How to Find Foreclosure Leads in Illinois (2026 Investor Guide)

How to Find Foreclosure Leads in Illinois (2026 Investor Guide)

Illinois requires lenders to mail a formal notice of foreclosure to borrowers before filing any court action. That document, mandated under the Illinois Mortgage Foreclosure Law (735 ILCS 5/Art. XV), triggers a judicial process spanning 12 to 24 months from filing to sheriff's sale. For investors targeting foreclosure leads in Illinois, that extended timeline creates a wide window for outreach and deal assembly before properties reach auction.

Why Illinois Is Different

Illinois is a strict judicial foreclosure state. Every foreclosure must pass through circuit court. The governing statute, the Illinois Mortgage Foreclosure Law (735 ILCS 5/Art. XV), sets procedural requirements that slow the process and create multiple touchpoints where investors can identify distressed properties.

The timeline is the defining feature. From filing to completed sheriff's sale, the process typically runs 12 to 24 months, among the longest in the country. A property entering foreclosure in January 2026 may not reach auction until mid 2027.

Illinois also grants homeowners strong protections. After judgment, borrowers retain a right of reinstatement for up to 90 days. Once that expires, the redemption period begins: either 7 months from service of summons or 3 months from judgment, whichever is later. These protections delay the process but create extended periods where owners may be receptive to a sale.

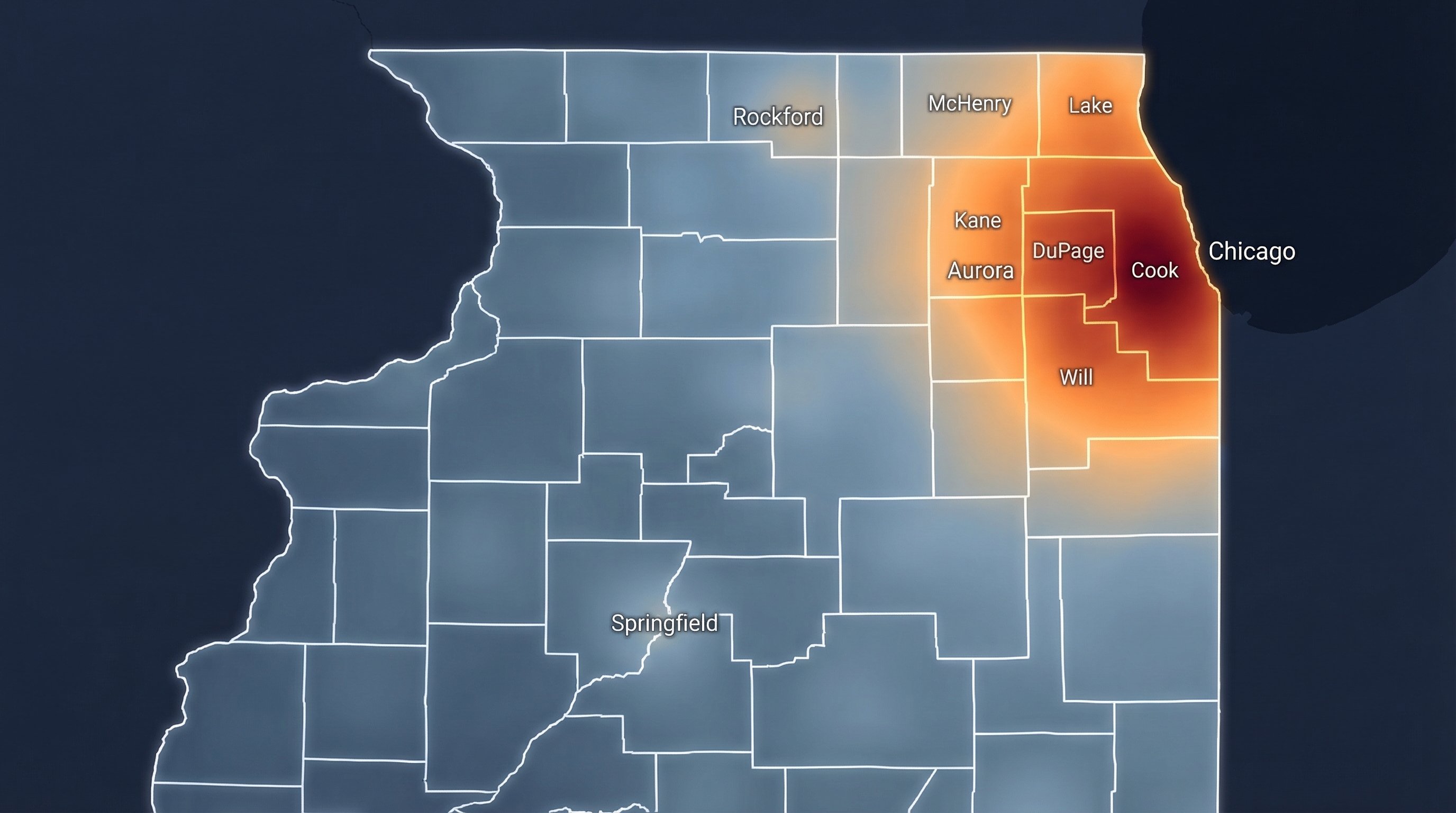

County-Level Foreclosure Activity

Cook County (Chicago). Cook County accounts for roughly 40% of all Illinois foreclosure filings. Within Chicago, Austin, Englewood, and South Shore consistently rank among the highest-activity neighborhoods. South suburbs like Dolton, Harvey, and Markham also produce steady inventory. Investors should monitor the Chancery Division of the Circuit Court of Cook County, where all foreclosure complaints are filed.

DuPage County. West of Chicago, DuPage sees moderate but consistent volume in towns like Aurora, Naperville, and Addison. Properties here carry higher valuations than south Cook County, making them attractive for fix-and-flip investors seeking wider margins.

Lake County. Filings cluster around Waukegan, North Chicago, and Zion. The circuit court in Waukegan processes all cases, and timelines track close to the state average.

Will County. Communities along the I-55 corridor, including Joliet, Bolingbrook, and Romeoville, have seen elevated activity as property taxes and insurance costs outpace income growth in some areas.

Kane County. Filings center on Elgin, Aurora (the western portion), and Carpentersville. Lower entry prices than DuPage make these markets popular with wholesale investors.

The Timeline and Where Leads Surface

Pre-filing: The Grace Notice. Illinois requires lenders to mail a notice of foreclosure at least 30 days before filing a complaint. This is the earliest signal. Properties at this stage are not yet in public court records, so identifying them requires specialized data sources: lis pendens monitors, lender activity databases, and lead aggregation services that track pre-filing signals.

Filing to Judgment. Once the lender files in circuit court, the case enters public record with a lis pendens recorded against the property. The period between filing and judgment typically spans 6 to 12 months. Homeowners in this window are often motivated to sell and avoid the credit damage of a completed foreclosure.

Judgment to Sale. After judgment, the redemption clock runs. Once it expires, the property goes to sheriff's sale. Owners at this stage have exhausted most legal options and may negotiate quickly. The auction price typically hovers near the outstanding mortgage balance rather than market value.

Free Weekly Alerts

See What's Distressed in Your Market

Get free weekly alerts — new distressed properties, motivation scores, and hot neighborhoods in your area. Addresses and contact info available inside DistressIQ.

Free forever · No credit card · Unsubscribe anytime

Data Sources for Illinois Foreclosure Leads

Circuit Court Records. Every Illinois foreclosure flows through circuit court. Most counties offer online case search portals. Cook County's system allows searches by party name, case number, or date. DuPage, Lake, Will, and Kane maintain similar portals, though bulk data extraction is rarely supported.

County Recorder Offices. Lis pendens filings are public record, searchable by date range, property address, or grantor/grantee name. Per-document access fees add up for investors pulling high volumes.

Sheriff's Sale Listings. Properties at the sale stage appear on the county sheriff's auction schedule. Cook County publishes its list roughly 30 days before auction, including the address, judgment amount, and minimum bid.

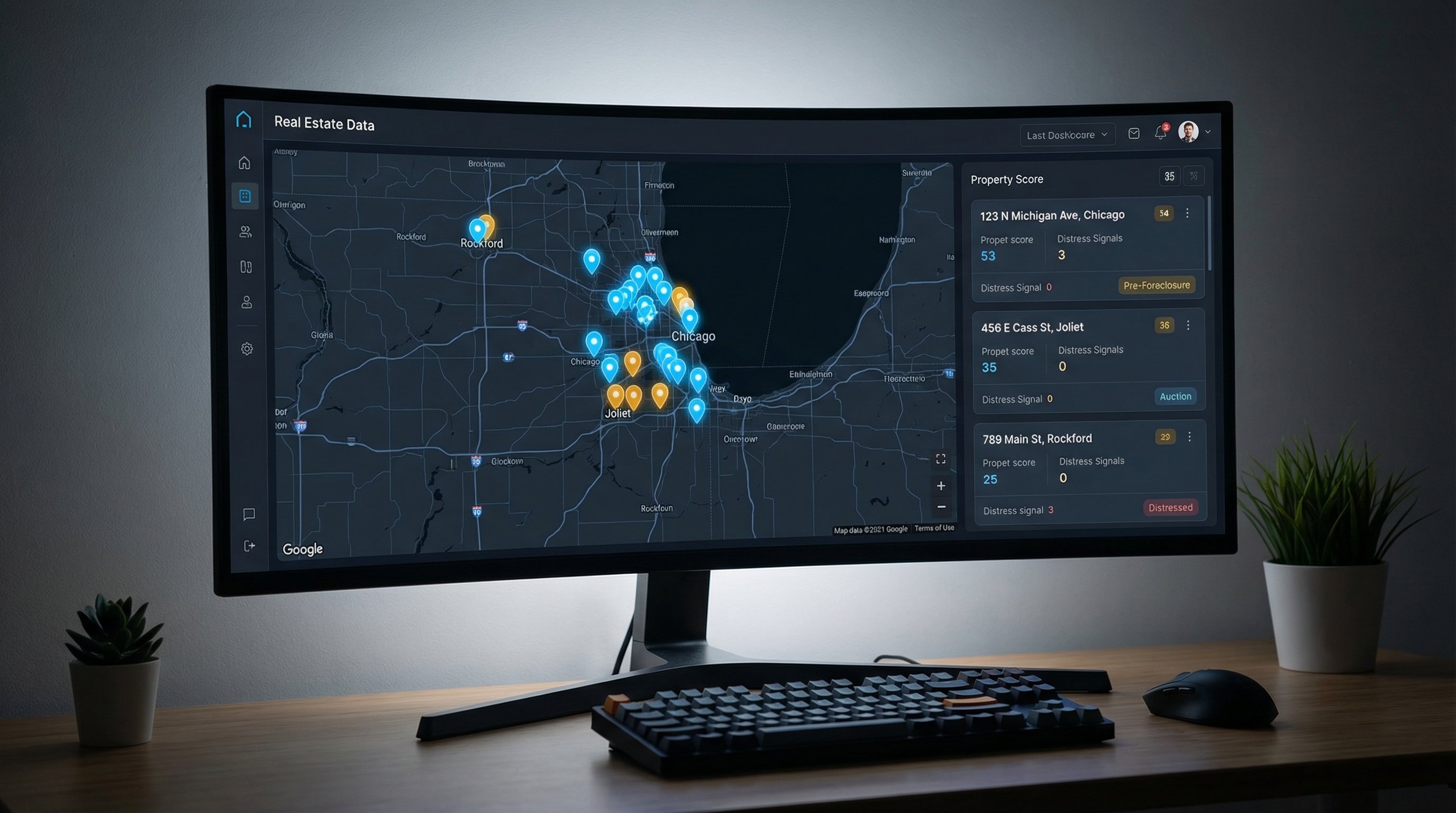

Aggregated Lead Platforms. Services like DistressIQ compile filings from multiple counties and stages into a single feed. For investors working across several Illinois counties, aggregation eliminates hours of manual research per week and reduces the risk of missing time-sensitive filings that competitors might catch first. The best platforms also layer additional distress signals, such as tax delinquency status and vacancy indicators, directly onto foreclosure records.

Building a County-by-County Pipeline

A scattergun approach across 102 counties wastes resources. Effective investors target two to four high-volume counties with consistent monitoring.

Pick the markets. Cook County is the starting point given its 40% share. Add collar counties based on strategy: DuPage for higher-margin flips, Will or Kane for wholesale volume, Lake for a mix.

Set stage filters. Wholesale investors should focus on pre-filing and early filings where homeowner motivation is building. Fix-and-flip buyers may prefer judgment-stage leads where the sale date is known and the acquisition path is clearer.

Layer distress signals. A property in foreclosure plus tax delinquency, code violations, or vacancy reports is a stronger lead than foreclosure alone. Stacking indicators increases the probability of closing.

Time the outreach. The Illinois timeline is long, but the optimal contact window is narrow. Outreach too early yields low response because the homeowner has not yet accepted the situation. Outreach too late leaves no negotiation room because the redemption period is expiring and the homeowner has run out of options. The sweet spot typically falls 2 to 4 months after filing, when the reality of the foreclosure has set in but the homeowner still has enough runway to consider a sale.

Common Mistakes

Ignoring redemption. A foreclosure judgment does not mean the deal is done. The redemption period gives the homeowner months to reverse the process. Contracts should include contingencies for reinstatement.

Overlooking reinstatement rights. The 90-day reinstatement window after judgment cannot be waived. If a borrower cures the default during this period, the deal collapses. Experienced investors either time outreach to fall after this window or build fallback provisions into purchase agreements.

Focusing only on Cook. Cook County's volume attracts every wholesaler and flipper in the Chicago metro. Collar counties offer lower competition and, in some cases, wider spreads between acquisition cost and after-repair value.

Relying on one source. Court records miss pre-filing leads. Sheriff's lists miss early-stage filings. The clearest picture comes from combining court filings, recorder data, tax records, and aggregated feeds.

Legal Considerations

The Illinois Home Repair and Remodeling Act and the Consumer Fraud and Deceptive Business Practices Act impose requirements on anyone soliciting business from distressed homeowners. All outreach must be transparent, offers documented clearly, and homeowners given the opportunity to seek independent counsel.

Property taxes also warrant attention. Illinois carries some of the highest property tax rates in the country, with Cook County averaging roughly 2.1% of assessed value. A discounted foreclosure acquisition may still carry a tax burden that compresses margins. Verify current tax bills and outstanding liens before closing.

If the property is occupied, eviction may be necessary. Illinois provides tenants and former owners with specific notice periods and procedural protections that can add 30 to 90 days before the property is available for renovation. Investors should factor these holding costs into their offer calculations, particularly in Cook County where eviction backlogs can push timelines toward the longer end of that range.

FAQ

Q: How long does the foreclosure process take in Illinois?

The full process typically runs 12 to 24 months from filing through sheriff's sale. This timeline is driven by mandatory waiting periods under the Illinois Mortgage Foreclosure Law, including the grace notice period, the time between filing and judgment, and the statutory redemption period. Cook County cases sometimes run longer due to court backlog, while smaller counties like Kane and Will may process cases closer to the 12-month end. Investors should plan outreach and negotiation timelines around this extended window rather than assuming a quick resolution.

Q: What is the redemption period for Illinois foreclosures?

Illinois grants a redemption period of either 7 months from service of the foreclosure summons or 3 months from the foreclosure judgment, whichever falls later. During this period, the homeowner can reclaim the property by paying the full judgment amount plus costs. This is a statutory right that cannot be waived by the lender. For investors, the redemption period means a purchase agreement signed during this window carries execution risk until the period expires and the deal can close.

Q: Can a homeowner stop a foreclosure after judgment?

Yes. Illinois law provides a right of reinstatement for up to 90 days after the foreclosure judgment. Reinstatement means paying the overdue payments, late fees, and costs to bring the loan current. This is separate from redemption, which requires paying the full balance. If the homeowner reinstates, the foreclosure is dismissed. Investors negotiating during this window should account for the possibility of reinstatement and structure contracts accordingly, either with contingencies or by timing outreach after the 90-day period ends.

Q: Which Illinois counties have the most foreclosure filings?

Cook County accounts for approximately 40% of all Illinois filings, with the Chicago neighborhoods of Austin, Englewood, and South Shore producing the highest concentration. Beyond Cook, DuPage, Lake, Will, and Kane counties generate the next tier of volume. Will County communities along I-55, including Joliet and Bolingbrook, have seen elevated activity as rising costs pressure household budgets. Investors should focus pipeline efforts on these high-volume counties rather than spreading resources across all 102 counties.

Q: What is the earliest signal for a foreclosure lead in Illinois?

The earliest signal is the pre-filing grace notice. Illinois law requires lenders to mail a formal notice at least 30 days before filing a court action. This notice is not part of the court record, so standard case searches will not find it. Specialized data aggregators track these pre-filing signals by monitoring lender activity and early-stage default indicators. Investors who capture leads at this stage have the longest runway for outreach and negotiation, often months before competitors see the filing.

Q: Do Illinois foreclosure properties come with tenants?

Some do. If the property was a rental, the tenant may still occupy it when the investor acquires it. Illinois tenant protection laws require proper notice before eviction, with timelines varying by lease terms and payment status. Investors should verify occupancy before closing and budget for potential eviction costs and delays, which can add one to three months to the hold period before renovation work can begin.

For investors ready to build a targeted foreclosure pipeline across Illinois counties, DistressIQ aggregates pre-filing notices, court filings, and judgment-stage leads into a single feed with county-level filters, stage tracking, and stacked distress signals. Visit distressiq.ai to explore live Illinois foreclosure data.

Sources

- Illinois General Assembly, "Illinois Mortgage Foreclosure Law," 735 ILCS 5/Art. XV

- Cook County Circuit Court, Chancery Division Foreclosure Case Search

- Illinois Attorney General, "Homeowner Protection Act and Foreclosure Resources"

The data behind this article

DistressIQ Monitors These Signals in Real Time

Pre-Foreclosures

NOD + NTS filings

Tax Delinquency

County treasurer records

Code Violations

Municipal inspection filings

Probate Filings

Superior Court records

Every lead is scored 0–100 for seller motivation based on signal type, duration, severity, and stacking. Nationwide coverage — every US county, updated daily.

Ready to find deals in your market?

See Live Distress Signals in Your County

Stop calling dead leads. Every lead in DistressIQ is scored 0–100 for seller motivation, with verified contact info included. Browse the free tier to see what's active in your market right now.

Browse Free Leads — No Credit Card