advantage over those still approaching auctions as they did in 2023.

Finding Leads: The Manual Process and Its Limits

Every lis pendens is public record, filed with the County Clerk. NJ's eCourts portal provides access to foreclosure filings statewide. In theory, an investor could monitor all 21 counties daily.

In practice, this means 21 separate systems with varying interfaces and search capabilities. Some portals require block-and-lot numbers rather than owner names. Cross-referencing filings against assessor records and skip tracing takes hours per county.

Experienced NJ investors specialize in two or three counties when working manually. Those covering all 21 either run large teams or use a platform that aggregates and scores the data. Skip tracing adds cost on top: phone numbers and current mailing addresses require separate tools and per-record fees, and many records lead to dead ends.

The Outreach Approach

NJ homeowners in foreclosure are among the most legally informed in the country. Mandatory notices and access to housing counselors mean many have already consulted an attorney before any investor contacts them.

Aggressive outreach backfires. What works is straightforward communication: a letter or call that clearly states who the sender is and that they are available to discuss a sale.

Timing matters. The sweet spot is often 12 to 36 months after a lis pendens filing. By then the homeowner has exhausted modification options and has a realistic picture of what comes next. The investor who has been in touch consistently, without pressure, is the one who gets the call.

Given the CWPP, some homeowners will ask about their rights at the sheriff's sale. Those rights exist and can be valuable, but they also introduce uncertainty. A fair cash offer before the sale eliminates that uncertainty entirely.

Frequently Asked Questions

How long does the New Jersey foreclosure process take?

New Jersey averages between 1,000 and 1,500 days for a foreclosure to move from the initial Notice of Intention to a completed sheriff's sale. The process is entirely judicial, meaning every case passes through the Superior Court system. In Essex and Hudson counties, court backlogs push timelines well beyond the state average. The Fair Foreclosure Act adds mandatory notice periods and mediation programs in some counties that extend the timeline further. This multi-year process creates an extended window for investors to contact homeowners before any public auction takes place.

What is a lis pendens and why does it matter for NJ investors?

A lis pendens is a public legal notice filed with the County Clerk indicating that a lawsuit affecting a property's title has been initiated. In NJ foreclosure cases, the lender files the lis pendens when the complaint is filed in Superior Court. This is the earliest public signal that a property is entering the foreclosure pipeline. Investors who track these filings gain a timing advantage because they can identify properties before competing buyers, before the homeowner has been overwhelmed by outreach, and while there is still time to negotiate a deal before the sheriff's sale is scheduled. In NJ's slow system, the gap between filing and sale can exceed two years, making this signal especially valuable.

Which New Jersey counties produce the most pre-foreclosure leads?

Essex County consistently leads the state in filings, driven by Newark and surrounding cities. Hudson (Jersey City, Bayonne), Passaic (Paterson), Camden, and Atlantic (Atlantic City) round out the top five. Each has distinct characteristics. Essex offers volume and lower price points. Hudson combines high property values with significant distress. Passaic provides accessible entry pricing. Camden features deep urban distress alongside stable suburbs. Atlantic City's tourism-dependent economy creates cyclical foreclosure waves. Bergen, Middlesex, and Ocean counties also warrant attention, where lower volume is offset by higher per-deal value.

What is the Community Wealth Preservation Program and how does it affect investors?

The CWPP was enacted in 2024. It grants a right of first refusal at sheriff's sales to homeowners facing foreclosure, their next of kin, tenants, and nonprofit community development corporations. Non-exempt buyers who acquire properties through the program must reside at the property for 84 months or face financial penalties. For investors, this means the sheriff's sale is no longer the clean acquisition path it once was. Deals negotiated directly with the homeowner before the case reaches auction have become the more reliable channel for acquiring distressed properties in New Jersey, because they avoid the right-of-first-refusal complication entirely.

Does New Jersey have a redemption period after a sheriff's sale?

New Jersey provides a 10-day redemption window after a sheriff's sale. During this period, the foreclosed homeowner can redeem by paying the full sale price plus costs. The 10-day window is shorter than many states' redemption periods, but it introduces brief uncertainty for auction buyers. If the property is not redeemed within 10 days, the sheriff's deed is delivered and the sale becomes final. Auction buyers must factor a 10-day hold into post-sale planning.

How do urban, suburban, and shore markets differ for NJ pre-foreclosure investing?

Urban markets (Newark, Trenton, Camden) produce high volume at lower price points, with homeowners often facing overlapping pressures including tax delinquency and code violations. Suburban markets (Bergen, Morris, Somerset) generate fewer filings but involve single-family homeowners in specific hardship situations like divorce, job loss, or medical debt. Shore markets (Ocean, Atlantic, Cape May) follow a seasonal pattern where vacation rental properties hit distress after weak tourism seasons. Each market type requires a different outreach approach and pricing model.

What is the Fair Foreclosure Act and how does it shape the NJ process?

The Fair Foreclosure Act (N.J.S.A. 2A:50-56) governs notice requirements and procedural steps lenders must follow before and during a foreclosure. Lenders must send a Notice of Intention to Foreclose at least 30 days before filing a complaint, using registered or certified mail. The act establishes timelines, notice content requirements, and homeowner protections throughout the process. For investors, the act is relevant because it defines when the lis pendens can be filed and how much advance notice homeowners receive before legal action begins. Understanding these timelines helps investors anticipate when new leads will surface and plan outreach accordingly.

Sources

- New Jersey Judiciary, "Foreclosure Self-Help," njcourts.gov

- New Jersey Legislature, P.L.2022, c.12 (Community Wealth Preservation Program), njleg.state.nj.us

The data behind this article

DistressIQ Monitors These Signals in Real Time

Pre-Foreclosures

NOD + NTS filings

Tax Delinquency

County treasurer records

Code Violations

Municipal inspection filings

Probate Filings

Superior Court records

Every lead is scored 0–100 for seller motivation based on signal type, duration, severity, and stacking. Nationwide coverage — every US county, updated daily.

Ready to find deals in your market?

See Live Distress Signals in New Jersey

Stop calling dead leads. Every lead in DistressIQ is scored 0–100 for seller motivation, with verified contact info included. Browse the free tier to see what's active in your market right now.

Browse Free Leads — No Credit Card