Foreclosure Leads Washington: What Smart Investors Need to Know in 2026

Foreclosure Leads Washington: What Smart Investors Need to Know in 2026

TL;DR: Washington state uses a judicial foreclosure process that averages 7-11 months from default to auction, one of the longest timelines in the nation. King, Pierce, and Snohomish counties account for the majority of auction volume, but Clark, Spokane, and Kitsap counties offer underbid opportunities the Seattle metro misses. The key to finding actionable foreclosure leads in Washington is filtering by motivation score, not just filing date, since borrowers in the early-stage Notice of Default window are almost always more flexible on price than those already headed to auction.

Why Washington Is Different From the Rest of the Country

Every state runs foreclosure differently. Washington is one of just nine states that requires a court order to sell a property at auction. That sounds like a obstacle. For investors who know how to work the system, it creates a longer runway and more motivated sellers than non-judicial states.

In Texas or Nevada, a lender can push a property to auction in 60 days. In Washington, the process from first payment default to trustee sale typically takes seven to eleven months. That extended timeline means more opportunities to contact the borrower while they are still in pre-foreclosure, before the property ever reaches the courthouse steps.

The longer runway also means the data gap is wider. Most public-facing portals only show properties already scheduled for auction. By the time a deal appears on those lists, fifty other investors are already calling the same number. The real opportunity sits earlier in the process, in the lis pendens records that appear months before the auction date is set.

Washington also has no deficiency judgment protection for borrowers in non-recourse loans, which creates interesting dynamics for investors in certain counties. Borrowers facing a foreclosure judgment where the auction price does not cover the loan balance may be more motivated to do a short sale or private transaction, even when the property has technically moved past the pre-foreclosure window.

How Washington Foreclosures Actually Work

The process begins when a borrower misses three consecutive mortgage payments. The lender files a Notice of Default with the county auditor, which triggers a lis pendens notation in the public record. This is the first public signal that a property is in distress.

From the Notice of Default, Washington law requires the lender to wait a minimum of 30 days before scheduling a trustee sale. The trustee sale itself cannot occur on a weekend or legal holiday, and the property must be advertised in a newspaper of general circulation for three consecutive weeks before the auction.

For investors, this creates four distinct windows:

- Notice of Default (NOD) — File date is public record. Borrower is aware but lender has not yet set an auction date. Highest motivation window.

- Notice of Trustee Sale (NTS) — Auction date is set. Borrower knows the end is coming. Motivation still elevated but competition increases.

- Pre-auction period — Weeks before the scheduled sale, borrowers often become highly motivated to find a way out. This is where short sale negotiations or cash offers most commonly close.

- Auction (trustee sale) — Property hits the courthouse steps. Some investors specialize here, but the properties are typically sold as-is with no contingencies and require all-cash or hard money financing.

The key metric investors should track is days-to-auction, not just filing status. A property with an NTS filed today but an auction date sixty days out is fundamentally different from one with an auction in ten days. The first is still negotiable. The second is a race condition.

Where to Find Washington Foreclosure Leads

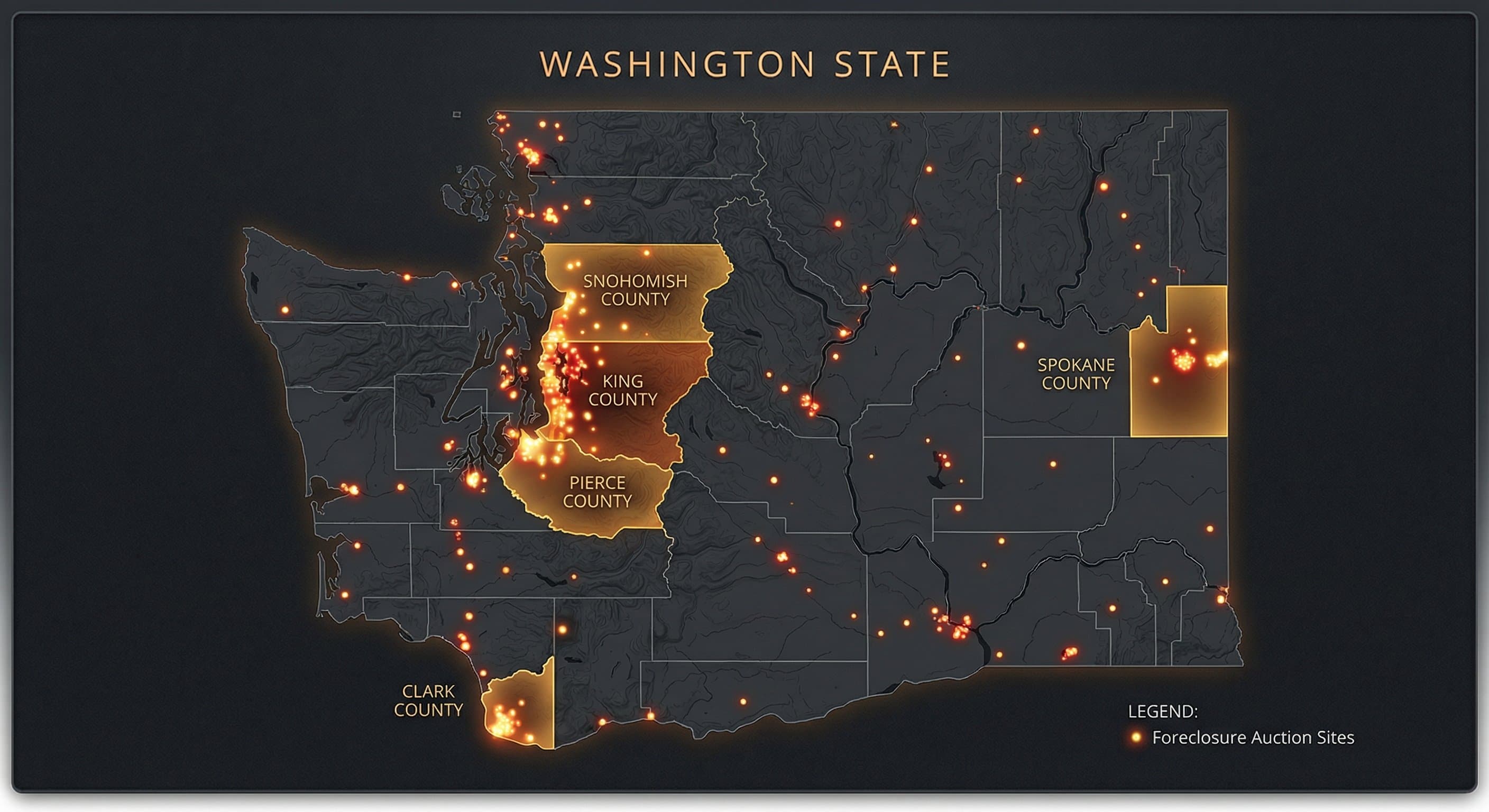

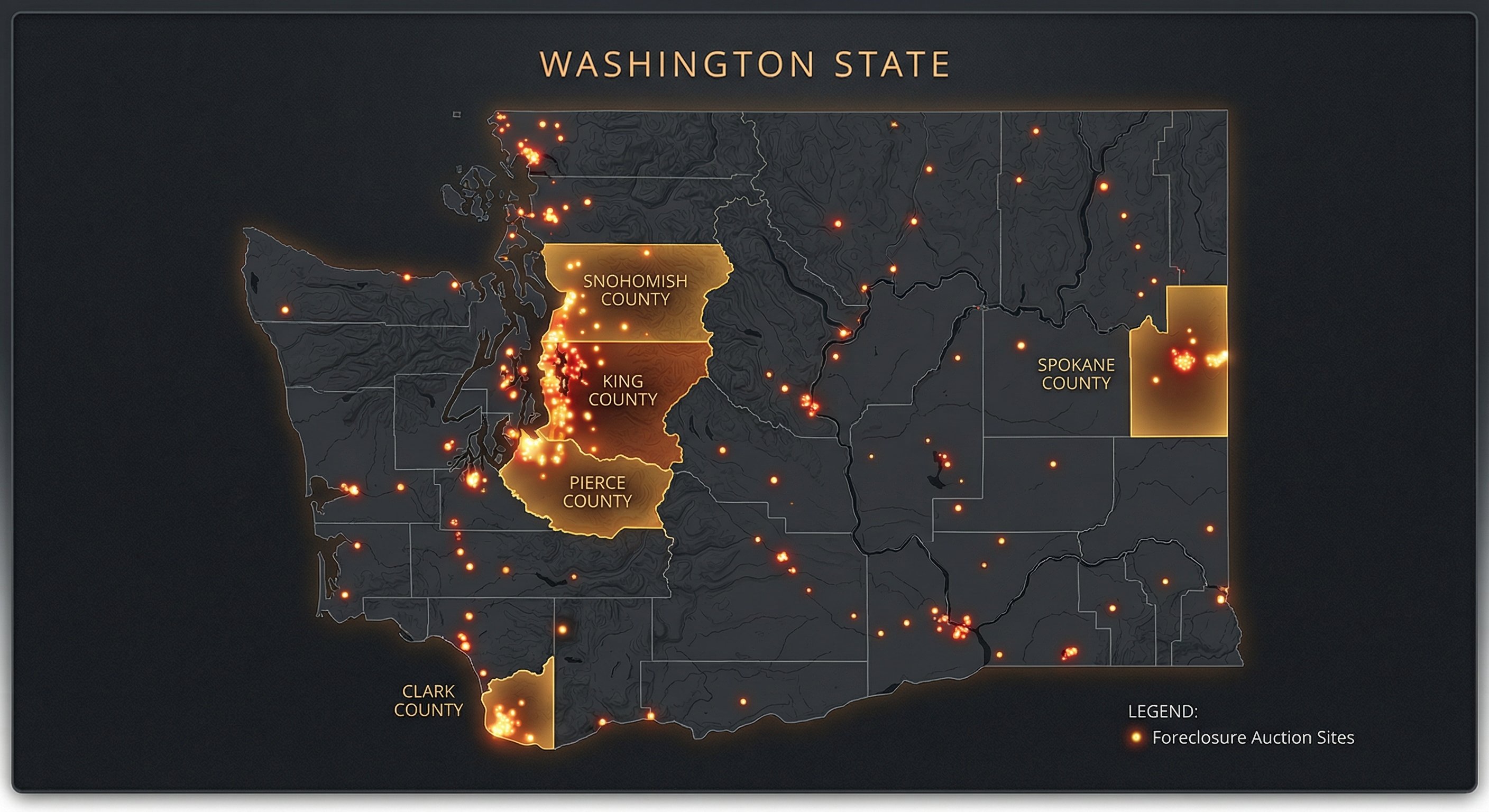

Washington has 39 counties, but the foreclosure volume concentrates in a handful. Understanding where the deals are, and which counties are underserved by active investors, is half the battle.

King County — Seattle, Bellevue, Renton. The highest volume county in the state. Properties here are expensive, which means more competition from institutional buyers but also more motivated sellers who need to offload a high-assessed-value property quickly. Median auction prices run 70-85% of assessed value. Strong demand for rental income means most investors here are hold-for-rent rather than fix-and-flip.

Pierce County — Tacoma, Puyallup, Lakewood. More approachable entry points than King County. Auction discounts tend to be deeper relative to ARV because retail investors focus on King and pass through Pierce. The county auditor publishes trustee sale calendars online. Tacoma's revitalization corridors (Hilltop, Eastside) offer concentrated opportunity zones.

Snohomish County — Everett, Lynnwood, Marysville. Second-highest volume after Pierce. Foreclosure inventory here tracks with Boeing employment cycles. When aerospace contracts tighten, foreclosure rates in north Snohomish County tick up predictably. Properties tend to be mid-century suburban stock, which renovates well for the build-for-rent strategy.

Clark County — Vancouver WA (the Portland metro side). High volume driven by population growth and the Interstate 5 corridor commute pattern. Foreclosures here compete with Portland-area buyers who cross the state line for Washington state income tax advantages. The Vancouver market is more sophisticated than investors outside the region assume, but auction deals still run 15-25% below comparable move-in ready properties.

Spokane County — Spokane and surrounding areas. The eastern Washington anchor. Significantly lower volumes than the western counties, but also significantly less competition. Properties here are older (many pre-1940s craftsman and foursquare homes) and often need more rehab than their western counterparts. The payoff per deal is smaller but the acquisition cost is lower and motivated seller situations are more genuine.

Kitsap County — Bremerton, Silverdale, Port Orchard. Severely underserved by active investors. The Bainbridge Island money keeps property values elevated relative to local incomes, which creates periodic waves of financial distress among commuters and service workers. Low competition from professional investors.

Free Weekly Alerts

See What's Distressed in Your Market

Get free weekly alerts — new distressed properties, motivation scores, and hot neighborhoods in your area. Addresses and contact info available inside DistressIQ.

Free forever · No credit card · Unsubscribe anytime

The Data Problem: Why Search Engines Keep Returning the Wrong Leads

Most investors start their Washington foreclosure search the same way: they Google "foreclosure homes Washington" or check Zillow's foreclosure filter. These sources show what is already listed as a foreclosure or REO (Real Estate Owned by the bank). By the time a property appears there, it has been picked over.

The actual distressed property data lives in county recorder filings. In Washington, those are the county auditor offices. Every Notice of Default, Notice of Trustee Sale, and bankruptcy filing involving real property is a public record that can be searched directly at the county level. The problem is that there are 39 counties, each with a different database interface, different search fields, and different fees for accessing bulk records.

Most investors solve this one of two ways. The first is a subscription to a national lead platform that aggregates county-level data nationally. The problem is that national aggregators update on weekly or monthly cycles, not daily. In a fast-moving market, a lis pendens filed on Monday can be scheduled for auction by Friday. By the time a weekly-updated platform reflects the new filing, the most motivated seller window has already passed.

The second approach is manual county-by-county research. This works for one or two counties, but Washington investors who try to manually track all 39 counties quickly discover the problem: incompatible interfaces, filing fees that add up, and no centralized way to rank leads by motivation. They end up with a spreadsheet full of names and no real prioritization signal.

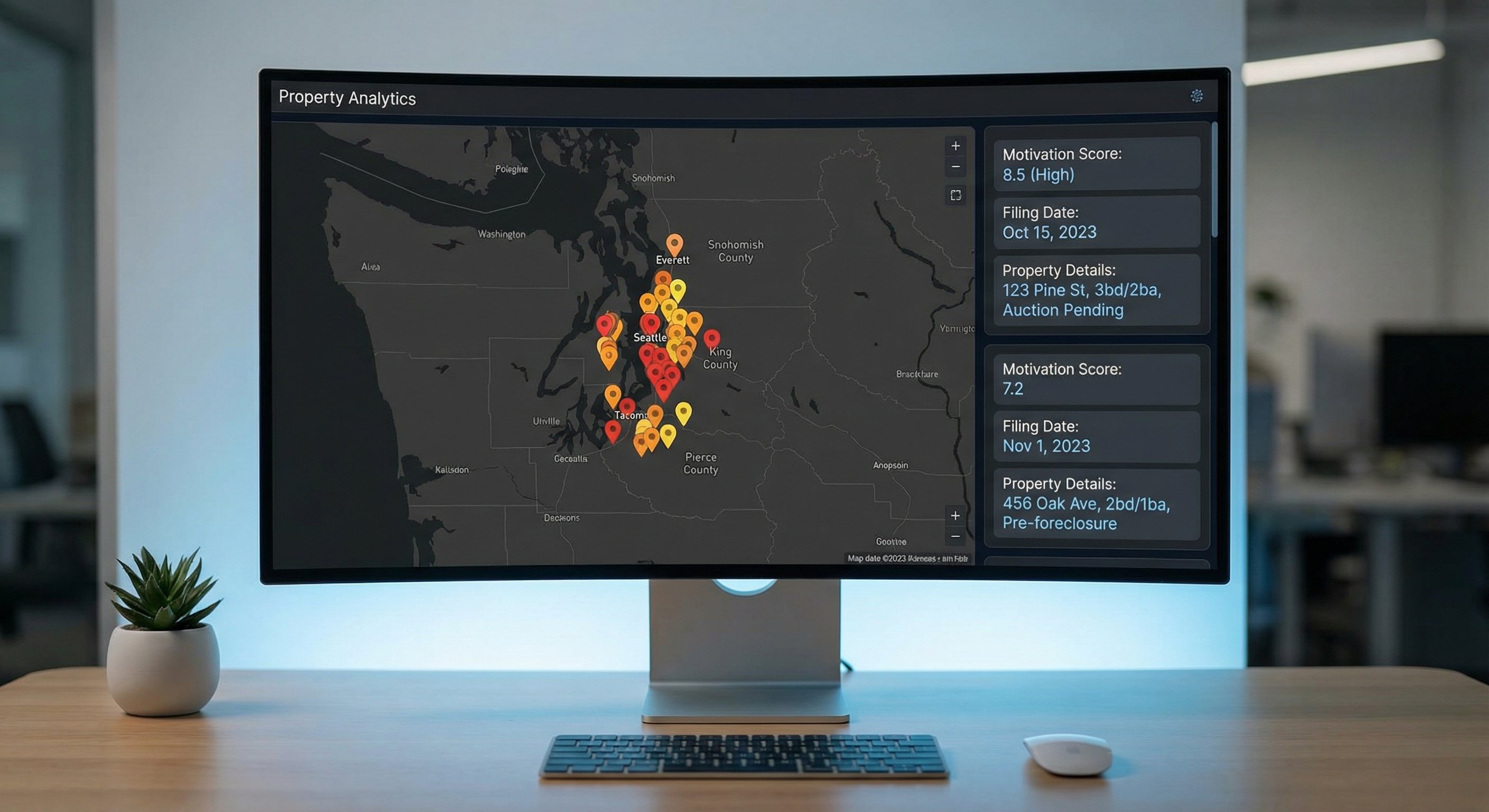

The investors getting the best results are the ones combining county-direct data feeds with a motivation scoring system. They know within the first week of a Notice of Default which borrowers are likely to respond to an offer and which ones are too far along to negotiate. That signal quality is what determines whether a deal closes or gets passed over for the next one.

What Motivated Sellers in Washington Actually Look Like

A foreclosure filing does not automatically mean a motivated seller. Washington borrowers in the early stages of default are often confused about their options, in active loss mitigation negotiations with their lender, or simply in a temporary financial crunch that resolves before the auction date. Reaching them early does not guarantee a deal.

The sellers worth pursuing are the ones who have already made the decision to sell but have not yet found a buyer. They have usually tried to work out a loan modification or short sale through their servicer, and they are now realizing the timeline is running out. They are often working with an agent who is trying to list the property at retail price, which means they are not yet in contact with the investor community.

Finding those sellers before their agent does, or finding them in the gap between when the agent gives up and when the auction date is set, is where the actual opportunity lives. The signal to watch is the Notice of Trustee Sale combined with a canceled short sale listing in the prior 90 days. That combination tells you the seller tried the traditional route, it did not work, and they are now on a fixed auction timeline with no backup plan.

DistressIQ tracks that combination across every Washington county, updated daily from county sources, so investors do not have to manually correlate cancelled listings with foreclosure filings across 39 different auditor databases.

Buying at Auction vs. Before Auction

Washington investors generally fall into two camps: auction buyers and pre-auction negotiators. Both strategies work. The decision depends on capital availability, renovation capacity, and risk tolerance.

Auction (trustee sale) strategy:

- Properties are purchased as-is, no inspections, no contingencies

- Payment is typically due at the auction in cash or certified funds

- Winning bidders must have financing arranged in advance or bring full cash

- Title issues are the primary risk, since the auction process does not clear liens from junior lienholders

- Auction buys work best for investors with a hard money line, contractor relationships for post-purchase rehab, and experience reading title reports before the sale

Pre-auction negotiation strategy:

- Properties are purchased before the auction date, typically through a direct offer to the borrower or a short sale negotiated with the lender

- The property can be inspected, financed conventionally, and the transaction handled through standard escrow

- The purchase price is usually higher than an auction discount, but the risk is lower and the exit timeline is more predictable

- Pre-auction deals work best for investors focused on hold-for-rent or moderate rehab, where the ARV spread does not require a deep auction discount to make the numbers work

Most experienced Washington investors prefer the pre-auction path for hold-for-rent deals (the numbers work without maximum discount) and reserve auction bids for properties that need significant structural work where the as-is auction price creates sufficient margin.

Washington Market Dynamics That Affect Your Strategy

Two factors are worth understanding before jumping into the Washington foreclosure market.

Seasonality — Foreclosure volumes in Washington spike in February and March each year, following the post-holiday financial crunch that hits lower-income borrowers hardest. Auction inventory peaks in late spring. Investors who want to buy at auction should be ready to bid in April through June when the most inventory is available. Investors who want to negotiate pre-auction should start outreach in December and January, when borrowers are most likely to be evaluating their options before the spring auction wave.

Remote work migration — The Pacific Northwest continues to attract buyers from California and New York who are relocating for quality of life and remote work flexibility. This has compressed cap rates in the Seattle metro and pushed many traditional fix-and-flip investors further south to Tacoma and south King County, where entry points are lower. Spokane has seen growing interest from investors who cannot afford the western Washington market but want Pacific Northwest exposure. Foreclosure inventory in Spokane is thinner but the buyer pool for renovated properties is growing.

Bottom Line

Washington's judicial foreclosure process rewards investors who understand the timeline, not just the filing status. The opportunity is not in finding foreclosure listings. It is in finding the borrowers who are motivated to sell before their auction date arrives, and having the data infrastructure to identify those sellers across 39 counties before the competition does.

The investors winning in Washington are the ones who monitor county-direct filings daily, score leads by motivation signal strength, and have the capital ready to move when the right property surfaces. The data edge is the only edge that matters in a market where every auction attendee has access to the same public trustee sale calendar.

See Washington foreclosure leads ranked by motivation score — browse verified distress signals across King, Pierce, Snohomish, Clark, and Spokane counties on DistressIQ →

Frequently Asked Questions

Q: How long does the foreclosure process take in Washington state?

Washington is a judicial foreclosure state, meaning lenders must go through the court system to obtain a sale order. From the first missed payment to the trustee sale, the process typically takes seven to eleven months. This is longer than non-judicial states like Texas or Nevada, but it creates a wider pre-foreclosure window where borrowers may be more flexible on price.

Q: Can I buy a foreclosed home before it goes to auction in Washington?

Yes. Many foreclosed properties in Washington are purchased through direct negotiation with the borrower or a short sale before the auction date. Pre-auction purchases allow for property inspections, conventional financing, and a cleaner title. The trade-off is that the purchase price is typically higher than the auction discount, so the strategy works best when the ARV spread still justifies the deal without maximum discount.

Q: What counties in Washington have the most foreclosure activity?

King County (Seattle metro) and Pierce County (Tacoma) account for the majority of Washington auction volume. Snohomish County (Everett) and Clark County (Vancouver) are the next most active. Spokane and Kitsap counties have lower volumes but also significantly less competition from professional investors.

Q: What is a lis pendens in Washington?

A lis pendens is a legal notice filed in the county recorder's office indicating that a property is involved in a lawsuit or foreclosure proceeding. In Washington, a lis pendens is automatically filed when a lender records a Notice of Default. This notice makes the pending action part of the public record and creates a cloud on the title until the case is resolved or the property is sold.

Q: Is Washington a deficiency judgment state?

Washington is a non-recourse state for purchase money loans, meaning lenders cannot pursue a deficiency judgment against the borrower if the auction price falls short of the loan balance. For investors, this means properties that go to auction are typically marketed at prices reflecting the lender's assessment of fair market value. Short sales and pre-auction negotiations with lenders are sometimes more complicated as a result, since the lender's negotiating position is constrained by the non-recourse rules.

Q: What does DistressIQ offer that public county records do not?

DistressIQ aggregates Notice of Default, Notice of Trustee Sale, and bankruptcy filings across all 39 Washington counties and updates them daily from county sources. The platform layers a motivation score on top of raw filing data, ranking leads by the likelihood that a seller will respond to an offer. Rather than manually tracking 39 different county auditor databases, investors can browse a prioritized list and click into any lead to see the property, the filing history, and assessor-verified characteristics in one place.

See Washington foreclosure leads ranked by motivation score — browse distressed properties across all Washington counties on DistressIQ →

The data behind this article

DistressIQ Monitors These Signals in Real Time

Pre-Foreclosures

NOD + NTS filings

Tax Delinquency

County treasurer records

Code Violations

Municipal inspection filings

Probate Filings

Superior Court records

Every lead is scored 0–100 for seller motivation based on signal type, duration, severity, and stacking. Nationwide coverage — every US county, updated daily.

Ready to find deals in your market?

See Live Distress Signals in Washington

Stop calling dead leads. Every lead in DistressIQ is scored 0–100 for seller motivation, with verified contact info included. Browse the free tier to see what's active in your market right now.

Browse Free Leads — No Credit Card