Foreclosure Leads New Mexico: What Smart Investors Miss About the Land of Enchantment

Foreclosure Leads New Mexico: What Smart Investors Miss About the Land of Enchantment

TL;DR: New Mexico runs judicial foreclosures through 13 district courts, taking a minimum of 360 days from filing to auction. That timeline is a feature for investors who move early. The state's mechanics' lien priority rule means property acquired at distressed prices can carry hidden title complications from contractor work performed years earlier. Albuquerque, Doña Ana, and Bernalillo counties generate the most foreclosure volume. The real edge comes from sourcing leads before the court process surfaces them publicly — DistressIQ tracks distressed properties across all 33 counties with daily county-direct data.

Most Investors Get New Mexico Wrong Because They Do Not Understand the Court System

There is a reason New Mexico does not show up on every real estate investor's target list. It is not Arizona's massive tax lien auctions. It is not California's foreclosure volume. It is not Nevada's turnaround speed. New Mexico has a slow, court-supervised process that punishes investors who treat it like a typical non-judicial state.

That punishment comes in the form of missed opportunities and bad assumptions.

New Mexico is a judicial foreclosure state. Every residential foreclosure goes through the district court in the county where the property sits. There is no trustee sale mechanism. There is no power-of-sale shortcut. The lender files a complaint, the court oversees the process, a special master conducts the auction, and the court confirms the sale. The shortest path from initial default to completed auction runs roughly 360 days. In practice, contested cases or properties with multiple lienholders can stretch 18 months or longer.

This is actually good news for investors who understand it. A slower foreclosure process means more time to identify motivated sellers and negotiate a direct purchase before the auction. It also means more time for the distress signals to compound. A homeowner who has been in default for 120 days in New Mexico is still months from a public auction date. That homeowner is stressed, exposed, and often willing to sell at a discount that reflects the reality of their situation.

The investors who do well in New Mexico are the ones who think in terms of district court timelines instead of auction calendars. They are calling homeowners during the complaint-filing window, not showing up at the courthouse steps on sale day.

The Three Things That Make New Mexico Different for Real Estate Investors

1. Judicial Foreclosure Means District Court Records Are Your Starting Point

In non-judicial states, the Notice of Default gets recorded at the county recorder and the sale date is set according to statute. The information is public quickly. In New Mexico, the process starts when the lender files a complaint in district court. That filing creates a court record that is searchable but not as immediately visible to casual observers as a recorded NOD in Arizona or California.

The practical implication is that accessing foreclosure leads in New Mexico requires monitoring district court filings, not just county recorder databases. The county assessor and recorder still matter for ownership records, mortgage data, and property characteristics, but the foreclosure trigger is the court complaint.

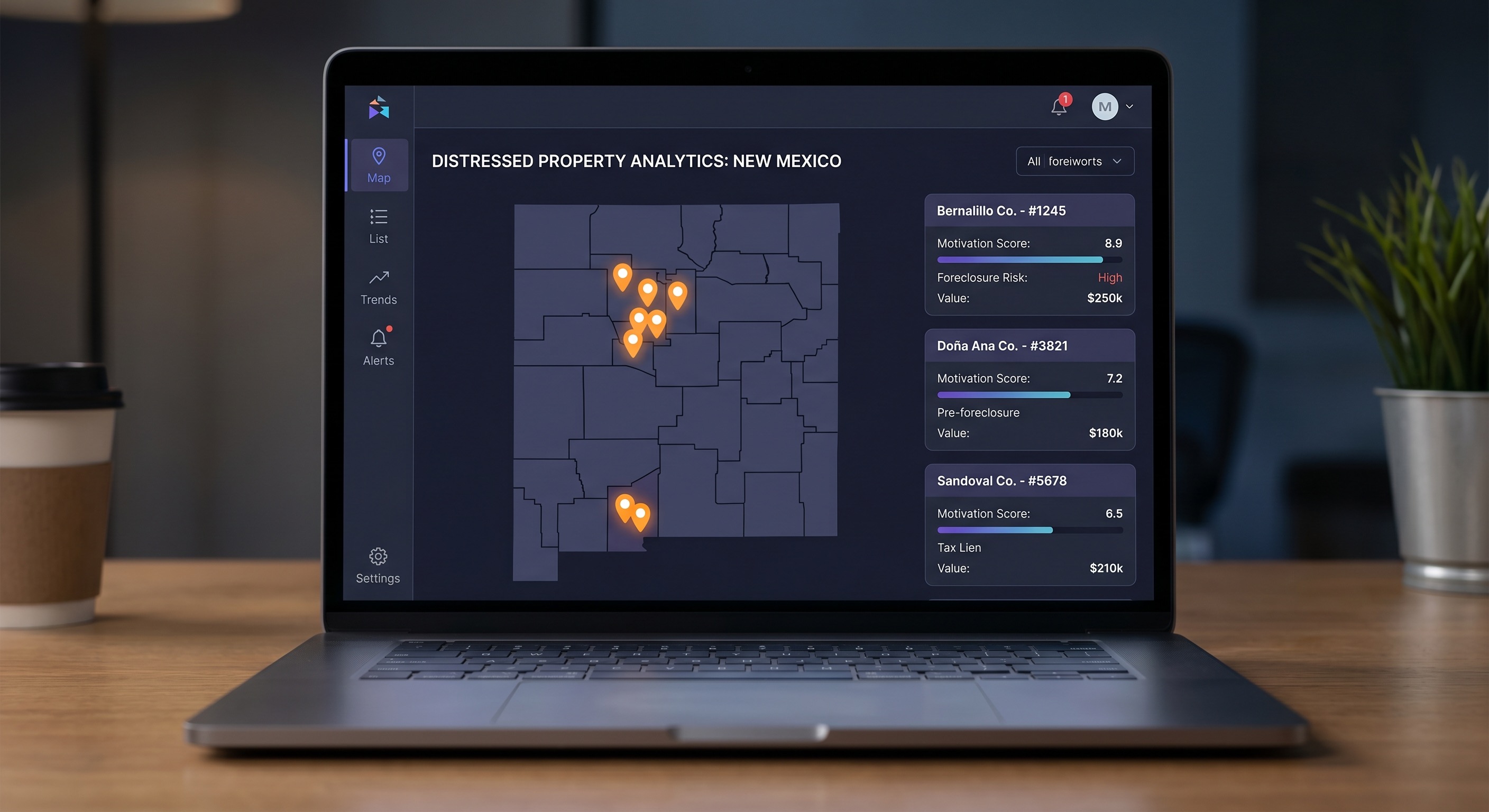

Bernalillo County (Albuquerque) and Doña Ana County (Las Cruces) handle the highest foreclosure volume in the state. Third is Sandoval County, which has absorbed significant Albuquerque metro growth over the past decade and shows active distress signals in the distressed-property data.

2. Mechanics' Lien Priority Can Complicate Your Title

This is the one New Mexico rule that surprises even experienced investors from other states. Under New Mexico law, a mechanics' lien relates back to the date visible construction commenced, not the date it was recorded. This means a contractor who worked on a property in 2022 can file a mechanics' lien in 2026 and, if properly documented, hold a priority position over a mortgage recorded after construction began.

For an investor acquiring a foreclosed property, this creates a title risk that does not exist in most other states. The property may have had contractor work performed years before the current default, and those lien claims can survive a foreclosure sale depending on their priority relative to the foreclosing lender's mortgage.

The mitigation approach is straightforward: run a full lien search including mechanics' lien filings before closing on any New Mexico distressed property. Properties with visible construction activity or recent renovation permits are the ones to scrutinize most carefully. This is not a reason to avoid New Mexico distressed properties. It is a reason to do title due diligence before closing rather than after.

3. HOA and Condo Association Liens Do Not Have Super-Priority Here

Some states give HOA liens a super-priority position that lets them prime a first mortgage in a foreclosure. New Mexico does not. HOA and condo association liens are treated like ordinary judgment liens. The first mortgage holder's position is protected ahead of HOA assessments in most scenarios. This matters for investors targeting distressed single-family homes in HOA communities or condo developments in the Albuquerque metro area.

How to Find Foreclosure Leads in New Mexico Before the Auction

The public foreclosure record in New Mexico runs through district court filings. A complaint for foreclosure is filed in the judicial district where the property is located. New Mexico has 13 judicial districts covering the state's 33 counties. Monitoring these filings systematically requires either direct court database access or a platform that aggregates court data across districts.

DistressIQ pulls distressed property signals across all New Mexico counties, aggregating pre-foreclosure activity, tax delinquency records, and code violation data into a single lead list sorted by motivation score. For investors targeting Albuquerque foreclosure leads specifically, Bernalillo and Sandoval counties offer the metro market volume. For rural land plays, Rio Arriba and San Juan counties have historically produced distressed agricultural property activity tied to drought conditions and economic pressure on small farms.

The key signal to watch in New Mexico is the combination of pre-foreclosure filing plus tax delinquency. A homeowner who has fallen behind on mortgage payments and also has delinquent property taxes is under pressure on two fronts simultaneously. The motivation to sell before auction is higher, and the negotiating discount an investor can access is deeper.

Free Weekly Alerts

See What's Distressed in Your Market

Get free weekly alerts — new distressed properties, motivation scores, and hot neighborhoods in your area. Addresses and contact info available inside DistressIQ.

Free forever · No credit card · Unsubscribe anytime

New Mexico Foreclosure Timelines: What the Numbers Actually Mean

The 360-day minimum timeline is real, but it is an average that masks significant variation by county and case complexity.

For a straightforward single-family residence with a clear first mortgage and no junior liens, the path from lender complaint to court-confirmed sale typically runs 10 to 14 months in Bernalillo County. The lender files the complaint, the court sets a settlement conference, and if no resolution occurs, the court enters judgment and orders the sale. The special master conducts the auction and the court confirms the sale within 30 days.

For properties with multiple lienholders, contested cases, or borrower bankruptcy filings, the timeline extends to 18 months or longer. This extended timeline is where the investor advantage lives. Properties that are publicly listed as being in pre-foreclosure have already been through the initial filing phase. The homeowner is six to nine months from a potential auction date at that point. This is the window for direct purchase negotiations.

The settlement conference requirement in New Mexico judicial foreclosures is also worth understanding. Under NMSA 1978 Section 48-10-1, the court can appoint a settlement facilitator to explore alternatives between the lender and borrower. This process typically runs 60 to 90 days. Investors who are monitoring court filings can sometimes insert themselves into this window by making a cash offer directly to the homeowner contingent on the property being pulled from the foreclosure process.

Which New Mexico Counties Have the Most Foreclosure Activity

Bernalillo County accounts for roughly 45 percent of the state's annual foreclosure volume. The Albuquerque metro market has the population density to support distressed property activity. Median home prices in the city have remained relatively accessible compared to other western metros, which means a distressed single-family home in the $180,000 to $280,000 range is a realistic acquisition target for fix-and-flip or buy-and-hold investors.

Doña Ana County, centered on Las Cruces, generates the second-highest volume. It has benefited from relocations from more expensive California and Arizona markets, but the county still produces distressed inventory tied to older subdivisions built during the 2000s boom that never fully stabilized.

Sandoval County is the fast-growing Albuquerque suburb market. Its foreclosure volume has risen as new communities established during the mid-2010s encounter the same economic pressures that hit metro markets elsewhere.

Rural counties with persistent foreclosure activity include San Juan County (Farmington area) and Rio Arriba, both tied to extractive economy cycles. These markets have lower volume but also lower competition from institutional investors.

New Mexico Distressed Properties: Signal Stacking for Higher Motivation

A property that is only in pre-foreclosure has a motivated seller. A property that is both pre-foreclosure and tax delinquent has a seller under pressure from two directions simultaneously. A property that is tax delinquent, pre-foreclosure, and vacant has a seller who has already stopped maintaining the property and is likely highly motivated to close a transaction quickly.

The motivation score approach works by stacking these signals. A property in Albuquerque with a pre-foreclosure filing and an open code violation from city inspection is a different category of motivated seller than a property with just a single pre-foreclosure signal. The investor who calls the highest-scored properties first is reaching the most motivated sellers before competitors do.

Vacant properties show up in New Mexico city and county records when utility companies flag an account as inactive. A property that is both pre-foreclosure and vacant is often an investor acquisition candidate where the homeowner has already moved out and is not actively maintaining the property. These tend to sell below market value faster than occupied distressed properties because the holding costs for the homeowner have become unsustainable.

New Mexico vs. Neighboring States: Why This Market Is Worth Knowing

Texas runs non-judicial foreclosures through a deed of trust structure with trustee sales. The timeline from default to auction is often 90 days or less in straightforward cases. Fast timelines mean less negotiating window for investors.

Arizona is a trustee-sale state with relatively fast auctions and a massive tax lien system through Maricopa County. The competition for tax lien certificates at auction has driven down effective yields to the point where deep-discount acquisitions require buying before the auction rather than at it.

New Mexico's 360-day judicial timeline gives investors the opposite of those two markets: more time, slower process, more negotiation window, and fewer institutional competitors actively working the distressed property pipeline. The market is not inactive. It is just operating on a different clock.

For investors who are comfortable with a longer deal timeline and want to avoid the competitive intensity of the Arizona tax lien market or the Texas trustee sale auctions, New Mexico distressed properties represent one of the more overlooked entry points in the Southwest.

Quick Comparison: Judicial vs. Non-Judicial Foreclosure States

| Factor | New Mexico (Judicial) | Arizona (Trustee Sale) | Texas (Non-Judicial) |

|---|---|---|---|

| Timeline | 360+ days | 90-120 days | 60-90 days |

| Court involvement | Full district court process | No court required | No court required |

| Auction mechanism | Special master conducted | Trustee sale | Substitute trustee sale |

| Investor access window | Long (most negotiating room) | Short | Shortest |

| Competition intensity | Low-moderate | High | High |

| Title risk | Mechanics' lien priority | Standard | Standard |

| Settlement conference | Required in most districts | Not applicable | Not applicable |

What to Do Right Now

If you are already operating in New Mexico and not finding distressed property leads, the most likely problem is the data source. County assessor data, court filings, and recorder documents are all public, but they are not centralized. A platform that pulls from district court filings and county assessor records across all 33 counties is the practical solution for systematic sourcing.

If you are considering New Mexico for the first time, the entry point is Bernalillo County. The volume is sufficient to run a systematic acquisition strategy without the intensity of competing against institutional buyers. Do not try to time the auction. Call homeowners during the pre-foreclosure window, which can stretch 6 to 9 months before a court filing converts the process to a public record.

Find New Mexico foreclosure leads by county — DistressIQ tracks distressed properties across all 33 New Mexico counties, updated daily with motivation scores that stack pre-foreclosure, tax delinquency, and vacancy signals. Browse Bernalillo, Doña Ana, and Sandoval County leads first. Try DistressIQ free on DistressIQ →

The investors winning in New Mexico are not the ones who move the fastest on auction day. They are the ones who have relationships with distressed homeowners before the public record exists. Build that sourcing system first.

Frequently Asked Questions

How long does foreclosure take in New Mexico?

New Mexico judicial foreclosures run a minimum of 360 days from lender filing to completed auction. Uncontested single-property cases typically take 10 to 14 months. Cases with multiple lienholders, borrower bankruptcy filings, or settlement conference complications can extend to 18 months or longer.

Can an investor buy a property before the foreclosure auction in New Mexico?

Yes. The most effective investor strategy in New Mexico is to contact the homeowner during the pre-auction window, which can last 6 to 9 months before the court sets an auction date. A direct purchase before auction lets the homeowner avoid the public auction process and often lets the investor acquire the property at a discount of 15 to 25 percent below market value.

Does New Mexico have a homestead exemption that affects foreclosure investments?

New Mexico's homestead exemption is $60,000 for individuals and $120,000 for married couples filing jointly, protecting equity in a primary residence from general judgment creditors. This does not stop a foreclosure on the mortgage itself, but it means homeowners with substantial equity in their primary residence have less motivation to sell quickly at a discount. Investors should target homeowners whose equity position makes a short sale or discounted purchase the economically rational choice.

What is the mechanics' lien priority rule in New Mexico?

New Mexico mechanics' liens relate back to the date visible construction commenced, not the filing date. A contractor who performed work on a property can file a lien claim that holds priority over mortgages recorded after construction began. For investors acquiring distressed properties, this means running a full mechanics' lien search before closing, particularly on properties with visible recent renovation or construction activity.

Which New Mexico counties have the most foreclosure activity?

Bernalillo County (Albuquerque) generates approximately 45 percent of the state's foreclosure volume. Doña Ana County (Las Cruces) is second. Sandoval County is third and growing fastest as an Albuquerque metro suburb. Rural counties with persistent activity include San Juan County (Farmington) and Rio Arriba County.

Does New Mexico allow deficiency judgments after foreclosure?

Yes. After a foreclosure sale, the lender can seek a deficiency judgment against the borrower for the difference between the auction sale price and the outstanding loan balance. New Mexico follows the fair value statute for deficiency calculations, which means the lender is entitled to seek the difference between the debt and the fair value of the property at the time of sale, not necessarily the auction price. For investors, this is relevant when evaluating whether a property with significant auction discounts will face deficiency claims that complicate clean title transfer.

Are New Mexico foreclosure properties available at auction to any bidder?

Any party can bid at a New Mexico judicial foreclosure sale conducted by a court-appointed special master. The lender can credit bid up to the full judgment amount without paying cash. Third-party bidders must pay in cash or certified funds at the time of sale. The sale must be confirmed by the court before the winning bidder receives title.

The data behind this article

DistressIQ Monitors These Signals in Real Time

Pre-Foreclosures

NOD + NTS filings

Tax Delinquency

County treasurer records

Code Violations

Municipal inspection filings

Probate Filings

Superior Court records

Every lead is scored 0–100 for seller motivation based on signal type, duration, severity, and stacking. Nationwide coverage — every US county, updated daily.

Ready to find deals in your market?

See Live Distress Signals in Your County

Stop calling dead leads. Every lead in DistressIQ is scored 0–100 for seller motivation, with verified contact info included. Browse the free tier to see what's active in your market right now.

Browse Free Leads — No Credit Card