Pre-Foreclosure Homes: What Smart Investors Know That Generic List Buyers Don't

Pre-Foreclosure Homes: What Smart Investors Know That Generic List Buyers Don't

TL;DR: Pre-foreclosure homes sit in a 90 to 120-day window between Notice of Default filing and the public auction. With 40,534 foreclosure filings in January 2026 alone, up 32% year over year, the pipeline is the largest since 2019. The problem is not finding these properties , it is finding them fast enough to reach the homeowner while they are still willing to negotiate. Most investors buying pre-foreclosure lists are buying data that is already 45+ days stale. Investors who stack multiple distress signals per property and prioritize by motivation score close at rates that generic list buyers never see. The difference is not effort , it is data freshness and targeting specificity.

The Pre-Foreclosure Window Is Real, But the Lists Are Broken

Every investor who has bought a pre-foreclosure list and gotten two callbacks and a wrong number knows this feeling. The list looked promising. Hundreds of homeowners, all somewhere in the pre-foreclosure process, all theoretically reachable. But the phone numbers are bad, the properties are already under contract, or the homeowner worked something out with the lender three weeks ago and the list provider has not updated their data since.

That is not bad luck. That is a data problem.

Pre-foreclosure homes exist in a narrow window between the moment a homeowner misses enough payments for the lender to file a Notice of Default and the moment the property goes to public auction. In most states, that window runs 90 to 120 days. In some it is shorter. In judicial foreclosure states like New York or New Jersey, it can stretch to 12 to 18 months. The national average sits around 120 days from first missed payment to auction.

The opportunity is real. Foreclosure filings hit 40,534 in January 2026 alone, up 32% year over year, according to ATTOM Data Solutions. The pipeline of pre-foreclosure inventory is the largest it has been since 2019. Investors who have built reliable systems for sourcing these properties are seeing more deal flow than they have in years.

The problem is not conceptual. Everyone understands the pre-foreclosure window exists. The problem is operational. The data most investors are using to find pre-foreclosure homes is stale before it reaches their inbox.

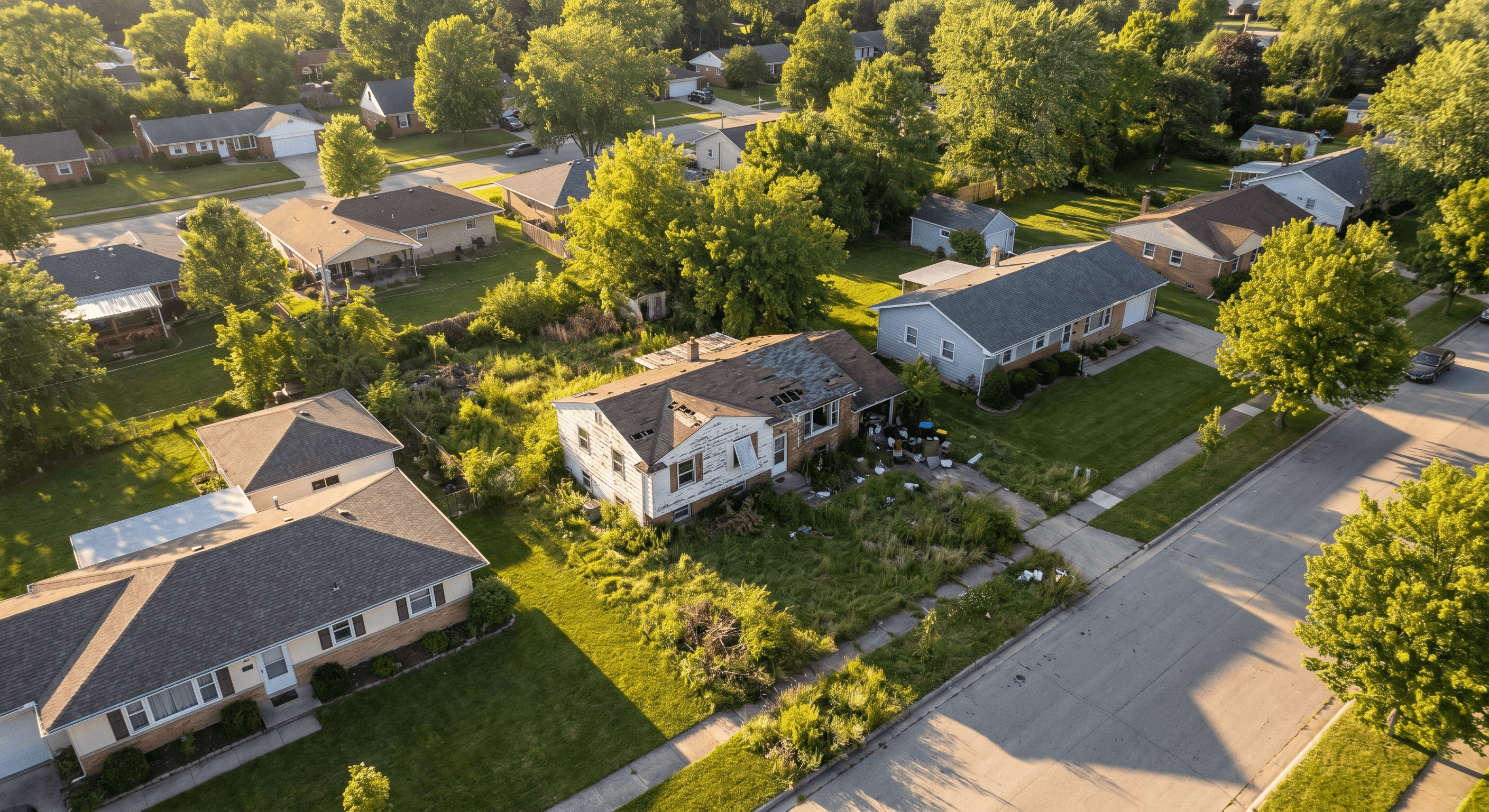

What a Pre-Foreclosure Home Actually Is

A pre-foreclosure home enters the process when a homeowner defaults on their mortgage. The lender files a Notice of Default with the county recorder , this is the formal trigger that launches the pre-foreclosure clock. The homeowner still owns the property. They still have the right to sell it, refinance it, or work out an agreement with the lender before the auction date.

This matters for investors because it is the only window in the entire foreclosure process where the homeowner has maximum motivation to negotiate and maximum ability to transact. After the auction, the bank owns it and the dynamics change entirely.

Most investors use "pre-foreclosure" and "short sale" interchangeably. They are not the same thing. A short sale is a negotiated sale where the lender agrees to accept less than the outstanding loan balance. A pre-foreclosure is a timeframe. A property can be in pre-foreclosure and qualify for a short sale, but the terms are not synonyms. A short sale is one possible outcome of the pre-foreclosure window. It is not the window itself.

Pre-foreclosure homes do not appear on MLS. The only way to find them is through public records , specifically, county recorder filings of Notices of Default and lis pendens notices. This is also why the data is so fragmented. There is no national database of pre-foreclosure filings. Each county maintains its own system, its own format, and its own update schedule.

Why Most Investors Never Reach the Right Pre-Foreclosure Homes

The most reliable way to find pre-foreclosure homes is to go directly to the county recorder or county clerk in each target market. Every Notice of Default filed in the United States is a matter of public record. In most states, the county recorder publishes these filings within days of submission.

The execution problem is brutal.

Tennessee has 95 counties. Florida has 67. Texas has 254. Building a manual research process across even the five most active counties in a state means navigating five different recorder websites, each with its own search interface, its own data export format, and its own update cadence. Some counties publish filing data in real time through an online portal. Others update a PDF docket once a week.

In smaller counties, the pre-foreclosure notice might run only in the local legal section of a weekly newspaper with 2,000 circulation and no website. Cross-referencing newspaper legal notices with county clerk records is how the most thorough investors build a complete picture of the pre-foreclosure market in rural areas. It is also slow enough that most investors never bother.

The result is that by the time a pre-foreclosure property appears on a free county search tool, by the time it gets aggregated into a list service database, by the time that list service sends you an email digest, the property has already been in the system for 45 to 60 days. The most motivated sellers have already received three postcards and two cold calls. The homeowner may have already worked out a forbearance with the lender or accepted that the auction is inevitable.

This is not an argument against pre-foreclosure investing. It is an argument about where the actual bottleneck is.

The bottleneck is not the concept of pre-foreclosure. The bottleneck is the speed and specificity of the data feeding your outreach. Investors who have solved this problem , who see new Notices of Default within days of filing, not weeks , are the ones closing pre-foreclosure deals at a rate that makes the strategy worthwhile.

Free Weekly Alerts

See What's Distressed in Your Market

Get free weekly alerts — new distressed properties, motivation scores, and hot neighborhoods in your area. Addresses and contact info available inside DistressIQ.

Free forever · No credit card · Unsubscribe anytime

What Signal Stacking Changes About Pre-Foreclosure Lead Quality

Pre-foreclosure investing at scale requires a filtering system. A single Notice of Default tells you a homeowner is behind on payments. It does not tell you whether they are likely to sell, whether they have any equity, whether they have other financial stress indicators, or whether they have already been contacted by three other investors this week.

This is why experienced pre-foreclosure investors do not treat every Notice of Default equally. They stack multiple distress signals per property.

A homeowner who has filed for bankruptcy, has a tax delinquency on the same property, and has a code violation open with the city is a categorically different lead than a homeowner who simply missed two payments because of a temporary job disruption. The multi-signal property is more likely to reach the auction stage, more likely to result in a motivated seller who needs to transact quickly, and more likely to close at a price that makes the deal work.

DistressIQ cross-references more than 20 signal types per property, including Notice of Default filings, lis pendens records, tax delinquency data, code enforcement violations, mortgage servicer transfer patterns, and ownership transfer history. Each property receives a motivation score from 0 to 100. The score reflects the density and recency of distress signals , not a gut feeling about whether a homeowner seems motivated.

The practical output for a pre-foreclosure investor is a ranked lead list instead of an unsorted database dump. Shelby County, Tennessee alone can have 200 to 400 properties in some stage of pre-foreclosure at any given time. Without a prioritization system, that volume is paralyzing. With a motivation score, the investor starts with the 10 to 15 properties that have the highest signal density and works down the list systematically.

How to Evaluate a Pre-Foreclosure Property Once You Find It

Finding the lead is the first step. Evaluating it correctly is where most investors either make money or lose it on a deal that looked better on paper.

Four factors determine whether a pre-foreclosure deal is worth pursuing.

Motivation density. The number and recency of distress signals on a property correlates directly with seller urgency. A Notice of Default filed 10 days ago combined with a tax delinquency is a more urgent lead than a Notice of Default filed 60 days ago with no other indicators. Signal recency matters as much as signal count.

Deal geometry. The math has to work. After-repair value minus outstanding loan balance minus estimated repair costs minus closing costs minus your profit margin must leave a number that justifies the risk. Pre-foreclosure properties sometimes carry back taxes, HOA liens, or code violation fees that are not visible in the initial lead data. A title search before contract is not optional , it is the step that prevents a $5,000 surprise from turning a profitable deal into a loss.

Title clarity. Properties in pre-foreclosure often have secondary liens, mechanic's liens, or IRS tax liens attached. These survive the foreclosure sale in many states and attach to the property in the hands of the new owner. A preliminary title report is the document that answers this question before you are contractually obligated.

Homeowner situation. This is the variable that does not appear in any database. Before calling, have a theory about why this homeowner is in distress. Job loss, divorce, medical debt, inherited property they cannot maintain , each scenario calls for a different conversation frame. Investors who understand the seller's specific situation negotiate more effectively than those who open with a generic pitch.

The Honest Case for Pre-Foreclosure Investing in 2026

The pre-foreclosure market in 2026 is larger than it has been in six years. Foreclosure filings have risen for 12 consecutive months. The pipeline of properties in the pre-foreclosure window is substantial. For investors with reliable data and a disciplined evaluation system, this is one of the strongest deal flow opportunities available.

For investors using generic pre-foreclosure lists bought from vendors who update their database every 30 to 60 days, it is a frustrating exercise in calling properties that are already under contract or whose owners have already resolved the situation. The difference in outcomes between these two groups has nothing to do with the quality of their phone calls or their negotiation skills. It has everything to do with the freshness and specificity of their data.

The investors closing pre-foreclosure deals consistently share one habit: they see new Notices of Default within days of filing, not weeks. They filter for signal density before they filter for geography. And they have a system for moving fast when they find a property that meets their criteria.

That system does not have to be manual. Platforms that aggregate county-direct filing data and apply motivation scoring across thousands of properties simultaneously give individual investors the same targeting capability that large wholesalers spend hundreds of thousands of dollars per year building internally.

Browse pre-foreclosure homes scored by motivation signal density , see which properties have the most distress indicators, not just a Notice of Default on file.

Frequently Asked Questions

What is a pre-foreclosure home?

A pre-foreclosure home is a property where the homeowner has defaulted on their mortgage and the lender has filed a Notice of Default with the county recorder, but the property has not yet gone to auction. The homeowner still owns the property and retains the legal right to sell it during this window. The pre-foreclosure window typically lasts 90 to 120 days from the filing of the Notice of Default, though this varies by state and can be shorter or significantly longer in judicial foreclosure states.

How is pre-foreclosure different from a short sale?

Pre-foreclosure is a timeframe in the foreclosure process. Short sale is a specific transaction type that can occur during that timeframe. In a short sale, the lender agrees to accept less than the outstanding loan balance as full payment when the property sells. A pre-foreclosure property may qualify for a short sale if the homeowner has equity and the lender approves the transaction before the auction date. Not all pre-foreclosure properties are short sales, and not all short sales occur during pre-foreclosure.

What is the difference between pre-foreclosure and a foreclosure auction?

Pre-foreclosure is the period before the auction when the homeowner still owns the property and may sell it to avoid foreclosure. A foreclosure auction is the public sale event where the property is sold to the highest bidder, typically at the county courthouse steps. At the auction stage, the bank owns the property (if no third party bids) and the previous owner's ability to negotiate directly with the buyer is eliminated. Pre-foreclosure deals happen before the auction with more flexibility on terms and inspection access.

Which states have the most pre-foreclosure activity?

As of early 2026, Texas, Florida, California, Georgia, Ohio, Illinois, Pennsylvania, New York, North Carolina, and Arizona generate the highest volume of pre-foreclosure filings. Shelby County, Tennessee; Harris County, Texas; Miami-Dade County, Florida; Maricopa County, Arizona; and Clark County, Nevada are consistently among the highest-volume individual counties for pre-foreclosure activity. States with non-judicial foreclosure processes like Texas and Tennessee tend to move through the pre-foreclosure window faster than judicial states like New York.

Can you finance a pre-foreclosure property?

Yes. Unlike auction purchases that typically require cash, pre-foreclosure transactions allow conventional financing, hard money loans, or other lending options because the transaction occurs before the property reverts to bank ownership. Financing depends on the property condition and the investor is financial profile. Properties in poor condition often require hard money or private money loans regardless of the purchase price. Conventional financing is generally only viable on properties in decent condition with sufficient equity to satisfy the loan-to-value requirements.

Why do some pre-foreclosure leads convert and others do not?

Pre-foreclosure leads convert when the homeowner has both the motivation to sell and the timeline pressure to act quickly. A Notice of Default alone is a weak signal , it tells you the homeowner missed payments, but not whether they are actively trying to avoid foreclosure. Properties with multiple overlapping distress signals , tax delinquency, code violations, bankruptcy filings, or an absentee owner , are significantly more likely to reach the auction stage and result in a motivated seller. Investors who filter by signal density rather than geography alone consistently see higher conversion rates from their pre-foreclosure outreach.

DistressIQ tracks pre-foreclosure filings across 3,200+ counties nationwide, updating daily from county recorder sources. Browse pre-foreclosure homes ranked by motivation score at distressiq.ai.

The data behind this article

DistressIQ Monitors These Signals in Real Time

Pre-Foreclosures

NOD + NTS filings

Tax Delinquency

County treasurer records

Code Violations

Municipal inspection filings

Probate Filings

Superior Court records

Every lead is scored 0–100 for seller motivation based on signal type, duration, severity, and stacking. Nationwide coverage — every US county, updated daily.

Ready to find deals in your market?

See Live Distress Signals in Your County

Stop calling dead leads. Every lead in DistressIQ is scored 0–100 for seller motivation, with verified contact info included. Browse the free tier to see what's active in your market right now.

Browse Free Leads — No Credit Card