Foreclosure Leads Iowa: How the Judicial Process Creates Selective Opportunities

TL;DR: Iowa requires judicial foreclosure, meaning every residential foreclosure must receive court approval before proceeding to auction. This adds 60 to 120 days to the timeline compared to non-judicial states, but it also means properties often sit longer before appearing at the courthouse steps. Investors who monitor Iowa district court filings, understand the state's redemption mechanics, and know which counties produce the highest volume of sheriff sales can find properties trading at meaningful discounts before they reach the open market.

Most midwestern states run foreclosures through a non-judicial process. Iowa does not. Every residential foreclosure in the state must clear the district court before a property can be scheduled for sheriff sale. That single procedural difference shapes everything about how foreclosure leads Iowa functions as an investment market.

The delay is not a bug. For investors with capital ready and patience to deploy, Iowa's court-driven timeline creates an extended window to locate properties, research their full debt picture, and make informed bids well before auction day.

Why Iowa's Judicial Process Matters to Investors

In a non-judicial state like neighboring Illinois or Minnesota, a lender initiates default notices and moves directly to the auction calendar. The process can close in 90 days. Iowa's requirement for a court decree adds a minimum of 60 days, often more, before the county sheriff can publish a sale notice.

The practical effect is a longer pipeline of pre-foreclosure activity. Properties in active default sit in the court system for months before they appear at public auction. That pipeline is where the real opportunity lives for investors who know how to monitor it.

The district court foreclosure filing creates a public record. Investors who track these filings across Iowa's 99 counties can identify properties in the early stages of distress, often before the owner is aware the process has formally begun. By the time the sheriff publishes the auction notice, informed investors have already completed their due diligence.

Iowa's Redemption Period and What It Means for Bidders

After a sheriff sale concludes, Iowa grants the former property owner a redemption period during which they can reclaim the property by paying the winning bid amount plus interest and certain costs. This is a critical detail that changes how investors structure their offers.

The standard redemption period in Iowa is one year for most residential properties. However, Iowa code allows this period to be shortened in specific circumstances. Investors who understand the conditions that trigger early redemption rights can negotiate purchase contracts with redemption periods already built in, effectively locking in a below-market purchase price while the former owner exercises their legal right to buy back the property.

For investors targeting immediate cash-flow, this creates a strategic question: buy at auction and wait out the redemption period, or negotiate directly with the owner during the court process before the auction date?

Both approaches have merit depending on the county and the specific property. Properties in counties with high volume foreclosure dockets often move through the redemption period faster simply because court resources are more accustomed to processing these cases routinely.

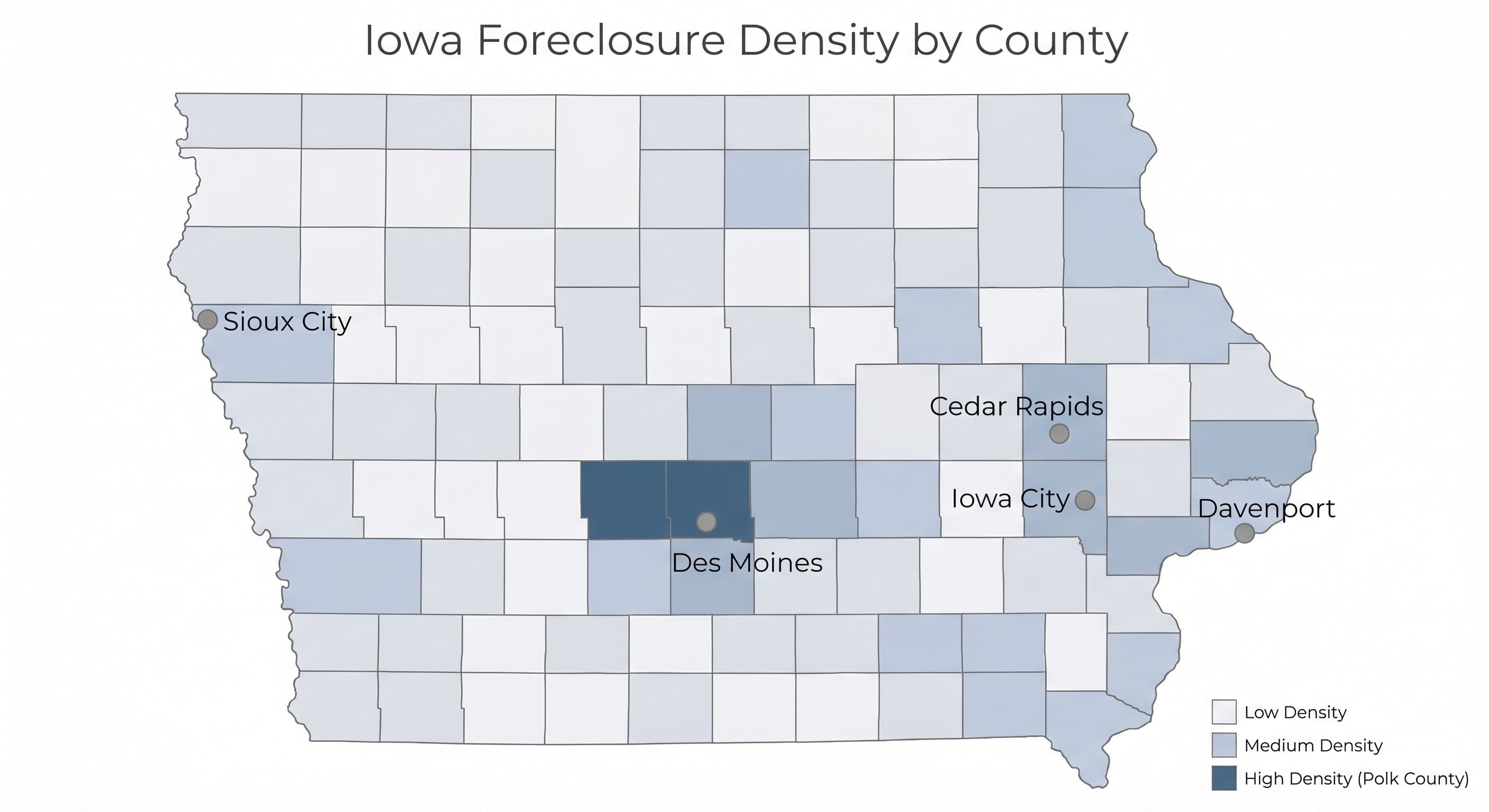

The County Structure: Where Iowa Foreclosure Leads Actually Cluster

Foreclosure activity in Iowa does not distribute evenly across the state. The pattern follows population and economic exposure.

Polk County, which includes Des Moines, consistently produces the highest volume of foreclosure filings in the state. Dallas, Linn, and Scott counties follow. These four counties account for a disproportionate share of Iowa's annual sheriff sales, meaning investors focused on volume should anchor their monitoring efforts there first.

Rural Iowa presents a different profile. Counties like Woodbury, Black Hawk, and Pottawattamie each show concentrated pockets of distress tied to agricultural economic cycles. Farm operators who suffered losses during periods of low commodity prices show up in these county foreclosure records with regularity. Agricultural zoned properties with residential structures represent a niche that national platforms frequently miss.

The DistressIQ platform monitors foreclosure filings and sheriff sale schedules across Iowa's county court systems, surfacing leads by signal type and location. For investors working multiple counties simultaneously, centralized data that spans the state's judicial structure makes it possible to compare opportunities across markets without manual court record monitoring.

Free Weekly Alerts

See What's Distressed in Your Market

Get free weekly alerts — new distressed properties, motivation scores, and hot neighborhoods in your area. Addresses and contact info available inside DistressIQ.

Free forever · No credit card · Unsubscribe anytime

The Sheriff Sale Process: What Happens at the Courthouse Steps

Iowa sheriff sales occur at the county courthouse and are conducted by the county sheriff's office. The property is sold to the highest qualified bidder. Unlike some states, Iowa does not require the winning bidder to have an outstanding mortgage balance that exceeds the property value. Cash bids are standard and preferred by trustees.

Key points for investors attending Iowa sheriff sales:

- Sales are typically scheduled on the first Monday of each month, though this varies by county and can be affected by court calendars.

- Winning bidders must tender payment immediately or within 24 hours. Financing contingencies are not accepted at the sale.

- The redemption period begins the moment the sale is confirmed by the sheriff.

- Properties sold at sheriff sale convey with the former owner's redemption rights intact unless specifically waived under Iowa code.

Investors who attend sales consistently develop relationships with county sheriff staff who manage the process. These relationships help with understanding the specific timeline mechanics for each county's current docket.

Tax Foreclosure in Iowa: A Parallel Acquisition Channel

Beyond the judicial mortgage foreclosure process, Iowa municipalities also pursue tax foreclosure on properties with delinquent property taxes. This operates on a separate timeline and separate court track.

Property tax foreclosure in Iowa follows the tax sale process defined under Iowa code. After a property fails to sell at the annual tax sale for non-payment of property taxes, the county can initiate a civil action to foreclose the tax lien. This path to ownership has different dynamics than mortgage foreclosure:

- The winning bidder at a tax sale is typically purchasing the property free and clear of most junior liens, subject to senior mortgage positions.

- Redemption periods on tax foreclosure follow different rules and timelines than mortgage foreclosure.

- The auction is administered by the county treasurer rather than the sheriff.

Investors who understand both channels have a significant advantage. A property that fails to sell at the mortgage foreclosure sheriff sale may still carry substantial tax delinquency, making it a candidate for the tax foreclosure track months later.

What Iowa Investors Need to Know About the Homestead Exemption

Iowa's homestead exemption affects foreclosure strategy in ways that are easy to overlook. Under Iowa law, homeowners may claim a homestead exemption that limits the amount of proceeds a lender can pursue from certain assets after a foreclosure sale. This can influence the total debt picture on a given property and the potential surplus available after the sale.

The exemption is most relevant when analyzing properties in higher-value neighborhoods where the loan balance significantly exceeds the current market value. In those cases, understanding how the exemption interacts with deficiency judgment rules affects whether an investor should expect additional complexity at closing.

For investor purposes, the practical takeaway is simple: always pull the homestead exemption status as part of the due diligence on any Iowa foreclosure lead. It changes the math.

Building an Iowa Foreclosure Leads Strategy in 2026

Iowa's judicial process is not the fastest in the country, but speed is not the only factor in investment returns. The additional time required to move a property from default filing to sheriff sale means less competition at the early research stage and more time to negotiate before auction day.

An effective approach for Iowa foreclosure leads in 2026 includes:

Monitor district court filings directly. Every foreclosure starts with a court filing. Iowa's district courts maintain public records that can be monitored by county. Investors who access these filings early can identify distressed properties 30 to 90 days before the sheriff publishes a sale notice.

Anchor monitoring on the Des Moines metro first. Polk and Dallas counties produce enough volume to keep an active investor busy year-round. Building a systematic approach in these markets before expanding statewide prevents spreading attention too thin.

Track tax-delinquent properties separately. The county treasurer's annual tax sale produces a distinct list of properties with no mortgage foreclosure activity. Combining both lists creates a fuller picture of the distressed inventory across any given county.

Factor redemption periods into every offer. Whether buying at sheriff sale or negotiating a direct purchase during the court process, the redemption timeline affects holding costs and exit strategy. Investors who account for this from the start avoid surprises after closing.

DistressIQ aggregates foreclosure leads across Iowa's county court and sheriff sale systems, combining mortgage foreclosure filings with tax delinquency records to present a unified view of distressed inventory. Investors can filter by signal type, county, estimated equity, and occupancy status to identify the properties most likely to match their acquisition criteria. Get started with Iowa foreclosure leads on DistressIQ at distressiq.ai.

Frequently Asked Questions

How long does foreclosure take in Iowa?

Iowa's judicial foreclosure process typically requires 6 to 12 months from the initial court filing to the sheriff sale, depending on the county's court docket volume and whether the borrower contests the action. This is longer than non-judicial states, where timelines are commonly 90 to 180 days.

Does Iowa have a redemption period after sheriff sale?

Yes. Iowa law grants the former property owner a redemption period of up to one year following the sheriff sale, subject to the property type and certain statutory conditions. Investors should account for this period before expecting clear title or possession.

Can investors attend Iowa sheriff sales?

Yes. Iowa sheriff sales are public proceedings held at the county courthouse. Bidders must present payment immediately following the sale confirmation. Investors should verify the specific sale schedule with the county sheriff's office, as schedules vary by county.

Are Iowa foreclosure properties subject to the homestead exemption?

The Iowa homestead exemption affects how proceeds are distributed after a foreclosure sale and can be relevant in deficiency judgment calculations. Investors should verify the exemption status during due diligence, particularly on properties where the loan balance approaches or exceeds market value.

What counties in Iowa have the most foreclosure activity?

Polk County (Des Moines metro) consistently leads the state in foreclosure volume, followed by Dallas, Linn, and Scott counties. Rural counties with agricultural exposure, including Woodbury and Black Hawk, show concentrated pockets of distress tied to commodity price cycles.

Can a property have both mortgage foreclosure and tax foreclosure activity?

Yes. A property with an active mortgage foreclosure can also carry delinquent property taxes. Tax foreclosure follows a separate legal track and timeline. Monitoring both channels provides a more complete picture of distressed inventory available for investment.

How do Iowa's foreclosure laws compare to neighboring states?

Iowa requires judicial foreclosure, while most neighboring states including Minnesota and parts of Illinois use non-judicial processes. This means Iowa timelines are typically longer but the court involvement creates a more structured public record that investors can monitor for early-stage leads.

Data in this article reflects publicly available county court records and sheriff sale schedules. Foreclosure timelines and redemption rules are subject to change based on Iowa statute and individual court circumstances. Investors should verify specific property status and applicable law with a licensed real estate attorney before making acquisition decisions.

The data behind this article

DistressIQ Monitors These Signals in Real Time

Pre-Foreclosures

NOD + NTS filings

Tax Delinquency

County treasurer records

Code Violations

Municipal inspection filings

Probate Filings

Superior Court records

Every lead is scored 0–100 for seller motivation based on signal type, duration, severity, and stacking. Nationwide coverage — every US county, updated daily.

Ready to find deals in your market?

See Live Distress Signals in Your County

Stop calling dead leads. Every lead in DistressIQ is scored 0–100 for seller motivation, with verified contact info included. Browse the free tier to see what's active in your market right now.

Browse Free Leads — No Credit Card