Foreclosure Leads Nevada: The Smart Investor's Guide to the Silver State Market in 2026

Foreclosure Leads Nevada: The Smart Investor's Guide to the Silver State Market in 2026

TL;DR: Nevada uses non-judicial foreclosure almost exclusively under NRS Chapter 107, meaning most foreclosures move to auction without court involvement, which creates both speed and risk for investors. Clark County dominates the market as home to Las Vegas and roughly two-thirds of Nevada's population. The state has no income tax, which attracts investors, but a high median home price and rapid appreciation in desirable areas means competitive bidding at auction. DistressIQ provides verified pre-foreclosure and auction leads across all Nevada counties, updated daily from county records.

Nevada foreclosures move fast. The non-judicial process that governs most Nevada transactions means a property can go from first payment default to auction confirmation in as little as 120 days. That speed separates serious investors from curious browsers. Whoever shows up with the right data, the right capital, and the right exit strategy wins.

The Silver State market has characteristics that don't exist in other Western states. Nevada's population growth is among the highest in the country, driven by migration from California and other high-tax states. That demand means distressed properties that hit the auction block rarely sit idle. But the same factors that drive demand also drive competition. Finding foreclosure leads in Nevada before they reach the courthouse steps is not optional. It is the entire game.

This guide covers what experienced investors need to know about Nevada foreclosure law, the counties that matter, the timelines that govern each stage, and how to access verified distress signals across every Nevada county.

Nevada Foreclosure Law: NRS Chapter 107 and the Non-Judicial Advantage

Nevada is primarily a non-judicial foreclosure state. Under Nevada Revised Statutes Chapter 107, lenders can foreclose without court involvement provided they follow the statutory notice requirements. The process does not require a judge to sign off on the sale, which means timelines are fast and predictable. A lender notices default, publishes a notice of sale in the local newspaper for three consecutive weeks, posts the property, and can confirm the auction within 110 to 140 days of the initial default in most cases.

The critical document for investors is the Notice of Default (NOD). When a borrower misses payments, the lender files an NOD with the county recorder. That filing is a public record and marks the official start of the pre-foreclosure period. The NOD contains the loan amount, the property address, and the name of the beneficiary. It is the first verifiable signal that a property is in distress. Fewer than 5% of Nevada foreclosures involve a court case.

Why Clark County Is the Center of Gravity

Nevada has 17 counties, but the investment opportunity is concentrated in one. Clark County accounts for roughly 2.2 million of Nevada's 3.1 million residents. It encompasses Las Vegas, Henderson, North Las Vegas, Boulder City, Summerlin, Spring Valley, and Paradise. Every serious investor sourcing Nevada foreclosure leads starts here.

The Las Vegas metro has experienced one of the most dramatic boom-bust cycles in American real estate history. Prices doubled from 2002 to 2006, then collapsed by more than 60% from 2008 to 2011. The 2020 pandemic migration from high-cost states drove prices to new nominal highs. That volatility creates distressed opportunities whenever economic conditions shift.

Within Clark County, certain ZIP codes consistently produce more distressed inventory than others. The 89110, 89115, 89106, and 89030 ZIP codes in east Las Vegas and North Las Vegas have historically shown elevated rates of pre-foreclosure and auction activity. These areas have older housing stock, higher concentrations of rental properties, and more investors who may be holding underwater from peak valuations. ZIP codes in the 89144, 89135, and 89138 area (Summerlin) tend to represent higher-value properties where distressed sellers have more equity cushion and less urgency.

Washoe County (Reno) is Nevada's second county by population. The Reno market tracks the California Bay Area economic cycle more than Nevada's own dynamics. Washoe foreclosure leads are worth tracking, but volume is roughly one-seventh of Clark County's.

Nevada Foreclosure Timeline: From Missed Payment to Auction

Understanding Nevada foreclosure law means understanding the timeline. Investors who work backward from the auction date can identify the precise window when a distressed homeowner is most reachable and most likely to negotiate a pre-foreclosure sale that nets both parties a better outcome than the auction.

The stages are: (1) Missed payment and grace period (typically 30 to 90 days before the lender acts, invisible in public records); (2) Notice of Default (NOD) filing with the county recorder, which triggers a 91-day period in Nevada before the lender can schedule a sale; (3) Notice of Sale, published for three consecutive weeks in a newspaper of general circulation; (4) auction, held on the first Tuesday of each month at the county courthouse; and (5) post-foreclosure redemption, which applies in limited circumstances under NRS 107.080 if the homeowner qualifies.

The 91-day window after the NOD is the primary pre-foreclosure outreach period. Distressed homeowners in this window are often motivated but have not accepted that a sale is inevitable. Pre-foreclosure leads in Clark County typically resolve within 90 to 120 days of the NOD filing. Investors who have already done their title search, evaluated comparable sales, and prepared an offer letter are the ones who close before auction.

Free Weekly Alerts

See What's Distressed in Your Market

Get free weekly alerts — new distressed properties, motivation scores, and hot neighborhoods in your area. Addresses and contact info available inside DistressIQ.

Free forever · No credit card · Unsubscribe anytime

Finding Foreclosure Leads in Nevada Before the Auction

The auction is not where smart investors source deals. By the time a property reaches the courthouse steps, it has been priced, analyzed, and bid on by every active investor tracking that county. The real opportunity is in the pre-foreclosure window, before the Notice of Sale is published.

Finding those properties requires accessing county recorder data directly. Every NOD filing is a public record in Nevada, but aggregating that data across Nevada's 17 counties means checking multiple recorder systems, many of which are not fully digitized. Clark County has a functional online search tool, but smaller counties like Elko, Lyon, and Churchill require phone calls or in-person visits.

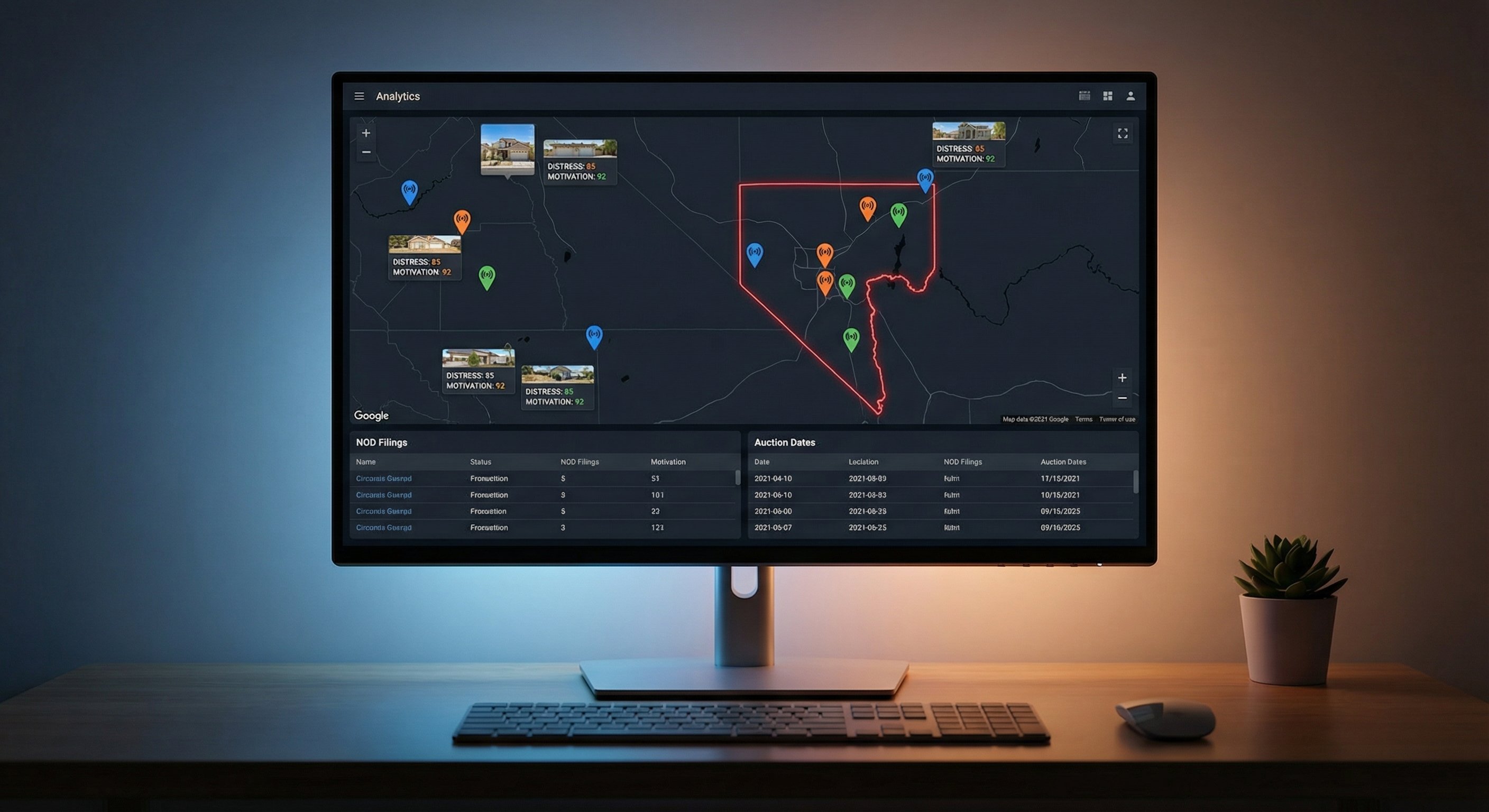

DistressIQ solves this by maintaining verified distress signal data across all Nevada counties. The platform surfaces properties in the pre-foreclosure window and ranks them by urgency using a multi-signal motivation scoring system. The difference between a cold call to a current homeowner and an outreach to a homeowner with a recorded NOD is the difference between a 1% and a 20% response rate.

Nevada Foreclosure Auctions: How to Bid and Win

Investors who want to buy at auction need to prepare before the day of the sale. The auction is not a place to discover the property for the first time.

Due diligence. Title issues become the buyer's problem at auction. Order a preliminary title report at least two weeks before the auction date. Properties at Nevada foreclosure auctions frequently carry junior liens, back taxes, HOA dues, and code violations that survive the foreclosure sale. An investor who wins on a $200,000 property and discovers a $40,000 HOA lien has acquired a costly problem.

The winning bid. Nevada is a non-recourse state for most purchase money loans, which means lenders cannot pursue borrowers for deficiency judgments after a foreclosure sale. This encourages aggressive bidding because investors know their downside is capped. However, investors bidding at auction do not have the same protection. If an investor bids $180,000 and the property is worth $150,000, the investor owns the difference.

Cash requirements. Nevada foreclosure auctions require certified funds. Personal checks are not accepted. Most investors bring a cashier's check for the full bid amount on auction day. Financing contingencies are not permitted. After the auction, properties that do not sell become lender-owned real estate (REO) and typically appear on the MLS within 30 to 90 days.

Key Nevada Counties Beyond Clark

Clark County dominates, but Nevada has other markets worth watching.

Washoe County (Reno / Sparks) is Nevada's second-largest market, closely tied to the California Bay Area economic cycle. Reno's migration-driven growth compressed distressed inventory to historically low levels, but economic corrections still generate leads in the $300,000 to $500,000 range. Washoe County follows the same NRS Chapter 107 process as Clark County.

Elko County is driven entirely by mining. When gold prices fall, Elko foreclosures spike. The pattern is predictable and the county has minimal online recorder access, making pre-auction leads harder to find manually.

Lyon County, south of Washoe, has become a Reno bedroom community. Rising interest rates hit adjustable-rate borrowers hard here, creating new distressed inventory in an area that rarely sees foreclosure activity.

Carson City has a government-employment-anchored economy with low foreclosure volume. Properties that do appear tend to be older homes in established neighborhoods.

How to Evaluate Nevada Distressed Properties

Not every foreclosure lead in Nevada is a good deal. Four factors separate winners from losing trades in this market.

Location. Nevada neighborhoods shift dramatically within a few miles. A distressed property in Summerlin carries a fundamentally different investment thesis than one in North Las Vegas. Evaluate crime rates, school district ratings, proximity to employment centers, and planned infrastructure before committing capital.

Construction quality. Nevada homes built between 2004 and 2008 were often constructed quickly during the population boom. Common issues include stucco failures, foundation settling in areas with poor drainage, air conditioning compressor failures from desert heat stress, and plumbing issues in homes built with polybutylene piping. A $30,000 repair estimate on a property that looks like a $50,000 bargain becomes a losing trade fast.

ARV. Nevada's market recovered past prior peaks in desirable areas. Investors need comparable sales from the past 90 days, not the past year. A comp that is six months old does not reflect a market that moves this quickly.

HOA liens. Nevada has one of the highest rates of HOA-covered properties in the country. Under NRS Chapter 116, HOA liens can prime a first mortgage in certain circumstances. This is a risk that does not exist in most states. Confirm HOA lien status and balance before purchasing any Nevada property in a community with an HOA.

How DistressIQ Surfaces Nevada Foreclosure Leads

DistressIQ tracks foreclosure activity across all Nevada counties, updated daily from county recorder records. For Nevada investors, the platform provides three advantages over manual research. It surfaces pre-foreclosure leads before the Notice of Sale is published, giving investors a window to contact homeowners directly. It scores each lead by motivation level using a multi-signal ranking system, so investors prioritize the most reachable distressed homeowners. And it provides assessor-verified property data including square footage, lot size, year built, and assessed value sourced from county tax records. MLS data is notoriously inaccurate in Nevada, where rapid appreciation has created comparable sales that reflect peak market conditions rather than current values. County assessor data provides the reliable baseline for accurate ARV calculations.

Frequently Asked Questions

How long does foreclosure take in Nevada?

Under NRS Chapter 107, most Nevada foreclosures complete in 110 to 140 days from the initial default filing to the auction. The homeowner has 91 days after the Notice of Default is recorded before the lender can publish the Notice of Sale. After publication (three consecutive weeks in a newspaper), the auction can occur as early as 20 days later.

Is Nevada a non-judicial foreclosure state?

Yes. The vast majority of Nevada foreclosures are non-judicial, processed under NRS Chapter 107 without court involvement. Judicial foreclosures (requiring a court order) represent fewer than 5% of Nevada foreclosure cases.

Can investors buy Nevada foreclosure properties before the auction?

Yes. Investors can approach distressed homeowners during the pre-foreclosure window (after the Notice of Default is recorded but before the auction). A pre-foreclosure sale benefits the homeowner by avoiding an auction with a deficiency judgment risk, and benefits the investor by eliminating auction competition and title risk.

What counties in Nevada have the most foreclosure activity?

Clark County (Las Vegas, Henderson, North Las Vegas) accounts for approximately two-thirds of all Nevada foreclosure activity. Washoe County (Reno / Sparks) is the second most active market. Foreclosure volume in rural Nevada counties is low but does occur around mining and agriculture economic cycles.

Do Nevada foreclosure auctions have a redemption period?

Under NRS 107.080, homeowners who meet indigency requirements can claim a redemption period of up to one year after the auction. However, most non-judicial foreclosures carry no statutory redemption period. Investors should consult a Nevada real estate attorney to confirm redemption rights on any specific property before bidding.

What are the risks of buying Nevada foreclosure property at auction?

The primary risks are title issues (junior liens, HOA liens, back taxes), structural or deferred maintenance issues that are not disclosed before the sale, and overbidding in a competitive auction environment. Nevada's HOA lien law (NRS Chapter 116) can allow HOA liens to prime first mortgages in certain circumstances, which creates risk that does not exist in most other states.

Stop searching through generic property databases that include every Nevada home on the market. DistressIQ shows only verified distress signals across Nevada's 17 counties, updated daily from county recorder sources. Every lead includes a motivation score, assessor-verified property data, and built-in Street View and aerial imagery so investors can evaluate condition before they ever pick up the phone.

See Nevada foreclosure leads at https://distressiq.ai

The data behind this article

DistressIQ Monitors These Signals in Real Time

Pre-Foreclosures

NOD + NTS filings

Tax Delinquency

County treasurer records

Code Violations

Municipal inspection filings

Probate Filings

Superior Court records

Every lead is scored 0–100 for seller motivation based on signal type, duration, severity, and stacking. Nationwide coverage — every US county, updated daily.

Ready to find deals in your market?

See Live Distress Signals in Nevada

Stop calling dead leads. Every lead in DistressIQ is scored 0–100 for seller motivation, with verified contact info included. Browse the free tier to see what's active in your market right now.

Browse Free Leads — No Credit Card