How to Find Foreclosure Leads in Florida (2026 Investor Guide)

How to Find Foreclosure Leads in Florida (2026 Investor Guide)

TL;DR: Florida requires every foreclosure to pass through the circuit court system, producing a pipeline that runs six months to over three years depending on the county and whether the homeowner contests the case. The investors who find the best foreclosure leads in Florida track lis pendens filings, final judgments, and tax deed applications across all 67 counties, stacking multiple distress signals on each property before competing buyers know the homeowner is in trouble.

Florida averages roughly 950 days from lis pendens filing to completed foreclosure sale, per ATTOM Data Solutions. That is nearly three times the timeline in non-judicial states like Texas or Georgia, where a property can move from default to auction in under 90 days. For real estate investors targeting distressed properties in Florida, that extended timeline is not a delay. It is the entire opportunity.

Every foreclosure in Florida moves through the courts. The lender files a lawsuit. The homeowner gets served. The case sits on the circuit court docket while both sides exchange discovery. A judge enters final judgment. The clerk schedules the sale. At every stage, the distress signal becomes public record, available to anyone who knows where to look.

Florida's Judicial Foreclosure Timeline: Where the Leads Live

The Florida foreclosure process has five distinct stages. Each produces a different type of lead with a different level of seller motivation and a different contact window.

Stage 1: Default and Lis Pendens Filing

When a borrower falls 90 or more days behind, the lender files a complaint in the county circuit court and records a lis pendens with the county clerk. This public notice signals that the property is subject to active litigation.

This is the earliest and often the most productive signal. The homeowner knows about the lawsuit and is typically still weighing options: loan modification, short sale, or an outright sale. A cash offer at this stage gives the homeowner a real alternative to a foreclosure auction that would damage their credit for seven years. The timeline from first missed payment to lis pendens filing runs 120 to 180 days in most cases.

Stage 2: Court Proceedings

After the complaint is filed, the lender must serve the homeowner, who has 20 days to respond under Florida Rule of Civil Procedure 1.140. Contested cases enter discovery and can stretch 12 to 24 months before trial.

This middle phase is where most investors stop paying attention. That is a mistake. Homeowners in active litigation but pre-judgment are often more receptive to conversation than people facing an imminent auction date. The urgency is real but the panic has not set in. They answer the phone.

Stage 3: Final Judgment and Sale Date

Once the court enters a final judgment, the clerk schedules the property for public sale within 20 to 35 days. The sale gets advertised in a local newspaper and posted to official county records. The homeowner's options narrow fast at this point. A Chapter 13 bankruptcy or last-minute loan modification can pause the sale, but most homeowners in this position have already tried those paths without success.

Stage 4: Foreclosure Auction

Florida conducts most foreclosure auctions online through Realauction.com and Bid4Assets. The sale goes to the highest bidder above the lender's opening credit bid. Buyers must register in advance with guaranteed funds. Interior access is almost never available before bidding. Properties that attract no outside bidders revert to the bank as REO inventory.

Stage 5: REO Disposition

When the lender takes title, the property becomes Real Estate Owned, managed by the servicer's loss mitigation department and eventually listed through a local broker. REO deals close faster than pre-foreclosure transactions because the bank is the sole decision-maker. The tradeoff is price. The highest-value opportunities in Florida foreclosure investing happen in stages 1 through 3, before the bank owns the asset.

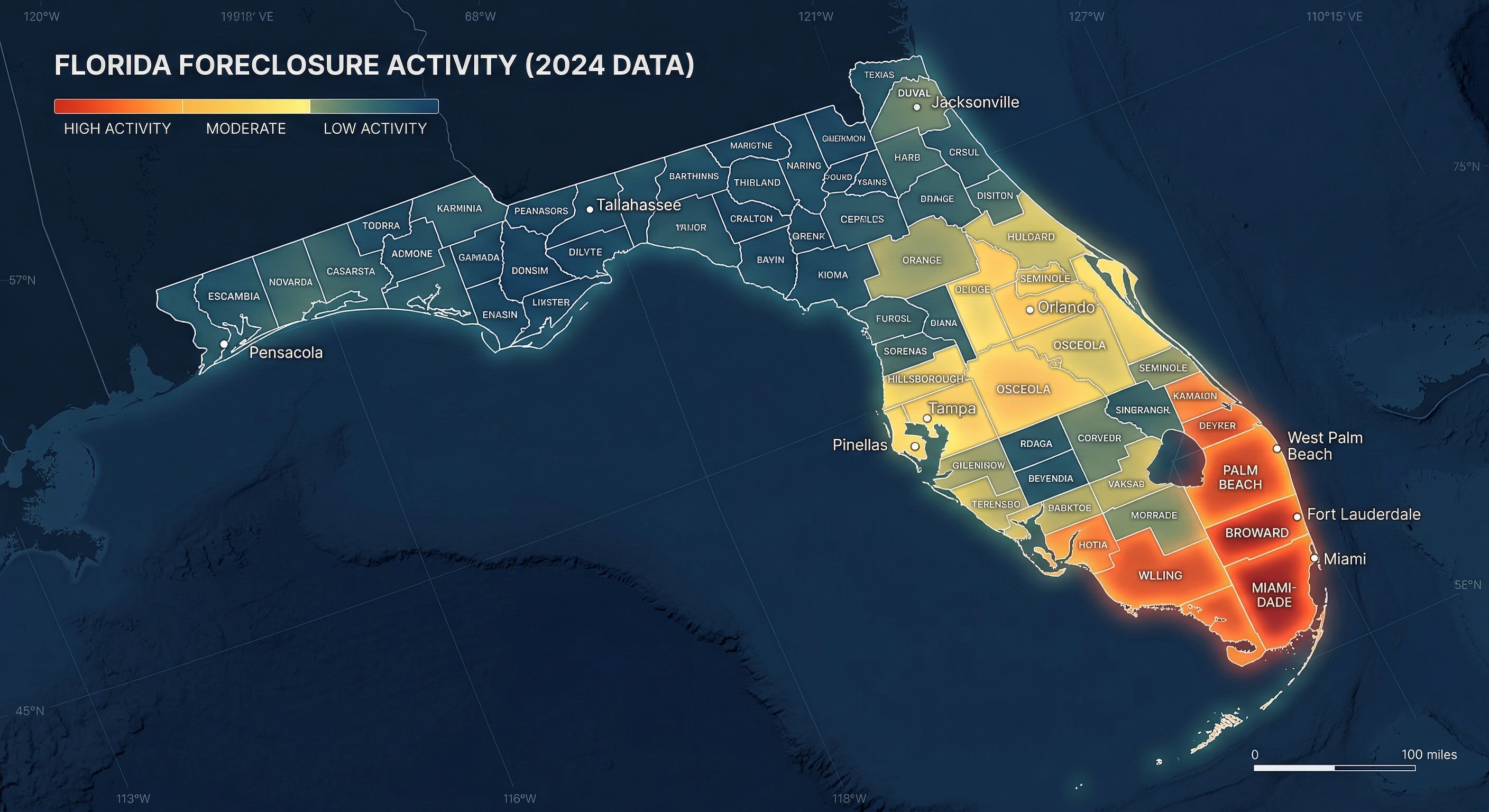

Where Foreclosure Records Live in Florida's 67 Counties

Each of Florida's 67 counties operates its own Clerk of Circuit Court website with its own search portal, case numbering, and download formats. The major counties offer relatively modern online access. Miami-Dade uses mdcourts.gov, Broward uses browardclerk.org, Hillsborough uses hcclerk.org, Orange uses myorangeclerk.com, and Palm Beach uses mypalmbeachclerk.com. Rural Panhandle counties including Gulf, Liberty, and Calhoun often require a phone call to the clerk's office or a physical courthouse visit.

Cross-referencing a single property across civil court records, property appraiser data, and tax collector information takes 20 to 30 minutes per address in a well-organized county. Scale that to 50 properties a week and it becomes a full-time administrative job that produces zero revenue.

Tax Deed Sales: Florida's Parallel Distress Track

Florida has a second foreclosure system that most out-of-state investors overlook. When a property owner falls behind on property taxes, the county sells a tax certificate at public auction, typically in May or June. The certificate holder earns interest at rates up to 18% per year. If taxes remain unpaid for two years, the certificate holder can apply for a tax deed, forcing a public auction of the property.

This sale is separate from mortgage foreclosure auctions and surfaces a different category of properties: often free-and-clear homes where the only distress signal is tax delinquency. Tax deed sales attract fewer bidders than mortgage foreclosures, but the due diligence requirements are higher since some liens survive a tax deed sale in Florida.

Investors running both tracks simultaneously find the same properties appearing in both systems. That overlap is a strong signal. A homeowner who cannot pay the mortgage and cannot pay property taxes has very few options remaining.

Free Weekly Alerts

See What's Distressed in Your Market

Get free weekly alerts — new distressed properties, motivation scores, and hot neighborhoods in your area. Addresses and contact info available inside DistressIQ.

Free forever · No credit card · Unsubscribe anytime

South Florida vs. North Florida: Two Different Markets

Florida is not one foreclosure market. It is at least three distinct regions.

South Florida (Miami-Dade, Broward, Palm Beach): These three counties consistently lead the state in foreclosure volume. The drivers are high property values, insurance costs that have more than doubled since 2020 as carriers pull out of the coastal market, and a large pool of investors who bought at the top with adjustable-rate or interest-only loans. The average timeline from lis pendens to sale runs 18 to 30 months because of court backlog.

Central Florida (Orange, Hillsborough, Polk, Seminole): Orlando and Tampa have seen foreclosure activity climb as property tax reassessments catch up with the 2021-2023 price runup. Orange County has a growing inventory of short-term rental properties where Airbnb income no longer covers the mortgage. These cases move faster, typically 10 to 16 months from filing to sale.

North Florida and the Panhandle: Lower property values mean smaller loan balances and fewer contested cases. A lis pendens filed in Duval County (Jacksonville) may reach final judgment in 8 to 12 months. The deals are smaller but so is the competition.

The Signal Stack: Why One Data Source Falls Short

The highest-converting foreclosure leads in Florida are not simply properties "in foreclosure." They are properties in foreclosure plus tax delinquent. Or in foreclosure plus carrying an open code violation. Or the subject of a lis pendens filed shortly after a recorded divorce decree.

Multiple simultaneous distress signals do not just indicate motivation. They indicate that the homeowner has exhausted alternatives. A property with four active distress signals is a situation where the homeowner needs a solution that only a fast cash buyer can provide.

Generic foreclosure lists deliver one signal: mortgage default. The properties that convert at three to four times the average rate are the ones where the financial situation has cascaded. Mortgage in default, taxes unpaid, code enforcement lien, mechanics lien from a contractor who never got paid. These layered signals separate "mildly motivated" from "needs to sell this month."

DistressIQ stacks 20+ signal types per property across all 67 Florida counties into a single 0-to-100 motivation ranking. Properties showing lis pendens plus tax delinquency plus code violation score higher than a clean lis pendens filing with no other distress indicators.

Florida-Specific Factors That Change the Deal

Homestead Exemption. Florida's constitution provides some of the strongest homestead protections in the country. A primary residence is shielded from forced sale for most creditor claims, with two exceptions: the mortgage itself and property taxes. Junior lienholders cannot force a sale of a homesteaded property. For investors, this affects which liens survive a foreclosure sale and how to structure an offer on a property with multiple judgment creditors.

Deficiency Judgments. If foreclosure sale proceeds do not cover the outstanding debt, the lender may pursue a deficiency judgment within one year under Florida Statute 702.06. Many borrowers prefer a negotiated pre-foreclosure sale that includes a deficiency waiver rather than risking a six-figure judgment after auction.

Property Insurance Costs. Homeowners insurance in South Florida has doubled or more since 2020, with several major carriers withdrawing from the market. For homeowners already stretched by mortgage payments, the insurance escalation has become a primary driver of default. This is a Florida-specific distress factor that does not exist in most states and it is accelerating.

Auction Competition. South Florida auctions attract institutional buyers and well-capitalitized investor groups. Margins are thin. The better opportunity is contacting the homeowner six to eighteen months earlier, before the property appears on Realauction.com and every investor in the state sees it.

Frequently Asked Questions

Q: How long does the foreclosure process take in Florida?

Florida's judicial foreclosure process typically runs six months to three years from lis pendens filing to completed sale. The national average for all foreclosures is 762 days, according to ATTOM Data Solutions' Year-End 2024 U.S. Foreclosure Market Report, and Florida sits well above that average. Contested cases, bankruptcy filings, and court backlog in high-volume circuits like Miami-Dade and Broward push timelines toward the longer end. Rural counties in North Florida may reach final judgment in under a year. The timeline directly affects investor strategy because longer timelines create more opportunity for pre-sale contact but also increase the risk of property deterioration and title complications.

Q: What is the difference between pre-foreclosure and foreclosure leads in Florida?

Pre-foreclosure refers to the period after a lis pendens is filed but before the court enters final judgment. The homeowner still has multiple options including loan modification, short sale, refinancing, or an outright sale to a cash buyer. Foreclosure leads in the strict sense refer to properties after judgment, those scheduled for auction, or properties already bank-owned as REO. Both categories involve motivated sellers but the negotiation dynamics, available time, and deal structures differ significantly. Pre-foreclosure leads generally offer more flexibility and better pricing for investors because the homeowner still controls the outcome and has room to negotiate.

Q: Where can investors find Florida foreclosure auction listings?

Most Florida counties conduct foreclosure auctions online through Realauction.com and Bid4Assets. Each county clerk's office publishes upcoming sale dates and property details on its official website. Registration with the auction platform is required before bidding and buyers must have guaranteed funds available. Properties are sold as-is, usually without interior access, and buyers take title subject to any liens that survived the foreclosure action. Title insurance is available but requires a separate title search that most experienced bidders complete before the auction date to avoid inheriting surprises.

Q: How does the Florida tax deed process work?

When a property owner falls behind on property taxes, the county sells a tax certificate at public auction to investors, who earn interest at rates up to 18% per year. After two years of nonpayment, the certificate holder can apply for a tax deed, triggering a public auction through the county clerk's office. Tax deed sales are separate from mortgage foreclosure auctions and often involve properties free of mortgage debt, where the sole distress signal is unpaid taxes. The risk profile differs because some liens survive a tax deed sale in Florida, making a thorough title search essential before bidding.

Q: Can investors find foreclosure leads across all 67 Florida counties in one place?

Manually, no. Each county operates its own clerk of court and property records system with different search interfaces, case numbering, and data formats. DistressIQ aggregates verified foreclosure signals, lis pendens filings, tax deed applications, and code violations from all 67 Florida counties into a single searchable map with stacked motivation scores updated daily from county-direct sources. Investors can browse the map for free and unlock owner contact details only when ready to act on a specific lead.

Q: How does Florida's homestead exemption affect foreclosure investing?

Florida's constitutional homestead exemption protects a primary residence from forced sale by most creditors, with two exceptions: the mortgage holder and the tax collector. Junior lienholders such as credit card companies or medical providers cannot force the sale of a homesteaded property. For investors, this affects which liens survive a foreclosure sale and how to assess a property carrying multiple recorded judgments. The homestead exemption also limits the ability of unsecured creditors to reach home equity, which changes how motivated a homeowner might be to sell quickly versus waiting out the full court process.

The data behind this article

DistressIQ Monitors These Signals in Real Time

Pre-Foreclosures

NOD + NTS filings

Tax Delinquency

County treasurer records

Code Violations

Municipal inspection filings

Probate Filings

Superior Court records

Every lead is scored 0–100 for seller motivation based on signal type, duration, severity, and stacking. Nationwide coverage — every US county, updated daily.

Ready to find deals in your market?

See Live Distress Signals in Florida

Stop calling dead leads. Every lead in DistressIQ is scored 0–100 for seller motivation, with verified contact info included. Browse the free tier to see what's active in your market right now.

Browse Free Leads — No Credit Card