Bankruptcy Leads in Florida: How Investors Find Chapter 13 Filings Before the Market Does

Bankruptcy Leads in Florida: How Investors Find Chapter 13 Filings Before the Market Does

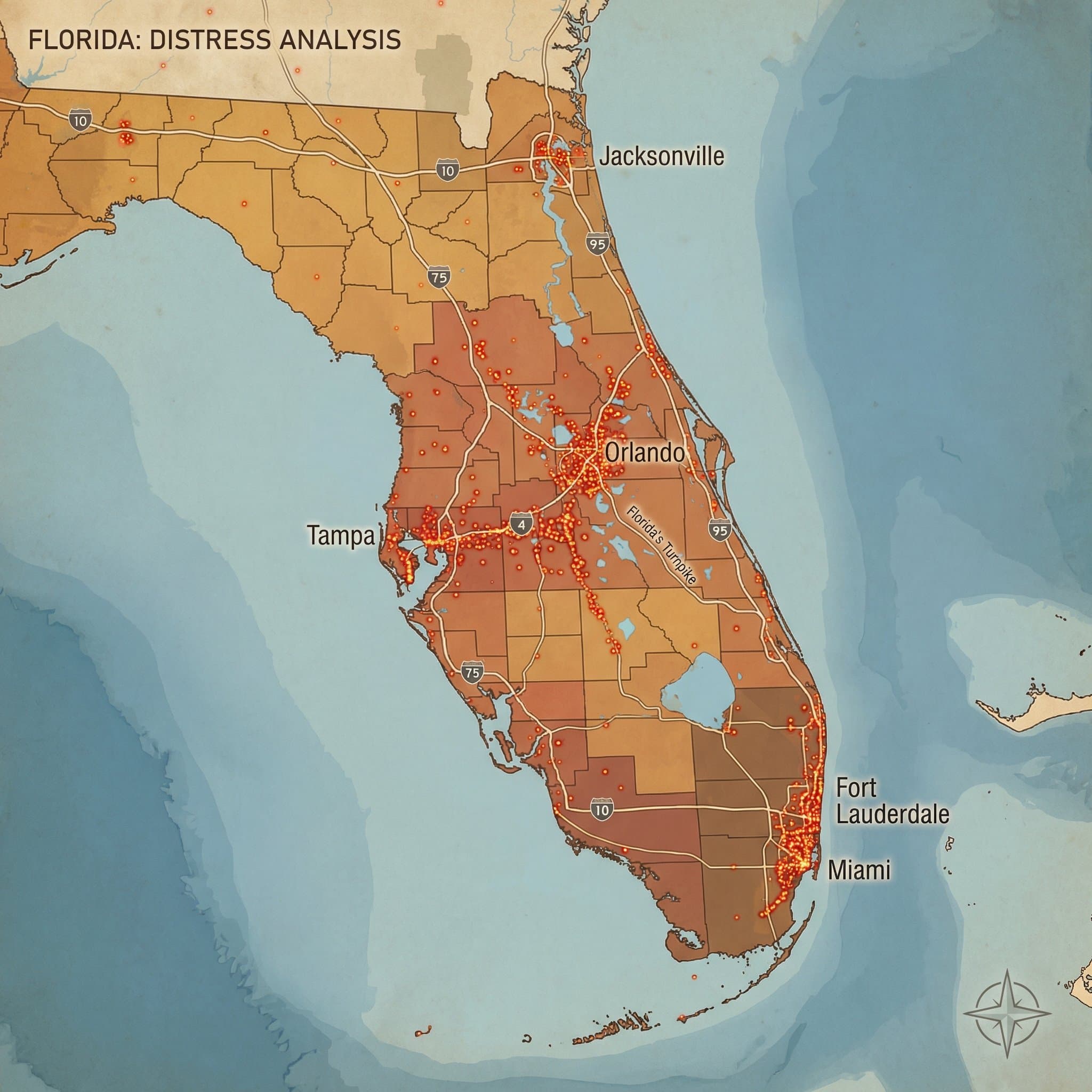

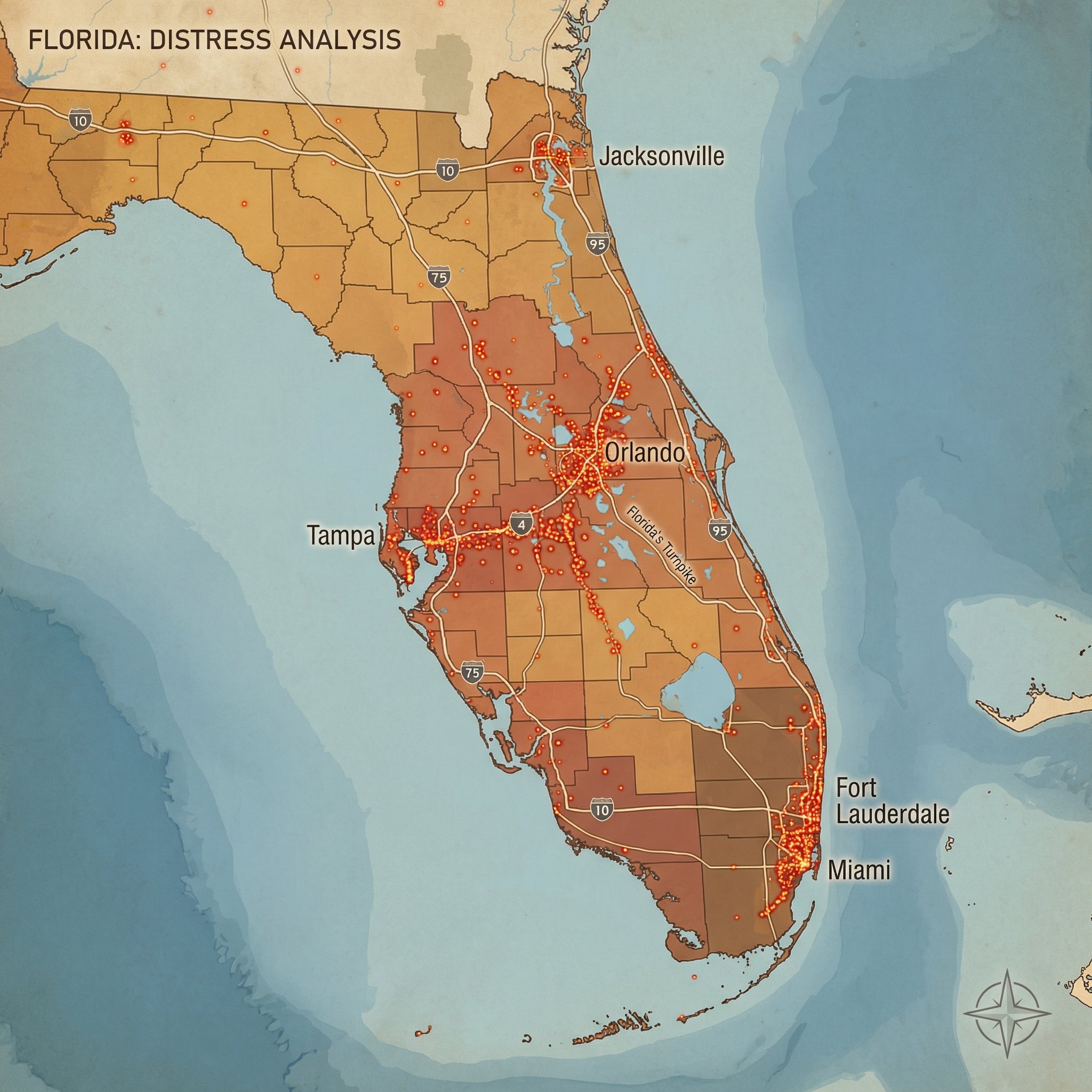

TL;DR: Florida bankruptcy filings represent motivated sellers often overlooked by competitors. Chapter 13 cases are particularly valuable for investors because repayment plans create concrete timelines and the automatic stay gives homeowners a narrow window to sell before the trustee takes over. Florida ranked 3rd nationally in Chapter 13 filings in 2025. DistressIQ aggregates these signals across all Florida counties so investors can act before the trustee lists the property publicly.

Most real estate investors have never made a single offer through a bankruptcy case. That is a problem. It means they compete with every other wholesaler and agent for the same distressed inventory while ignoring a parallel pipeline where competition is thinner and motivation is documented in federal court filings.

Florida bankruptcy leads deserve a closer look. The state processed approximately 72,000 Chapter 13 filings in 2025, placing it behind only California and Texas in total volume. These homeowners signed a court document admitting they cannot pay their debts and committed to a repayment schedule. When circumstances derail that schedule, the property becomes a forced sale.

Why Florida Produces More Bankruptcy Leads Than Most States

Florida has structural features that keep bankruptcy filings elevated relative to other large states.

The homestead exemption creates unusual dynamics. Florida Constitution Article X, Section 4 protects primary residence equity without limit. This often pushes debtors into Chapter 13 because they want to keep the homestead while reorganizing other debts. When the plan fails, these homeowners are highly motivated to sell quickly before the trustee takes control of estate assets.

Volatile income patterns affect a large segment of the workforce. Seasonal employment in hospitality, retail, and food service means Florida households experience income swings that undermine court-approved repayment plans. A worker who files Chapter 13 after a slow winter season may have a budget that does not account for losing overtime. When the plan fails, the trustee moves to liquidate non-exempt assets, often including investment properties or rental homes.

Short-term rental disruptions created a wave of investor bankruptcies. Between 2022 and 2024, Florida property investors who borrowed against short-term rental properties at peak valuations faced unsustainable debt service when interest rates reset. Chapter 13 filings among investors with multiple properties increased significantly during this period.

Chapter 13 vs. Chapter 7: What Investors Need to Understand

The distinction between Chapter 7 and Chapter 13 matters more for real estate investors than almost any other buyer type.

Chapter 7 bankruptcy is liquidation. The trustee identifies non-exempt assets and sells them to repay creditors. For real estate, this typically means the debtor has little or no equity in the property. Most Chapter 7 debtors reaffirm their mortgage and keep making payments. These cases are not useful for investors unless there is substantial equity the trustee must unlock.

Chapter 13 bankruptcy is reorganization. The debtor proposes a 3-to-5-year repayment plan. This is the investor sweet spot. Chapter 13 filers often have equity in their properties, which they use as collateral against the repayment plan. When the plan fails, the trustee is required to liquidate assets. The trustee becomes a motivated counterparty who must sell, and that is the moment to make an offer. The window between a missed plan payment and the trustee listing the property typically runs 45 to 90 days. An investor who identifies this window early can negotiate directly with the debtor before the property enters a public auction where trustee sales command 60 to 80 cents on assessed value.

How Florida Bankruptcy Court Works for Real Estate Investors

Florida bankruptcy cases are filed in the Middle District (Tampa), Northern District (Pensacola and Tallahassee), and Southern District (Miami and West Palm Beach). Each district has its own procedures and trustee rotation, which affects how quickly cases move and how responsive trustees are to investor inquiries.

The automatic stay is both a constraint and an opportunity. Federal law halts all foreclosure proceedings, creditor lawsuits, and debt collection the moment someone files bankruptcy. For an investor, this creates a unique negotiation environment. The homeowner is legally prohibited from selling without court approval, but they desperately want to sell before the trustee takes control. This pressure often produces motivated sellers who accept below-market offers in exchange for a clean, fast closing that resolves their bankruptcy case.

The Chapter 13 trustee conducts the 341 meeting within 30 to 45 days of filing. At this meeting, the trustee reviews the petition and plan, assessing whether the plan is feasible and whether assets must be liquidated. Investors who monitor these meetings gain intelligence about which cases are likely to succeed. Florida's three bankruptcy districts publish 341 meeting calendars publicly, and DistressIQ aggregates these filings with property addresses cross-referenced against county assessor records.

Trustee sale procedures differ from standard foreclosure sales. When a Chapter 13 case fails, the property is sold through the bankruptcy estate under federal law rather than state foreclosure statutes. The Southern District of Florida typically sees trustee sales completed within 120 days of case dismissal. The Middle District may take 180 days or longer depending on the trustee caseload.

Free Weekly Alerts

See What's Distressed in Your Market

Get free weekly alerts — new distressed properties, motivation scores, and hot neighborhoods in your area. Addresses and contact info available inside DistressIQ.

Free forever · No credit card · Unsubscribe anytime

What Florida Bankruptcy Filings Signal About Property Condition

Bankruptcy cases produce a paper trail that sophisticated investors use to assess deal quality before making an offer. The petition includes Schedule A (real property) and Schedule D (secured debt), which together tell an investor exactly what the property is worth on paper and how much debt is attached.

Loan-to-value ratios above 95% are common in Florida Chapter 13 cases. Schedule D filings consistently show properties where secured debt exceeds current market value. Investors who understand this can structure offers that satisfy the mortgage lender while leaving room for negotiation. Often, the lender prefers a short sale through the bankruptcy court rather than a foreclosure.

Properties with multiple secured creditors create negotiating leverage. Schedule D lists all secured creditors in order of priority. A property with a first mortgage, second mortgage, and HELOC has three lenders who must approve any sale. Investors who understand the creditor hierarchy can approach the first mortgage holder with an offer that pays the first lien in full while leaving junior lienholders with nothing.

The Florida-Specific Investor Trap to Avoid

There is one pattern that trips up investors new to Florida bankruptcy leads. The automatic stay protects the debtor from creditors, but it does not prevent the mortgage lender from seeking relief from the stay to pursue foreclosure. Lenders routinely file motions for stay relief in Chapter 13 cases, particularly when the debtor is behind on both plan payments and post-petition mortgage payments. A motion for relief from stay can be granted within 30 to 60 days of filing, at which point the lender resumes foreclosure. An investor who has been negotiating a purchase agreement for 90 days may suddenly find the property entering auction while the bankruptcy case is still open. The correct approach: negotiate purchase agreements that are contingent on court approval and include a clause releasing the buyer if the automatic stay is lifted within a specified period. Experienced bankruptcy attorneys draft these contingencies as standard practice.

How to Find Bankruptcy Leads in Florida Counties

Public access to PACER (Public Access to Court Electronic Records) gives anyone the ability to search Florida bankruptcy filings by county, case type, and filing date. However, PACER returns docket entries without property addresses cross-referenced against distress signals, which makes monitoring multiple counties simultaneously impractical. DistressIQ aggregates these filings and cross-references them against county assessor records to surface the property address, estimated value, lien position, and current trustee status.

For Miami-Dade and Broward markets, the Southern District's high-volume docket means trustee sales occur weekly. Investors targeting this area should monitor dismissed Chapter 13 cases on a rolling 30-day basis. A case dismissed within 60 days of filing signals that the plan was not viable and the debtor may be willing to sell at a discount rather than file again.

In the Tampa Bay area, investors should focus on Pinellas, Hillsborough, and Pasco counties where rental property concentration is highest. Trustee sales in these counties often involve investment properties with existing tenants, complexity that retail buyers cannot navigate but experienced landlords can monetize.

Working With the Chapter 13 Trustee: What to Expect

Once a Chapter 13 case fails and the trustee begins the liquidation process, the investor enters a different negotiation dynamic. The trustee has a fiduciary duty to the bankruptcy estate and must obtain the best price reasonably available. In practice, trustees frequently accept offers below market value because their priority is completing the sale quickly and returning proceeds to creditors.

Trustees in Florida charge a commission on sales. The standard Chapter 13 trustee commission runs between 3% and 6% of the sale price depending on the district. This commission is paid from estate assets before unsecured creditors receive anything. An investor who structures a deal at 75% of market value effectively negotiates against the trustee commission, since the trustee calculates net proceeds to creditors rather than gross sale price.

Court approval typically takes 30 to 45 days from offer acceptance. The trustee files a motion to sell, serves notice on all creditors, and waits for objections. If no objections are filed within 14 days, the court enters an order approving the sale. Investors should plan for a 60-day closing timeline from the date of initial offer acceptance.

See how DistressIQ surfaces bankruptcy leads across all 67 Florida counties, updated daily from public federal court records and county assessor data at distressiq.ai. Browse the map, filter by Chapter 13 case status, and sort by estimated equity position. Founding member pricing starts at $89 per month for Starter, with Pro at $174 and Elite at $349 per month.

Frequently Asked Questions

Q: What is the difference between Chapter 7 and Chapter 13 bankruptcy for real estate investors?

Chapter 7 is liquidation, typically with little equity to unlock for investors. Chapter 13 is reorganization with a repayment plan, and when those plans fail, trustees often must sell assets. Chapter 13 cases are where investors find motivated sellers with documented financial distress and court oversight that ensures a clean transaction.

Q: How do investors find Florida bankruptcy filings before the trustee lists the property?

PACER provides direct access, but it requires manual effort and does not cross-reference property addresses against assessor records. DistressIQ aggregates Florida Chapter 13 filings and displays the associated property address, estimated value, lien amounts, and trustee status in a map view, so investors can identify cases likely to fail before they appear on a public auction list.

Q: Can an investor negotiate directly with a debtor in an active Chapter 13 case?

Yes, but any purchase agreement must be contingent on court approval and include a stay-relief clause that releases the buyer if the automatic stay is lifted. Purchasing estate property without court authorization violates federal bankruptcy law and can result in sanctions.

Q: What happens when a Chapter 13 case is dismissed?

The automatic stay lifts, the debtor regains the ability to sell independently, and the mortgage lender can resume foreclosure. Investors with a purchase agreement in place can often close within 30 days before foreclosure restarts.

Q: How long does a trustee sale take in Florida bankruptcy cases?

Florida bankruptcy trustee sales typically run 60 to 90 days from offer acceptance to closing. The court approval process takes 30 to 45 days. The Southern District generally moves faster than the Middle District.

Q: Are bankruptcy leads in Florida typically in worse condition than other distressed properties?

Not necessarily. Bankruptcy filings reflect financial distress, not property condition. Some Chapter 13 filers own well-maintained homes; others own properties with deferred maintenance. County assessor records provide an independent estimate to assess condition relative to value.

Q: What Florida counties have the most Chapter 13 bankruptcy activity?

Miami-Dade, Broward, Palm Beach, Hillsborough, and Orange counties account for the highest volume. These urban and suburban markets have the highest concentration of investment properties and HELOCs that push households into Chapter 13 when income disruptions occur.

Sources: American Bankruptcy Institute 2025 Annual Filing Report; U.S. Courts Administrative Office Statistical Tables for Chapter 13 filings by state; Florida Constitution Article X, Section 4 (homestead exemption).

The data behind this article

DistressIQ Monitors These Signals in Real Time

Pre-Foreclosures

NOD + NTS filings

Tax Delinquency

County treasurer records

Code Violations

Municipal inspection filings

Probate Filings

Superior Court records

Every lead is scored 0–100 for seller motivation based on signal type, duration, severity, and stacking. Nationwide coverage — every US county, updated daily.

Ready to find deals in your market?

See Live Distress Signals in Your County

Stop calling dead leads. Every lead in DistressIQ is scored 0–100 for seller motivation, with verified contact info included. Browse the free tier to see what's active in your market right now.

Browse Free Leads — No Credit Card