Pre-Foreclosure Leads Maryland: How to Find and Work Them Before the Auction

Pre-Foreclosure Leads Maryland: How to Find and Work Them Before the Auction

TL;DR: Maryland's judicial foreclosure process takes 6 to 12 months from default filing to auction, creating a longer and more accessible pre-foreclosure window than most non-judicial states. The key counties are Baltimore City, Prince George's County, Montgomery County, Baltimore County, and Anne Arundel County. Pre-foreclosure leads in Maryland work differently than sheriff sale leads in Texas or Georgia because every case goes through the circuit court system, requires mandatory mediation for owner-occupied properties, and can be halted at any point before auction if the homeowner negotiates a settlement or sells. Investors who pull county circuit court data directly and reach homeowners early in the process have a significant timing advantage over those who wait for properties to appear on public auction lists.

Most investors think of Maryland as a slow, bureaucratic market. That reputation is partly deserved, and for investors who know how to work the system, it is a genuine advantage. The Maryland circuit court process moves slowly, and that pace translates directly into a longer window to find motivated sellers, negotiate pre-foreclosure sales, and close deals before anyone else knows the property exists.

This article covers how pre-foreclosure leads in Maryland work, which counties produce the most actionable volume, what the judicial process looks like in practice, and how experienced investors use the extended timeline to their advantage.

What Is Pre-Foreclosure in Maryland

Pre-foreclosure begins the moment a lender files a foreclosure action in the county circuit court after a homeowner defaults on their mortgage. Unlike non-judicial states where a trustee can move a property to auction within 30 to 60 days of default, Maryland requires every foreclosure to pass through the circuit court system. That court process takes time, and that time is exactly what smart investors use.

A pre-foreclosure lead in Maryland is a homeowner who has received a foreclosure filing but has not yet been sold at auction. During this window, the homeowner may still be living in the property, may still have equity to negotiate with, and is typically highly motivated to avoid the auction and the credit damage that follows a completed foreclosure.

The path from default to auction in Maryland follows these stages: the lender files a foreclosure action in the county circuit court, the homeowner is served with foreclosure papers, a mediation request is initiated for owner-occupied properties meeting certain loan thresholds, the court schedules a hearing and potentially a ratification hearing after sale, and finally the property goes to auction if no resolution is reached.

Baltimore City, Prince George's County, and Montgomery County each carry the highest pre-foreclosure volumes in the state, though the nature of the inventory and the typical deal structure varies considerably between them.

The Counties That Matter for Maryland Pre-Foreclosure Leads

Not all Maryland pre-foreclosure leads are the same. The county determines the volume an investor works with, the typical price point, the condition of the inventory, and the court backlog that affects how long a pre-foreclosure case takes to resolve.

Baltimore City produces the highest pre-foreclosure volume in Maryland. Median home prices in Baltimore City typically range from $130,000 to $180,000, which means the entry point is accessible for most investors and the repair costs on distressed inventory are often lower than in suburban markets. The trade-off is condition. Baltimore City pre-foreclosure leads frequently involve properties with deferred maintenance, code violations, and long-term vacancy. For investors with renovation experience in urban markets, this is the most active and actionable market in the state.

Prince George's County is the second-highest-volume jurisdiction and arguably the most interesting for investors focused on equity plays. Located immediately outside Washington D.C., Prince George's County has median home prices in the $320,000 to $380,000 range. Pre-foreclosure leads here often involve homeowners who purchased at the peak, faced payment shocks from adjustable-rate resets or escrow increases, and now find themselves underwater or barely above water. The equity position in Prince George's County pre-foreclosure leads tends to be stronger than in Baltimore City, making assignment fees more attractive for wholesalers who connect these properties with the right cash buyers.

Baltimore County surrounds Baltimore City and operates at similar price points. Pre-foreclosure volume is substantial, and property condition tends to be slightly better than in the city proper because the housing stock is newer in many subdivisions.

Anne Arundel County and Montgomery County round out the top five jurisdictions. Anne Arundel County includes parts of the Baltimore metro area plus proximity to Annapolis, with median prices from $380,000 to $440,000. Montgomery County, which includes Bethesda, Rockville, and Silver Spring, is the most expensive market in the state, with median prices from $420,000 to above $500,000. Pre-foreclosure volume in Montgomery County is lower, but the equity position of homeowners who enter the process is often substantial.

The practical implication for investors is straightforward. Baltimore City offers the most deals to work with. Prince George's County offers the strongest equity plays for assignment-focused investors. Anne Arundel and Montgomery Counties offer fewer but potentially larger deals for investors with more capital to deploy.

Maryland Foreclosure Law: What Investors Need to Know

Maryland is a judicial foreclosure state, which means lenders must file a lawsuit in the county circuit court to foreclose. This has several direct implications for investors working pre-foreclosure leads.

The notice of intent to foreclose must be sent to the borrower at least 45 days before the lender files the foreclosure petition with the court. This 45-day period is a critical early window for investors who have access to pre-foreclosure data from county circuit court records. By the time the petition is filed and publicly available, the homeowner has already received written notice from the lender.

Once the petition is filed, the homeowner has 90 days to respond before the court schedules a hearing. During this period, lenders are required to request mediation for owner-occupied properties where the loan amount meets certain thresholds set by Maryland law. The mediation requirement creates a formal negotiation window that both parties are incentivized to use because litigation is expensive and time-consuming for everyone involved.

After a foreclosure sale is held, the sale must be ratified by the court, a process that can add 30 to 60 days depending on the county and court backlog. During this ratification period, the sale is not final, and Maryland law provides limited redemption rights in certain circumstances.

The entire process from initial default to completed auction typically takes 6 to 12 months in Maryland. Compare this to a non-judicial state like Texas or Georgia, where the trustee can auction a property within 30 to 45 days of the initial notice with minimal court involvement. That 5 to 11 month difference is where Maryland pre-foreclosure leads offer a structural advantage for investors who know how to use the time.

Free Weekly Alerts

See What's Distressed in Your Market

Get free weekly alerts — new distressed properties, motivation scores, and hot neighborhoods in your area. Addresses and contact info available inside DistressIQ.

Free forever · No credit card · Unsubscribe anytime

Why the Extended Timeline Changes the Investment Math

The 6 to 12 month Maryland pre-foreclosure window fundamentally changes the way investors approach these leads.

In a non-judicial state, the auction date moves quickly and without court involvement. Investors who do not reach the homeowner before the auction date lose their negotiating position almost entirely. In Maryland, the auction date is set by the court and can be delayed, continued, or halted entirely if the homeowner reaches a settlement with the lender or files for bankruptcy protection.

This means pre-foreclosure leads in Maryland stay actionable for longer. A homeowner who receives a foreclosure filing has more time to respond, more court-mandated touchpoints, and more opportunities to accept a negotiated sale than a homeowner in a non-judicial state where the trustee moves at full speed.

For wholesalers specifically, the Maryland pre-foreclosure timeline changes the workflow in a meaningful way. The extended window means more time to identify leads, verify ownership, run the numbers, make contact, negotiate an assignment contract, and market the deal to cash buyers before the auction arrives. The challenge is that county circuit court records are not easy to search systematically. They are public, but maintained county by county, with different filing systems, different access protocols, and different update frequencies.

This is where the difference between a focused platform and a general property database becomes obvious. Most investors who work Maryland pre-foreclosure leads manually spend hours navigating county court record databases, filing requests in person or by mail, and cross-referencing addresses against property records. A platform that pulls county circuit court data directly and scores pre-foreclosure leads by motivation level removes that friction and lets investors spend their time on what actually makes money, which is talking to homeowners and negotiating deals.

How to Evaluate Pre-Foreclosure Leads in Maryland

Once a pre-foreclosure lead is identified, experienced investors apply a consistent evaluation framework.

Equity position is the first check. Run the outstanding loan balance against estimated current market value using county assessor data, not MLS comps. In Maryland, assessor data is the legal record for tax purposes, and it provides a baseline for calculating whether a homeowner has equity or is already underwater. Prince George's County and Montgomery County pre-foreclosure leads tend to have stronger equity positions because home prices in those markets have held more consistently. Baltimore City leads often have thin or nonexistent equity, which usually means the deal structure requires a short sale negotiation with the lender.

Occupancy status signals urgency. Vacant properties mean the homeowner has already moved out, which signals high motivation but also requires a fast close. Tenant-occupied properties require different handling under Maryland tenant rights law.

Distress signal stacking is where Maryland pre-foreclosure evaluation becomes genuinely differentiated. A pre-foreclosure lead that also carries a code violation, an open permit, or a tax delinquent status is a property where the owner has multiple pressures converging simultaneously. Multiple converging signals consistently outperform single-signal leads because the motivation is not going away.

Finding Pre-Foreclosure Leads in Maryland: The Practical Path

The county circuit court is the primary source for pre-foreclosure filings in Maryland. Every foreclosure action is filed there, and the docket is a public record. Manual searching through county circuit court databases is possible but time-consuming. Each of Maryland's 24 counties maintains its own land records division, and the filing systems vary in accessibility and update frequency.

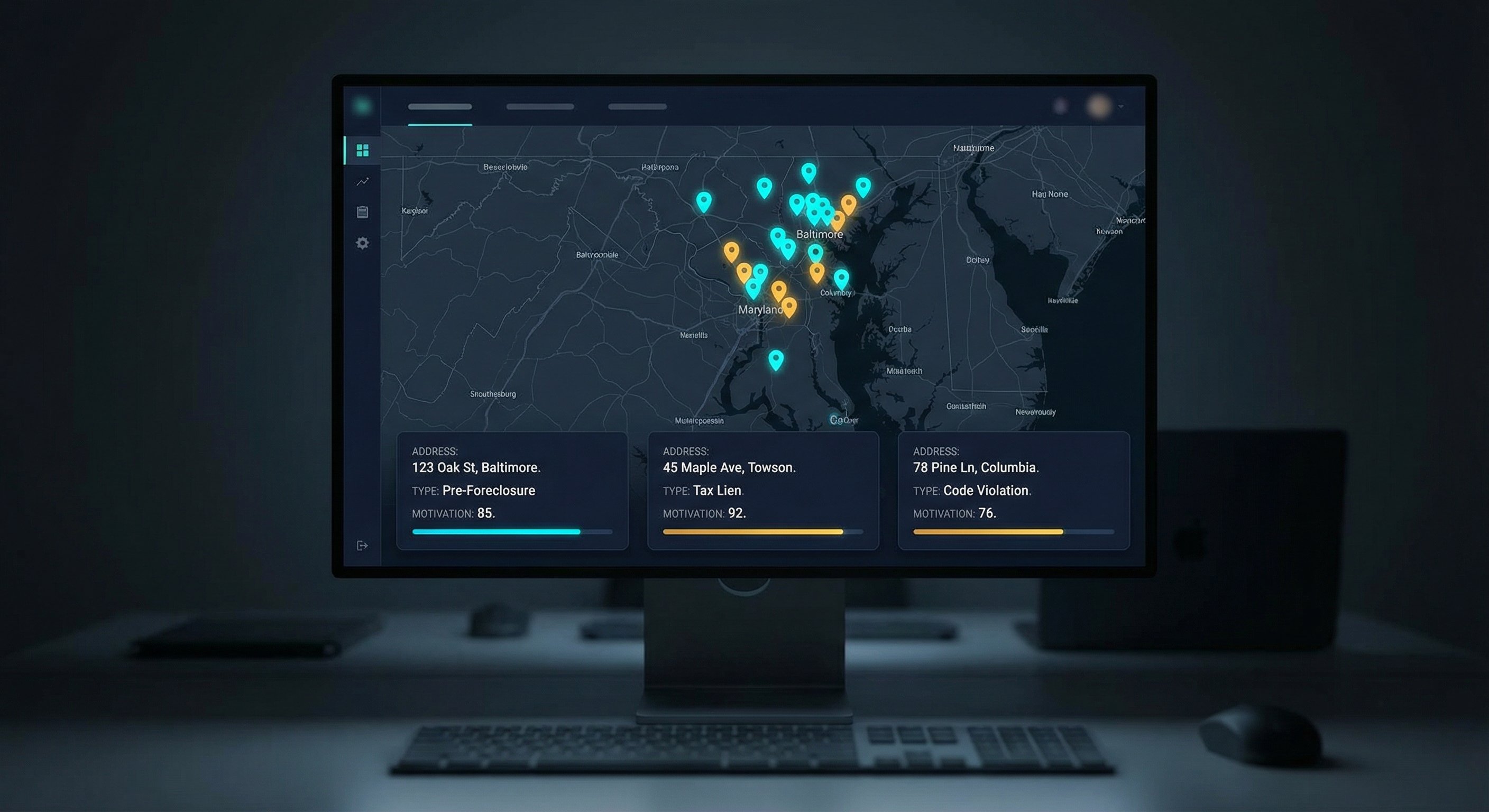

DistressIQ pulls county circuit court data directly and presents pre-foreclosure leads with motivation scores and cross-referenced distress signals, updated daily. Investors can filter by county, signal type, estimated equity position, and motivation score without navigating multiple court databases by hand. The most productive counties to monitor daily are Baltimore City, Prince George's County, Baltimore County, and Anne Arundel County.

Working Pre-Foreclosure Leads as a Wholesaler in Maryland

The wholesaler workflow in Maryland differs from a direct investment approach primarily in the exit strategy. A wholesaler identifies a pre-foreclosure lead, negotiates an assignment contract with the homeowner at a below-market price, and then markets the contracted deal to a cash buyer for an assignment fee rather than purchasing the property directly.

The Maryland pre-foreclosure timeline benefits wholesalers in a specific way. The 6 to 12 month court process means the auction date is not an immediate cliff. A wholesaler who gets a property under contract during pre-foreclosure can market it to buyers with a realistic closing timeline that fits the court schedule. Cash buyers who purchase at auction face a different risk profile and often require different pricing than buyers who are acquiring a pre-foreclosure sale that is already in contract.

The most common mistake made by new wholesalers working Maryland pre-foreclosure leads is moving too slowly. Waiting for a homeowner to appear on a public auction list means competing with every other investor who has the same information. Reaching a homeowner during the mediation phase, before the auction date is formally set, is where the negotiating position is strongest and the assignment fees are highest.

Frequently Asked Questions

How long does pre-foreclosure take in Maryland?

Pre-foreclosure in Maryland typically lasts 6 to 12 months from the date the lender files the foreclosure action in the county circuit court until the property is sold at auction. The timeline varies by county due to court backlogs and whether the case involves mandatory mediation.

Is Maryland a judicial or non-judicial foreclosure state?

Maryland is a judicial foreclosure state, which means every foreclosure must be filed as a lawsuit in the county circuit court. The court oversees the process, sets hearing dates, may order mediation, and must ratify the sale before it is final. This court involvement is what creates the longer pre-foreclosure window compared to non-judicial states like Texas or Georgia.

What is mediation in Maryland pre-foreclosure?

Maryland law requires lenders to request mediation for owner-occupied properties meeting certain loan thresholds before proceeding to auction. The mediation conference brings the homeowner and lender together with a neutral mediator to explore alternatives. This phase often produces the highest-motivation pre-foreclosure leads because both parties want to avoid the cost and delay of continued litigation.

Finding pre-foreclosure leads in Maryland requires understanding how the circuit court system works, which counties produce the most volume, and when in the process homeowners are most reachable. DistressIQ covers all 24 Maryland counties with daily-updated county circuit court data, cross-referenced distress signals, and motivation scores so investors can prioritize the leads most likely to convert. Browse pre-foreclosure leads in Maryland on DistressIQ.

The data behind this article

DistressIQ Monitors These Signals in Real Time

Pre-Foreclosures

NOD + NTS filings

Tax Delinquency

County treasurer records

Code Violations

Municipal inspection filings

Probate Filings

Superior Court records

Every lead is scored 0–100 for seller motivation based on signal type, duration, severity, and stacking. Nationwide coverage — every US county, updated daily.

Ready to find deals in your market?

See Live Distress Signals in Your County

Stop calling dead leads. Every lead in DistressIQ is scored 0–100 for seller motivation, with verified contact info included. Browse the free tier to see what's active in your market right now.

Browse Free Leads — No Credit Card