How to Find Foreclosure Leads in North Carolina (2026 Investor Guide)

How to Find Foreclosure Leads in North Carolina (2026 Investor Guide)

TL;DR: North Carolina processes foreclosures through a hybrid "special proceeding" governed by General Statutes Section 45-21, routing cases through the Clerk of Superior Court rather than a full civil trial. The process runs 60 to 120 days total, faster than full judicial states but slower than pure non-judicial markets. Two windows matter for investors: the pre-hearing filing stage, when leads first become public, and the 10-day upset bid period after auction, a mechanism unique to NC that lets any third party outbid the auction winner by 5 percent. This guide covers the timeline, the top counties by volume, and the strategies that produce consistent deal flow.

North Carolina does not run foreclosures the way most investors expect. The state uses a hybrid process called a "special proceeding," sitting between full judicial foreclosure and pure non-judicial power of sale. Cases move through the Clerk of Superior Court, not a judge's trial docket. No jury, no discovery phase, no multi-year timeline. The Clerk hears the matter, authorizes the sale, and the property moves to auction within 60 to 120 days.

That compressed timeline makes these leads both valuable and time-sensitive. An investor who identifies a property at the right stage can move before the competition knows the filing exists.

The NC Foreclosure Timeline

Understanding the mechanics is the foundation for finding deals. Here is how a North Carolina foreclosure moves through the system.

Default. The borrower falls behind on payments, typically 90+ days. Not yet public record, but approaching defaults often show early signals: tax delinquency, code violations, water shutoffs.

Notice of Hearing. The lender files with the Clerk of Superior Court. This is public from the moment it hits the docket and includes the property address, owner name, lender name, and the hearing date, typically 10 to 30 days out. The single most important lead signal in NC.

Clerk's Hearing. The Clerk reviews the filing and determines whether the lender has the right to foreclose. If the debt is valid and in default, the sale is authorized.

Notice of Sale. Posted and published for at least two weeks before the auction date.

Foreclosure Sale. Public auction at the courthouse steps or online in larger counties.

10-Day Upset Bid Period. The sale is not final for 10 calendar days. Any third party can file an upset bid exceeding the winning bid by at least 5 percent, minimum $750. If an upset bid comes in, the clock resets. The cycle continues until a full 10-day period passes with no competing bid.

Deed Transfer. The deed transfers. NC has no statutory right of redemption.

Where to Find NC Foreclosure Leads

The Notice of Hearing filing is the earliest point at which a foreclosure becomes public. Every investor should track these filings. The question is how.

County clerk portals. Each of NC's 100 counties maintains its own case system. Mecklenburg provides online lookup. Wake uses eFile. Guilford and Forsyth have their own portals. Searching all 100 individually is slow and many are not updated in real time.

Legal notices. The Notice of Sale is published in a local newspaper, arriving weeks after the Notice of Hearing. Investors relying only on published notices are already behind.

Aggregated platforms. Services that pull filings from county-verified sources into a single feed eliminate manual searching. When the platform layers additional distress signals, the leads become more actionable than a raw case number.

The best NC investors stack signals: a Notice of Hearing plus tax delinquency plus a code violation plus absentee ownership. Each layer raises the probability the homeowner is genuinely motivated.

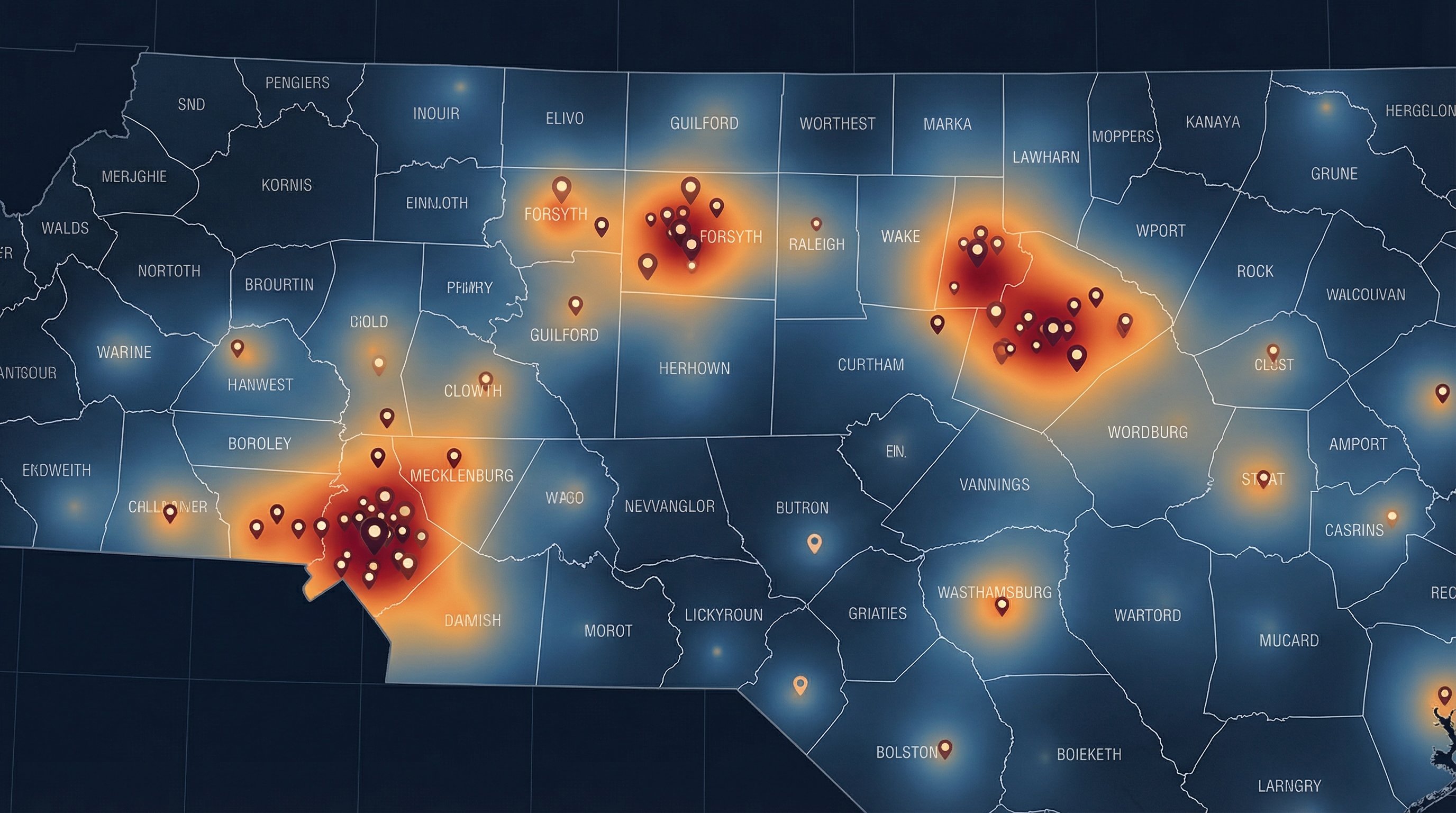

The Five Highest-Volume Counties

Not all 100 NC counties produce the same deal flow. Here is where foreclosure activity concentrates.

Mecklenburg (Charlotte). The largest county by population. High loan balances mean more distress when employment shifts or rates reset. The Mecklenburg Clerk processes one of the highest foreclosure volumes in the state. Outer suburbs like Steele Creek and Huntersville offer straightforward single-family opportunities.

Wake (Raleigh). Rising property taxes and cost of living have pushed some homeowners into default. Per-capita volume is lower than Mecklenburg, but property values are higher, which matters for ARV math. Courthouse-step competition is intense here, making pre-foreclosure leads especially valuable.

Guilford (Greensboro and High Point). Underrated for foreclosure investors. Lower price points, solid rental demand from UNCG and NC A&T, meaningful volume, and less competition than Charlotte or Raleigh. Older housing stock creates more rehab opportunity and stronger flip margins.

Forsyth (Winston-Salem). Mid-sized market, older housing, less investor saturation. Outer neighborhoods offer foreclosure opportunities at price points that work for wholesale and fix-and-flip.

Cumberland (Fayetteville). A military market driven by Fort Liberty's transient population. Steady volume from PCS moves and deployment-related income disruptions. Lighter competition and lower price points, but consistent deal flow.

Free Weekly Alerts

See What's Distressed in Your Market

Get free weekly alerts — new distressed properties, motivation scores, and hot neighborhoods in your area. Addresses and contact info available inside DistressIQ.

Free forever · No credit card · Unsubscribe anytime

The Upset Bid Strategy

The 10-day upset bid period creates an opportunity that exists in almost no other state. Two strategies take advantage of it.

The first is direct auction bidding. Show up, compete, win. The risk: someone can file an upset bid for 10 days, so the purchase is not final until that window closes.

The second is more surgical. Monitor auction results, identify properties that sold below market value, and submit an upset bid on the ones that fit. This skips auction-day frenzy and reduces competition to a single opposing bidder, at a cost of only 5 percent more than the winning price.

Neither strategy works without data on what sold, for how much, and when the upset bid window opens.

Signal Stacking: Prioritize the Right Leads

A Notice of Hearing filing tells you a property is in trouble. It does not tell you whether the homeowner wants to sell or whether the property is worth pursuing. Signal stacking solves this.

Notice of Hearing plus tax delinquency means the owner is behind on both the mortgage and taxes, indicating severe distress. Notice of Hearing plus code violations suggests lender and city pressure are both mounting. Notice of Hearing plus vacancy plus absentee ownership often points to an inherited property or a distant rental, resulting in negotiated pre-foreclosure purchases.

Every additional signal makes the lead more actionable and reduces time spent on dead ends.

Working Leads: The Practical Playbook

Contact within 48 hours of the Notice of Hearing filing. Earlier contact means more options for the homeowner and less defensiveness. A homeowner two weeks from the hearing date is harder to reach than one who just received notice.

Lead with empathy, not an offer. Explain that you work with homeowners who need to sell quickly and ask whether a conversation would help.

Know the ARV and MAO before the first call. After-repair value, repair estimate, and maximum allowable offer should be calculated before dialing.

Track the hearing date for follow-up. If initial contact does not produce a deal, reach out again three to five days before the hearing.

Key Legal Points

No post-sale redemption. Once the upset bid period closes, the deed transfers cleanly. This eliminates a risk that investors in states like Minnesota or Michigan must carry.

Deficiency judgments are limited. Section 45-21.38 restricts them on purchase money mortgages, affecting how lenders approach workout negotiations and how motivated sellers are to cooperate with a short sale.

Pre-sale right to cure. Homeowners can pay off the full mortgage balance plus costs at any point before the sale to stop the process. Even late-stage leads can fall through, which is why speed of contact matters.

FAQ

Q: How long does the foreclosure process take in North Carolina?

Most NC foreclosures run 60 to 120 days from the Notice of Hearing filing to final deed transfer. The timeline depends on whether the homeowner contests the hearing, how quickly the county schedules the sale, and whether upset bids extend the post-auction window. The special proceeding format keeps even disputed cases moving faster than full judicial states, where filings can sit on a trial docket for over a year.

Q: What is the 10-day upset bid period in North Carolina?

After a property sells at a NC foreclosure auction, the sale does not become final for 10 calendar days. During this window, any party can submit an upset bid exceeding the winning bid by at least 5 percent, with a minimum increase of $750. If an upset bid is filed, a new 10-day period opens. The process repeats until a full 10-day period passes with no competing bid. This mechanism is unique to North Carolina and creates a second acquisition opportunity most out-of-state investors do not know exists.

Q: Where can you find NC foreclosure filings?

Foreclosure Notices of Hearing are filed with the Clerk of Superior Court in the property's county. Many counties offer online access, though each of NC's 100 counties operates a different portal. Aggregated platforms pulling from county-verified sources provide a more practical solution for investors tracking multiple counties simultaneously.

Q: Does North Carolina have a post-sale redemption period?

No. Once the 10-day upset bid period closes without a competing bid, the deed transfers and the former owner has no legal mechanism to reclaim the property. This is a significant advantage compared to states like Minnesota, where redemption periods can extend six months or more after the sale, creating prolonged uncertainty for the buyer.

Q: Which North Carolina counties have the most foreclosure activity?

Mecklenburg County (Charlotte) leads by raw volume due to population size and loan count. Wake County (Raleigh), Guilford County (Greensboro), Forsyth County (Winston-Salem), and Cumberland County (Fayetteville) also generate meaningful volume. Smaller counties like Gaston, Rowan, and Craven sometimes post higher per-capita rates with less investor competition.

Q: What is a "special proceeding" foreclosure in NC?

A special proceeding is NC's hybrid foreclosure process, governed by General Statutes Section 45-21. It is not a full civil lawsuit. The lender files a notice of hearing with the Clerk of Superior Court, who conducts a ministerial review to confirm the debt is valid and in default. If authorized, the property moves to auction without entering a judge's trial docket. The result is a faster timeline than full judicial foreclosure, with more procedural safeguards than pure non-judicial states.

Q: Is it better to buy at auction or submit an upset bid?

Both strategies have merit depending on investor goals. Buying at auction gives the first shot at a competitive price but carries the risk of being outbid during the 10-day upset bid window. Submitting an upset bid after the auction skips day-of competition but costs at least 5 percent more. Investors with strong conviction on value often prefer the auction. Those who want less competition prefer the upset bid route.

For investors ready to stop pulling courthouse records manually from 100 NC county websites, DistressIQ aggregates foreclosure filings, tax delinquency records, code violations, and 28 other signal types across all of North Carolina's counties, updated daily from county-verified sources. Filter by county, zip code, or signal stack. See Street View and aerial imagery on every lead. Start finding foreclosure leads at distressiq.ai.

Sources

- North Carolina General Statutes Section 45-21 (Foreclosure of Mortgages and Deeds of Trust)

- ATTOM Data Solutions U.S. Foreclosure Market Report

- N.C. Judicial Branch Clerk of Superior Court Special Proceedings Procedures

The data behind this article

DistressIQ Monitors These Signals in Real Time

Pre-Foreclosures

NOD + NTS filings

Tax Delinquency

County treasurer records

Code Violations

Municipal inspection filings

Probate Filings

Superior Court records

Every lead is scored 0–100 for seller motivation based on signal type, duration, severity, and stacking. Nationwide coverage — every US county, updated daily.

Ready to find deals in your market?

See Live Distress Signals in Your County

Stop calling dead leads. Every lead in DistressIQ is scored 0–100 for seller motivation, with verified contact info included. Browse the free tier to see what's active in your market right now.

Browse Free Leads — No Credit Card