Foreclosure Leads West Virginia: What Smart Investors Need to Know in 2026

Foreclosure Leads West Virginia: What Smart Investors Need to Know in 2026

TL;DR: West Virginia gives investors a cleaner path to ownership than most states. The foreclosure process typically runs 60 days, there is no post-sale redemption period, and lenders cannot pursue deficiency judgments after an auction. That combination means less delay and less legal exposure for buyers who move fast. The counties generating the most activity are Kanawha, Berkeley, Cabell, and Raleigh.

Why West Virginia Is Worth Watching in 2026

Foreclosure activity in West Virginia jumped 97.5% year over year as of February 2025, according to ATTOM data. That is not a small move. It reflects a broader shift in the national housing landscape, and it is putting the Mountain State on more investors' radar.

Most articles about foreclosure leads treat the process as essentially the same from state to state. They are not. West Virginia has legal features that materially change how an investor approaches a deal, particularly around what happens after the auction gavel falls.

If you are looking for foreclosure leads in West Virginia, three facts will shape every decision you make: the state has no post-sale redemption period, lenders cannot pursue deficiency judgments, and the notice and publication requirements create a narrow but exploitable window between the first public notice and the actual auction date.

This article covers all three, along with the counties producing the most deal flow and the specific data points that separate informed investors from latecomers to this market.

How Foreclosure Works in West Virginia

West Virginia permits both judicial and non-judicial foreclosure, but the non-judicial path is faster and far more common when the mortgage or deed of trust contains a power of sale clause. Most investment-focused foreclosure leads in the state trace back to non-judicial trustee sales.

Here is how the process moves:

Missed payments trigger default notice. After three consecutive missed mortgage payments, the lender refers the case to a foreclosure trustee. The trustee sends the borrower a notice of default. The borrower then has 10 days to cure the arrearage before the process advances.

Publication and notice requirements begin. Once the lender has decided to proceed with a sale, West Virginia law requires the notice of sale to be published as a Class III legal advertisement once a week for four consecutive weeks in the county where the property is located. That is a minimum of four publication dates. The notice must also be posted at the county courthouse and on the property itself at least 20 days before the auction.

The auction happens at the courthouse door. Foreclosure sales in West Virginia are public auctions. Unless the deed specifies different terms, the winning bidder must pay one-third of the bid amount immediately at the sale, with the balance due at closing.

Total timeline: typically 60 days from the first missed payment to the sale date, assuming no borrower contests or pursues loss mitigation.

The Two Legal Features That Make WV Different

This is where West Virginia separates itself from states like New York, New Jersey, and Florida, where redemption periods and deficiency exposure create post-closing risk.

No Redemption Period

Many states give borrowers a statutory window to reclaim their property after a foreclosure auction, sometimes 30 days, sometimes a full year. West Virginia does not. Once the auction is complete and the sale is confirmed, ownership transfers immediately. There is no statutory redemption period that can undo the transaction.

For investors, this means certainty of acquisition. You do not close and wait to see if the previous owner finds financing to buy back the property. The deal you strike at the auction is the deal you keep.

No Deficiency Judgments

In most states, if a foreclosing lender sells the property at auction for less than the outstanding mortgage balance, the lender can pursue the borrower personally for the difference. That is a deficiency judgment. It creates ongoing liability that can follow a borrower for years.

West Virginia prohibits deficiency judgments following non-judicial foreclosure sales. The auction price, whatever it is, settles the debt. This also means buyers at auction do not need to worry about the previous owner's financial exposure clouding title.

For investors, these two features together create a cleaner exit. You acquire, you own, and there are no surprise legal liabilities waiting behind you.

Free Weekly Alerts

See What's Distressed in Your Market

Get free weekly alerts — new distressed properties, motivation scores, and hot neighborhoods in your area. Addresses and contact info available inside DistressIQ.

Free forever · No credit card · Unsubscribe anytime

The 20-Day Notice Window: Your Competitive Edge

While the four-week publication requirement gets most of the attention, the notice provisions in West Virginia contain a detail that sophisticated investors use strategically.

The lender must serve written notice of the sale on the borrower and all junior lien holders at least 20 days before the auction date. This notice is part of the legal record. It is also a public document.

Investors who monitor county courthouse filings and trustee sale calendars in high-activity counties can identify properties entering the pipeline before the publication cycle completes. The notice of sale often surfaces in public records 30 to 45 days before the auction date, which gives an investor a meaningful head start compared to waiting for the county website to update or relying solely on third-party listing aggregators.

This is not a glitch in the system. It is how the process is designed. But most retail buyers and even many active investors do not monitor public notice records systematically. That is the gap.

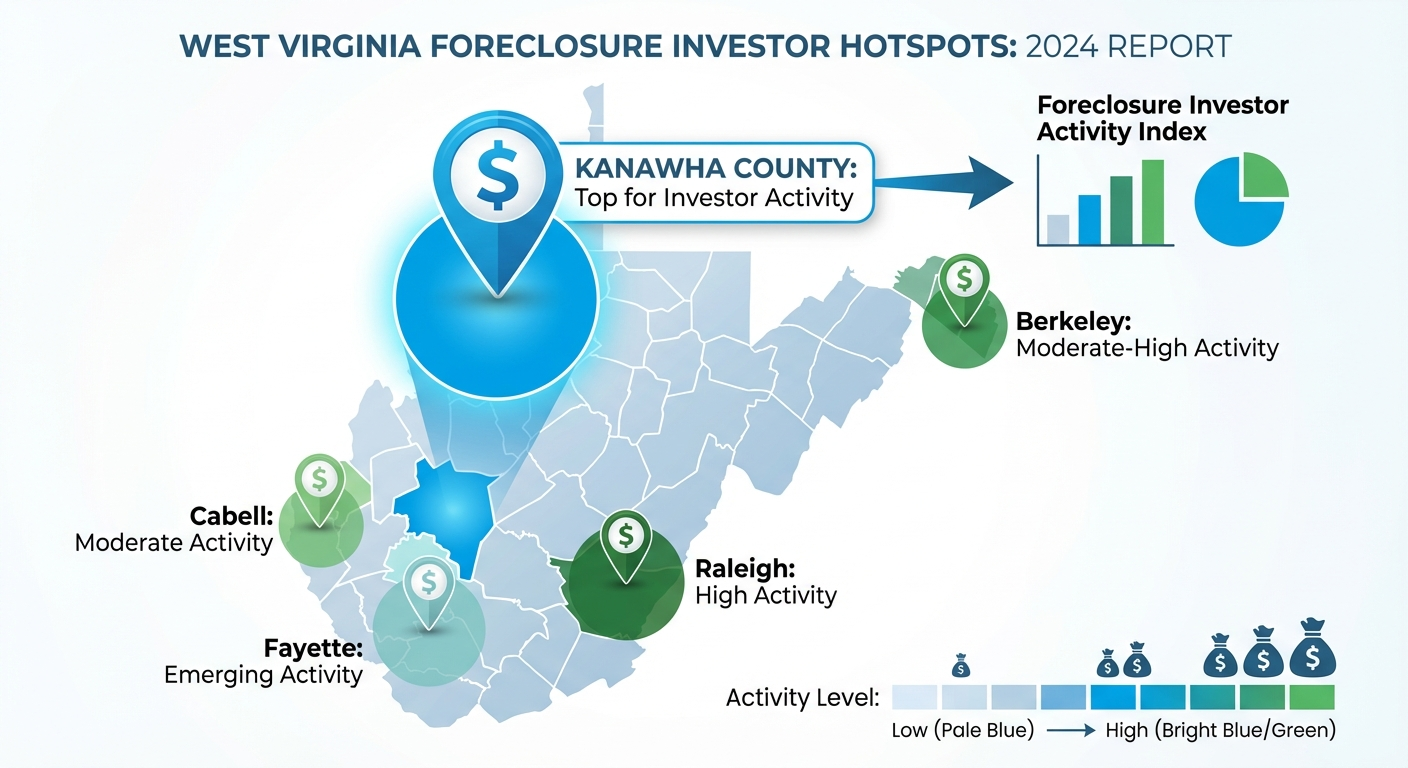

Counties Generating the Most Foreclosure Leads

Not all West Virginia counties are equal when it comes to deal volume. The investor activity data from Q4 2025 shows clear geographic concentration.

Kanawha County leads the state with 13,240 investor-owned single-family residential properties and a 22.7% investor ownership rate. It is the capital county and the largest metro area in West Virginia. If you are targeting the highest raw volume of leads, this is where to start.

Raleigh County stands out as the second-highest volume county with 9,186 investor-owned properties and a 35.1% investor ownership rate. That combination of volume and concentration makes it one of the most efficient counties to target for deal flow.

Berkeley County ranks fourth in total investor property count with 5,942 properties, but its ownership rate of 14.1% reflects a larger and more active overall housing market. Its proximity to the Washington-Baltimore metro area drives demand, and foreclosure leads here frequently trade at a smaller discount than in more rural counties.

Cabell County (Huntington metro) and Fayette County round out the top five counties by investor property volume.

For investors building a geographic strategy, Kanawha and Raleigh offer the highest density of investor-relevant inventory. Berkeley County offers a different profile: larger price points, metro-adjacent demand, and potentially faster resale or rental turnaround.

What DistressIQ Provides for West Virginia Investors

The research above tells you what the process looks like. The actual work is finding properties before they hit the auction calendar, with owner contact information and motivation signals attached.

DistressIQ aggregates pre-foreclosure filings, auction notices, and REO listings across West Virginia counties and delivers them with motivation scoring so you can prioritize the leads most likely to convert. Rather than monitoring five different county recorder websites and courthouse bulletin boards, you get a unified view of the West Virginia foreclosure market updated daily.

You can filter by county, by estimated equity gap, by owner occupancy status, and by time-on-market signals. The platform covers the counties listed above and the dozens of smaller counties with lower foreclosure volume but sometimes deeper discounts.

If you are actively working leads in West Virginia, the difference between a two-week deal cycle and a two-month cycle often comes down to how early you identify the property and how much you know about the seller's situation before you make contact.

See West Virginia foreclosure leads scored by motivation -- browse free on DistressIQ. Get Started

How West Virginia Compares to Neighboring States

Investors working across the Appalachia corridor often evaluate West Virginia alongside Ohio, Pennsylvania, Virginia, and Kentucky. The comparison is favorable on two key dimensions.

West Virginia's non-judicial foreclosure timeline of roughly 60 days is faster than Pennsylvania's judicial process, which can stretch six months or longer. It is comparable to Virginia's non-judicial timeline but without Virginia's statutory redemption period. Against Kentucky, which allows redemption periods that can run 12 months, West Virginia's no-redemption rule is a significant structural advantage.

Ohio presents a more mixed picture. Its judicial foreclosure process can be lengthy, but the state has a more active distressed property market with higher volume. Investors who want speed and legal simplicity choose West Virginia. Investors who want volume and deal flow choose Ohio. The two states complement each other in a regional portfolio.

Frequently Asked Questions

How long does foreclosure take in West Virginia?

Non-judicial foreclosure in West Virginia typically completes in 60 days from the initial default notice to the auction date, assuming the borrower does not contest the case or pursue loss mitigation. Judicial foreclosures take longer, sometimes several months, depending on court calendars.

Does West Virginia have a redemption period after foreclosure?

No. West Virginia does not have a statutory redemption period following a non-judicial foreclosure sale. Once the auction is complete, ownership transfers immediately and the previous owner has no legal right to reclaim the property by paying the auction price.

Can a lender pursue a deficiency judgment in West Virginia?

No. West Virginia prohibits deficiency judgments following non-judicial foreclosure sales. The winning bid at auction settles the debt between the lender and the borrower, and the lender cannot pursue the borrower personally for any shortfall.

Which West Virginia counties have the most foreclosure activity?

Kanawha County leads the state in total foreclosure volume, followed by Berkeley, Cabell, Raleigh, and Fayette counties. These five counties account for over 31% of all investor-owned single-family residential properties in West Virginia.

Can investors buy properties before they go to auction in West Virginia?

Yes. Pre-foreclosure leads in West Virginia represent properties where the owner has received a notice of default but the auction has not yet occurred. Investors who identify these properties early can contact the owner directly and negotiate a pre-foreclosure sale, potentially avoiding the auction process entirely and acquiring the property with more flexibility on closing terms.

What does a buyer need to pay at a West Virginia foreclosure auction?

Unless the deed specifies different terms, the winning bidder at a West Virginia foreclosure auction must pay one-third of the bid amount immediately at the sale, with the remaining balance due at closing. Bidders should have financing arranged or have verified funds available before attending an auction.

Are REO properties common in West Virginia?

REO (bank-owned) volume in West Virginia is relatively low compared to larger states. As of early 2025, ATTOM data showed fewer than 100 REO properties statewide. Most of the deal flow for investors comes from pre-foreclosure and auction-stage properties rather than bank-owned inventory.

Also published on DistressIQ Blog: Foreclosure Leads West Virginia

The data behind this article

DistressIQ Monitors These Signals in Real Time

Pre-Foreclosures

NOD + NTS filings

Tax Delinquency

County treasurer records

Code Violations

Municipal inspection filings

Probate Filings

Superior Court records

Every lead is scored 0–100 for seller motivation based on signal type, duration, severity, and stacking. Nationwide coverage — every US county, updated daily.

Ready to find deals in your market?

See Live Distress Signals in West Virginia

Stop calling dead leads. Every lead in DistressIQ is scored 0–100 for seller motivation, with verified contact info included. Browse the free tier to see what's active in your market right now.

Browse Free Leads — No Credit Card