Foreclosure Leads Kansas: The Shortest Path to Distressed Property Deals in the Sunflower State

TL;DR: Kansas uses judicial foreclosure exclusively, meaning every foreclosure goes through the court system. The standard redemption period is 3 months for most homeowners (12 months if more than one-third of the principal has been paid), making Kansas one of the fastest pipelines from pre-foreclosure to sheriff sale in the country. The foreclosure process takes approximately 120 days from default to sale. Most distressed inventory concentrates in three counties: Johnson County (Kansas City suburbs), Sedgwick County (Wichita), and Wyandotte County (Kansas City, KS). The median home price is $281,000 statewide, but submarket prices vary widely: Johnson County homes average $460,000 while Wichita-area distressed properties frequently trade under $100,000. For investors who understand Kansas's court-driven process and know where to look, the Sunflower State offers less competition per deal than bigger markets.

Most real estate investors skip Kansas. The distressed inventory numbers look small compared to Texas or Florida, so they write the state off and pile into markets where the raw lead counts are bigger.

That is exactly the mistake.

Kansas has a judicial-only foreclosure process that creates a uniquely compressed timeline from default to sheriff sale. The redemption period runs as short as 3 months for most homeowners, which is the shortest standard window in the country. And the market splits into two distinct investment tiers: a high-price Johnson County suburb market where median prices approach $460,000, and a Wichita/Sedgwick County market where distressed properties trade below $100,000 regularly.

Less competition. Faster pipeline. Two different price points that support different exit strategies.

If you are working Kansas leads, here is what you need to know.

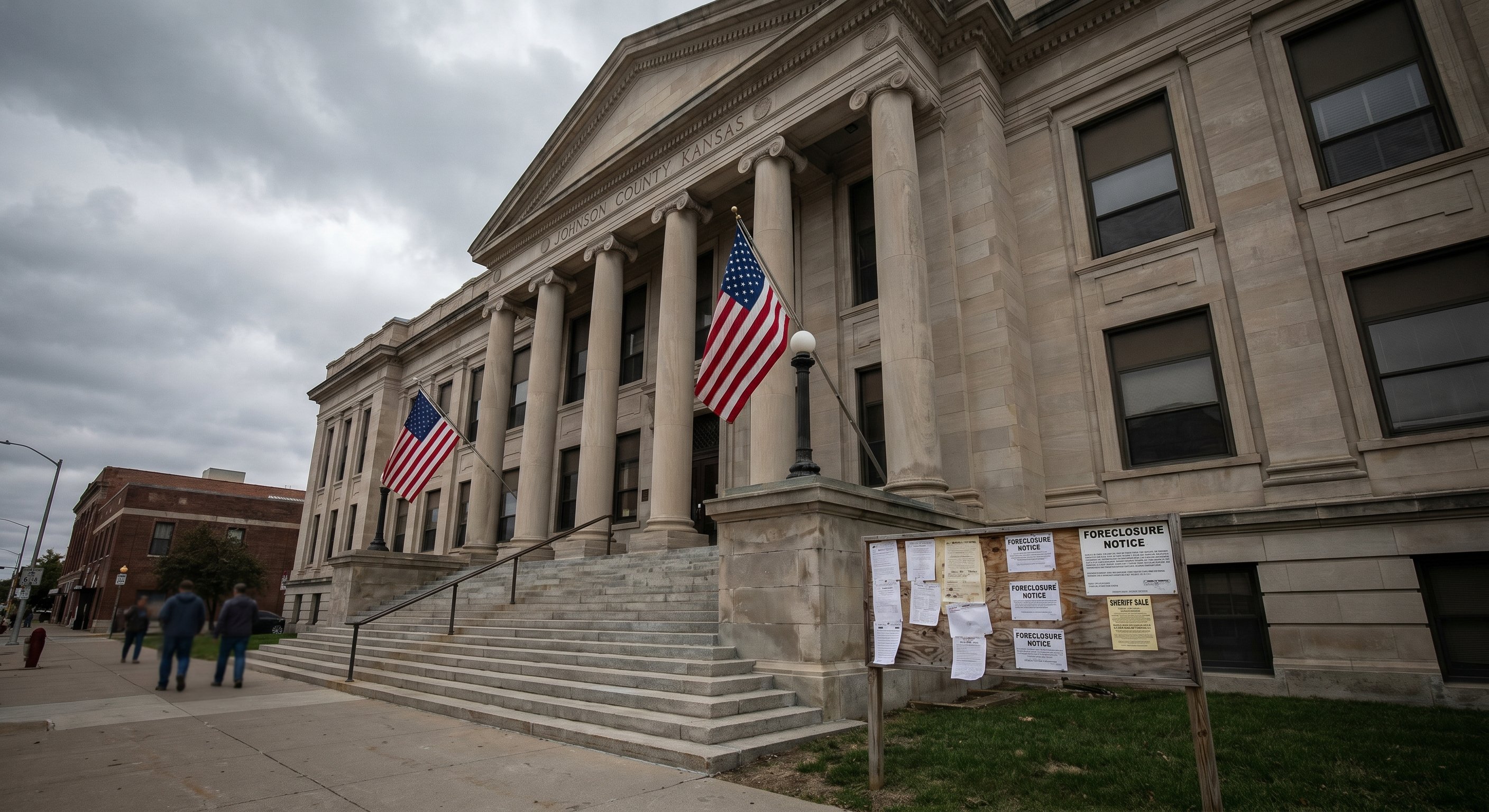

How Foreclosure Works in Kansas

Kansas is one of 15 states that uses judicial foreclosure exclusively. The lender cannot proceed outside of court. They must file a foreclosure lawsuit and get a court order before the property can be sold at auction.

This is a meaningful constraint. It adds legal steps, filing requirements, and court timelines that do not exist in the 35 states that allow non-judicial foreclosure. But it also means the process is more structured and more transparent, with court records that make lead identification more reliable.

Here is the Kansas foreclosure sequence:

Default: Typically after 120 days of missed payments. Federal servicing guidelines generally require 120 days delinquency before a servicer can initiate foreclosure.

Pre-foreclosure window: After default, before the lender files suit. This is your outreach window. The homeowner is actively dealing with financial distress and is most reachable.

Court filing: The lender files a foreclosure petition with the district court in the county where the property sits. The petition must be served on the borrower, who has 21 days to respond.

Judgment: If the borrower does not respond or has no valid defense, the court enters a judgment of foreclosure. This establishes the amount owed and orders the property sold at sheriff sale.

Sheriff sale: The property is auctioned at the county sheriff's office. Sales are typically held at the county courthouse. Winning bidders receive a certificate of purchase.

Redemption period: After the sale, the borrower has a statutory right to redeem the property by paying the full judgment amount plus costs. Most Kansas homeowners have a 3-month redemption period. If the borrower has paid more than one-third of the original principal balance, the redemption period extends to 12 months.

The entire process runs approximately 120 days from default to sale, though the redemption period adds time after the sale before the sheriff's deed is issued and title clears.

The 3-Month Redemption Period: Kansas's Best-Kept Investor Advantage

This is the detail most investors miss, and it is the strongest argument for working Kansas.

Most Kansas homeowners have a 3-month redemption period after the sheriff sale. That is the shortest standard redemption window of any state in the country. Compare that to New York, where redemption periods can run 12 months or more, or to Vermont, where 180-day periods are standard.

The practical impact is significant. A 3-month redemption period means:

- The homeowner has less time to arrange alternate financing or find a buyer

- The post-sale urgency is genuinely higher than in states with longer windows

- Your post-sale outreach to the previous owner is more likely to catch them still in transition

- The lender clears title and can convey the property faster, reducing your closing timeline compared to states with extended redemption periods

The 12-month extension applies only when the borrower has paid down more than one-third of the original principal. That is a meaningful equity condition that most distressed homeowners do not meet, which means the 3-month window is the common case.

For investors who understand this, Kansas is not a slow judicial state like New York or Illinois. It is a fast judicial state with a short redemption tail. The deal pipeline moves.

Kansas Foreclosure Laws: What Investors Need to Know

Title search requirement: Kansas requires a title search before a lender can file foreclosure. This is not universal across judicial states. The title search identifies any liens senior to the lender's lien, and all junior lienholders must be named as defendants in the foreclosure suit. For investors, this means the title on a Kansas foreclosure property should be cleaner at sale than in states where junior liens can survive the auction unnoticed.

Deficiency judgments: Kansas allows deficiency judgments. After the sheriff sale, the lender can sue the borrower for the difference between the sale price and the outstanding loan balance. This affects homeowner motivation. Kansas homeowners facing deficiency judgments have additional financial pressure that can drive them to negotiate a short sale or deed-in-lieu before the sale, which creates pre-foreclosure deal opportunities.

Notice requirements: The notice of sale must be published once a week for three consecutive weeks in a local newspaper. The final publication must be at least 7 days and no more than 14 days before the sale date. The borrower must also receive written notice of the first publication within 5 days.

Sheriff sale location: Sales are typically held at the county sheriff's office in the county where the property is located. Bidders need to appear in person or arrange for a third party to bid on their behalf.

Free Weekly Alerts

See What's Distressed in Your Market

Get free weekly alerts — new distressed properties, motivation scores, and hot neighborhoods in your area. Addresses and contact info available inside DistressIQ.

Free forever · No credit card · Unsubscribe anytime

Where the Deals Are: Kansas's Three Investment Markets

Kansas distressed inventory is not evenly distributed. Three counties hold the vast majority of the state's pre-foreclosure and sheriff sale activity.

Johnson County, Kansas City Suburbs

Johnson County is the dominant Kansas investment market. As the wealthiest and fastest-growing county in the state, it holds the most distressed inventory by volume and the highest price points. Median home prices hit $460,000 in early 2026, up 4.5% year-over-year. Homes sell in 46 days on average.

Despite the strong underlying market, Johnson County had 41 pre-foreclosures at last count with 2,549 total involuntary liens across the county. That is a thin inventory number, but it reflects how quickly the market absorbs distressed properties when they hit. The demand pool is deep.

For flippers, Johnson County is ARV territory. A distressed ranch home purchased at sheriff sale and renovated commands $400,000-plus in most submarkets. The repair budgets need to support that exit, which means $30,000 to $60,000 in rehab is realistic for the right property.

For wholesalers, the Johnson County buyer pool is active and well-capitalized. Distressed properties that are clean and priced right move.

Overland Park, Olathe, and Leawood are the primary submarkets within Johnson County. Overland Park alone saw 542 homes close in February 2026, up 10.4% year-over-year.

Sedgwick County, Wichita

Sedgwick County and the Wichita metro represent Kansas's affordable end of the distressed property spectrum. This is where Kansas whispers to investors who are paying attention.

Median home prices in Wichita are substantially lower than Johnson County. Distressed properties in Sedgwick County regularly trade below $100,000 at sheriff sale. Local investors and wholesalers have been quietly working this market for years, but national attention is thin compared to bigger metros.

The Wichita investment community is active and sophisticated. Local wholesalers like KS Wholesale Properties and Kansas Home Guys have built businesses around distressed Wichita properties. These are not amateur operators; they have been working the market through multiple cycles.

For out-of-state investors, Wichita's distressed inventory is accessible via county-direct data. The property profiles are available, the sheriff sale process is public, and the local investor community is willing to do deals with outside capital.

Wyandotte County, Kansas City, KS

Wyandotte County is the Kansas half of the Kansas City metro. It is more affordable than Johnson County and has a distinct buyer pool: working-class buyers, Section 8 rental investors, and flippers who target the $150,000 to $250,000 range.

Wyandotte County had significant pre-foreclosure activity and is historically one of the more active Kansas counties for distressed property filings. The median home price is substantially lower than Johnson County, which supports both fix-and-flip and buy-and-hold strategies.

For investors willing to work the lower price point, Wyandotte County can offer more deal volume per county than the Johnson County market.

Kansas Market Fundamentals: Why the Math Works

Kansas ranked #20 among the hottest real estate markets in the country in 2026, according to Construction Coverage's state-level analysis. The composite score of 58.0 reflects a market that is growing faster than national averages in some dimensions.

Key numbers from Construction Coverage's 2026 state housing report:

- Median sale price (January 2026): $281,000, up 6.9% year-over-year versus 1.6% nationally

- Average days on market: 29 days, well below the national average of 48.7

- Sale-to-list ratio: 98.0%, meaning most homes sell at or near asking

- Homes sold above asking: 15.3%

The 29-day average marketing period is a meaningful signal for investors. Kansas does not have the extended market times that plague some Midwest markets. Distressed properties that are priced correctly move. That supports the flip timeline and reduces carrying cost exposure.

Johnson County specifically outpaces the state average. Per eMetropolitan's February 2026 Johnson County housing report, the Kansas City suburbs averaged $574,777 in February 2026 with a median of $460,000, up 10.9% year-over-year. Average sales prices have climbed from under $300,000 in 2016. That decade of compounding appreciation creates equity in the existing housing stock that translates directly into ARV potential for rehab investors.

The Wichita market follows a different but equally compelling pattern. Lower entry prices mean distressed Wichita properties can be acquired at sheriff sale for $40,000 to $80,000, renovated for $20,000 to $35,000, and sold or rented at $180,000 to $220,000. The spread works at lower price points than investors typically need in major metros.

The Title Search Requirement: An Underappreciated Kansas Advantage

Here is a detail that almost never appears in articles about Kansas foreclosure investing, but matters enormously for deal quality.

Kansas law requires a title search before a lender can file foreclosure. This is not a universal requirement in judicial foreclosure states. The title search identifies all liens senior to the lender's mortgage and requires that junior lienholders be named as defendants in the foreclosure suit.

The practical result: Kansas foreclosure properties that reach sheriff sale have a higher probability of clean title than foreclosure properties in states where title defects can survive the sale unnoticed. The junior lien issue has been addressed through the litigation process before the auction, per Kansas Legal Services foreclosure guidance.

For investors who buy at sheriff sale and want to flip or rent without extensive post-closing title issues, this is a structural advantage. It does not eliminate title risk entirely, but it reduces one of the most common post-foreclosure complications that investors encounter in states like Illinois or New York.

This also means that pre-foreclosure outreach in Kansas has an additional strategic value. A homeowner who agrees to a short sale or deed-in-lieu before the foreclosure suit is filed avoids the full legal process and the public record of a sheriff sale. Some Kansas homeowners in pre-foreclosure are highly motivated to find this exit because it avoids the court process entirely.

How to Find Foreclosure Leads in Kansas

Kansas does not maintain a centralized statewide foreclosure listing. The auction docket lives at each county sheriff's office, and court filings are public records available through the Kansas district court system.

The practical sourcing options for investors:

County courthouse research: Each of Kansas's 105 counties maintains foreclosure filings through its district court. The sheriff's office in each county publishes the auction docket. For investors working one or two counties, this is feasible. For investors covering the state, it requires significant time allocation.

Published notices: Kansas requires three consecutive weekly publications of the sheriff sale notice in a local newspaper. These notices are public record and can be tracked, but they are not aggregated into a consumer-facing database.

Third-party platforms: Most national lead platforms cover Kansas, but coverage depth varies. Platforms pulling county-direct data will have the most current pre-foreclosure listings before they reach the auction stage.

DistressIQ covers Kansas across all 105 counties with distress signals sourced from county records. Investors can browse Kansas properties by county, filter by signal type, and see motivation scores that rank leads by urgency before doing any outreach.

Browse foreclosure leads in Kansas on DistressIQ, filtered by county, signal type, and motivation score.

Kansas vs. Neighboring States: Why Kansas Wins for Serious Investors

Kansas sits in a region where neighboring states offer different foreclosure dynamics. Understanding how Kansas compares helps investors decide where to allocate their sourcing effort.

Kansas vs. Missouri: Missouri uses non-judicial foreclosure for most mortgages, which means faster foreclosure timelines but fewer court records as a sourcing resource. Missouri's redemption period is also longer. Kansas's court-driven process creates better public records for lead identification, even if the raw timeline is similar.

Kansas vs. Oklahoma: Oklahoma is non-judicial for most mortgages. Oklahoma City and Tulsa are larger metros with more distressed volume than any single Kansas market. But Kansas offers less competition per lead in the suburban Johnson County market, which is a meaningful differentiator.

Kansas vs. Colorado: Colorado's market is substantially more expensive, with median prices well above $400,000 in the Denver metro. Colorado investors are working a higher-price-point game. Kansas offers lower entry costs and comparable judicial structure.

Kansas vs. Nebraska: Nebraska is also judicial-only and has a 3-month redemption period similar to Kansas. But Nebraska's distressed inventory volume is even smaller than Kansas's, making it harder to build a volume sourcing business.

The strongest case for Kansas over neighboring states is the combination of judicial process, 3-month redemption window, and the Johnson County/Wichita dual-market structure. You get a premium suburban market and an affordable entry market within the same state.

Kansas Real Estate Market Trends Every Investor Should Track

Beyond the foreclosure basics, Kansas's broader market dynamics affect deal math and exit strategy.

Johnson County appreciation has been extraordinary. Average sales prices have climbed from under $300,000 in 2016 to over $574,000 in early 2026. That is roughly 10% annual appreciation over a decade. The implied ARV for renovated properties has moved correspondingly, which means flippers working Johnson County have a strong underlying market supporting their exit.

Wichita's rental market is stable. The Wichita metro has a well-established rental demand driven by military families (McConnell Air Force Base), healthcare workers (Via Christi and Wesley healthcare systems), and students (Wichita State University). Cap rates for turnkey Wichita rentals run 7 to 10% in established neighborhoods, which is competitive with national averages.

Kansas property taxes are a factor in deal math. Kansas property taxes are moderate compared to Texas but higher than some neighboring states. The effective tax rate varies significantly by county, with Johnson County rates running higher than rural Kansas counties. Factor ongoing property tax burden into holding cost calculations.

Inventory remains tight. Kansas has approximately 1.8 to 2 months of housing supply in most metros, which is firmly in seller market territory. Low inventory means distressed properties that hit the market face genuine competing demand from regular buyers. This supports your exit whether you are selling to an end buyer or wholesaling to another investor.

Finding Verified Foreclosure Leads in Kansas

The challenge with Kansas is not the data itself. The challenge is accessing it efficiently across 105 counties with varying digital record availability.

County court records are public in Kansas, but accessing them requires either physical courthouse visits or navigating county-specific online record systems that are not standardized. Most investors working Kansas either specialize in one or two counties or use a platform that aggregates county-direct data across the full state.

DistressIQ tracks pre-foreclosures, code violations, lis pendens filings, and other distress signals across every Kansas county, updated daily from county records. The motivation scoring ranks Kansas leads by urgency so you can focus outreach on the properties where homeowners are most likely to engage.

Browse Kansas foreclosure leads on DistressIQ.

Frequently Asked Questions

How long does foreclosure take in Kansas?

The judicial foreclosure process in Kansas runs approximately 120 days from default to sheriff sale. After the sale, the standard redemption period is 3 months for most homeowners. If the borrower has paid more than one-third of the original principal balance, the redemption period extends to 12 months. The total timeline from default to title clearance is typically 6 to 9 months.

Does Kansas allow deficiency judgments after foreclosure?

Yes. Kansas allows lenders to pursue deficiency judgments for the difference between the foreclosure sale price and the outstanding loan balance. This affects homeowner motivation and creates pre-foreclosure deal opportunities as homeowners look to avoid both the public sale and potential deficiency liability.

What is the redemption period in Kansas?

Most Kansas homeowners have a 3-month redemption period after the sheriff sale. This is the shortest standard redemption window in the country. If the borrower has paid more than one-third of the original principal balance, the redemption period extends to 12 months. The court sets the specific redemption period based on the borrower's payment history.

Which Kansas counties have the most foreclosure activity?

Johnson County (Kansas City suburbs) holds the most distressed inventory by volume and price point, with median home prices approaching $460,000. Sedgwick County (Wichita) is the most active affordable market, with distressed properties regularly trading below $100,000 at sheriff sale. Wyandotte County (Kansas City, KS) rounds out the active markets with a mix of fix-and-flip and rental investment opportunities.

Can you buy Kansas foreclosure properties with a conventional loan?

Most sheriff sales require cash or certified funds at the auction. After the redemption period passes and title is cleared, conventional financing can be used for post-foreclosure purchases. Many investors use hard money or private money for the sheriff sale acquisition and refinance to conventional after closing.

What makes Kansas different from neighboring states for foreclosure investing?

Kansas is judicial-only (every foreclosure goes through court), has the shortest standard redemption period in the country at 3 months, and requires a title search before foreclosure can be filed. This combination creates a faster pipeline, better public records for lead sourcing, and cleaner titles at auction than many neighboring states.

The data behind this article

DistressIQ Monitors These Signals in Real Time

Pre-Foreclosures

NOD + NTS filings

Tax Delinquency

County treasurer records

Code Violations

Municipal inspection filings

Probate Filings

Superior Court records

Every lead is scored 0–100 for seller motivation based on signal type, duration, severity, and stacking. Nationwide coverage — every US county, updated daily.

Ready to find deals in your market?

See Live Distress Signals in Your County

Stop calling dead leads. Every lead in DistressIQ is scored 0–100 for seller motivation, with verified contact info included. Browse the free tier to see what's active in your market right now.

Browse Free Leads — No Credit Card