Tax Delinquent Property List Colorado: How Investors Find and Work Them in 2026

Tax Delinquent Property List Colorado: How Investors Find and Work Them in 2026

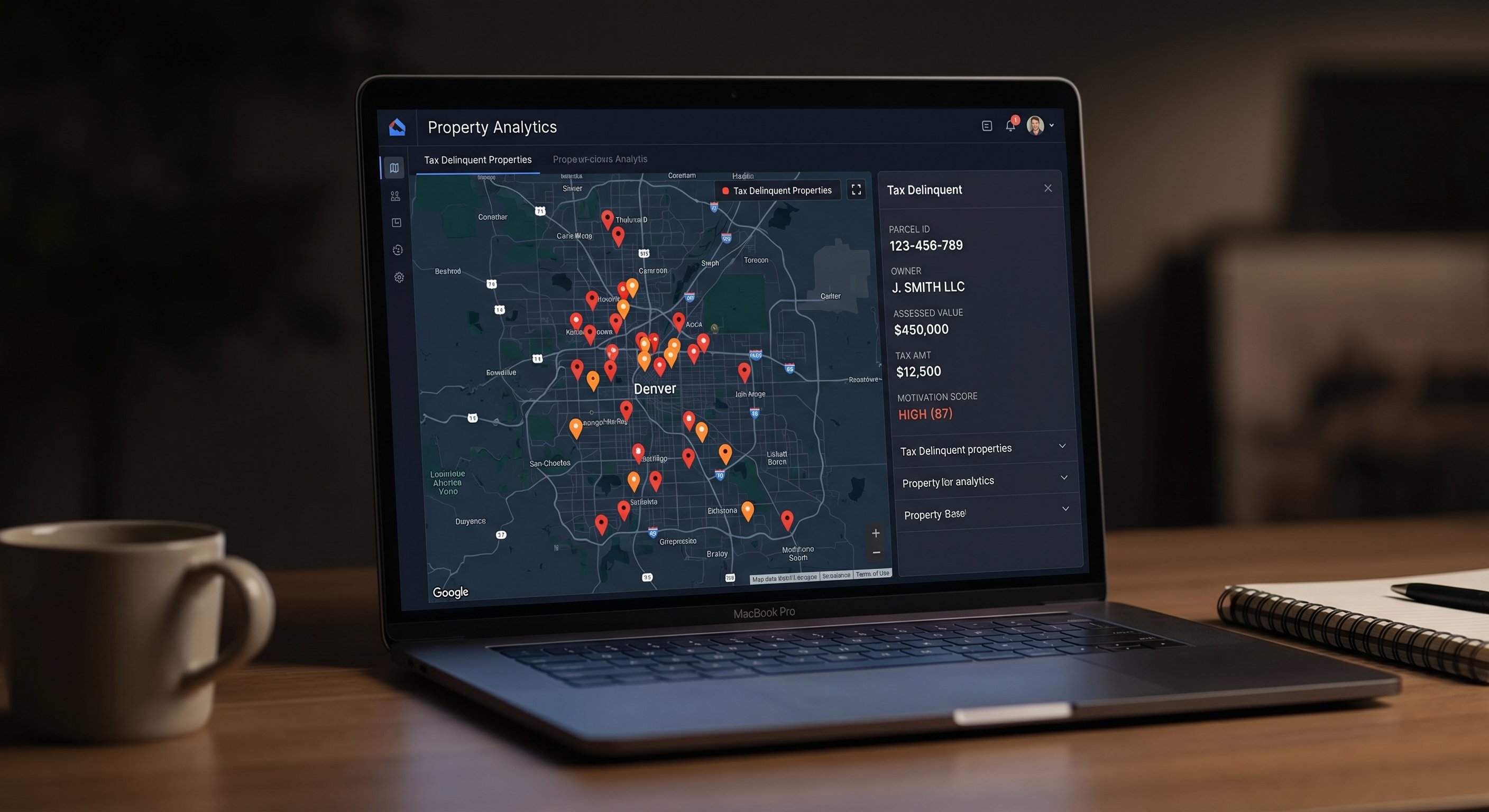

TL;DR: Colorado counties sell tax liens annually at public auction, typically in December. Investors bid downward on interest rates to win liens, then earn returns when property owners redeem within the 3-year redemption period. Properties that fail to redeem become tax deeds, which investors can acquire at a subsequent public auction. DistressIQ aggregates tax delinquent properties across Colorado's most active counties, showing property details, assessed values, and distress signals before the sale date arrives.

Colorado's property tax system runs quietly in the background of one of the country's most dynamic real estate markets. Every year, across counties from Denver to Grand Junction, homeowners fall behind on property taxes for reasons ranging from inheritance disputes to investment property cash flow problems. When that happens, counties move to collect through a formal process that has existed in some form since the Colorado territorial era.

For real estate investors who understand how this process works, the tax delinquent property list in Colorado represents one of the most legally cleanest ways to acquire real estate below market value. No negotiations with motivated sellers. No wondering whether the deal will fall through at the title company. The county has already done the enforcement work. Your job is to show up at the right auction with the right research.

Why Tax Delinquency Creates Investor Opportunities in Colorado

Property tax delinquency does not happen overnight. By Colorado statute, a property must be at least 90 days delinquent before a county can initiate the tax sale process. In practice, many counties wait significantly longer, accumulating multiple years of unpaid taxes, special assessments, and associated penalties before scheduling a public sale.

The typical profile of a tax delinquent property in Colorado includes several patterns that investors should recognize.

Investment properties with absent owners represent a substantial portion of delinquent parcels. Colorado's ski resort economy, military presence at bases in El Paso County, and remote work migration have created a class of out-of-state property owners who sometimes lose track of tax obligations on second homes or rental properties. These owners are often highly motivated to resolve the situation cleanly once they become aware of it, which makes redemption rates on these properties relatively high and the investment thesis straightforward.

Probate and estate properties frequently surface on tax delinquent lists. When a property owner passes away, property tax obligations transfer to the estate. If the estate lacks sufficient liquid assets to cover tax bills while the probate process runs its course, delinquency follows. These situations can move quickly and often resolve when heirs decide whether to keep or sell the property.

Properties with tax assessment disputes create another category of delinquency. Colorado's residential assessment rate is tied to market conditions under the Gallagher Amendment framework, which has been repealed but whose effects linger. Some owners who disagree with their assessed value engage in deliberate non-payment as a form of protest, not realizing the full consequences. These cases can produce motivated sellers who simply want the situation resolved.

The key variable for investors is recency and stacking. A property that is one year delinquent behaves differently than one that is three years delinquent. A property with a tax lien plus an open building permit plus a recent bankruptcy filing presents a far more compelling acquisition opportunity than one with a tax lien alone. This stacking logic underpins how modern property intelligence platforms score and surface the most actionable tax delinquent leads.

Colorado's Tax Sale Structure: Liens Before Deeds

Colorado operates as a tax lien state, not a tax deed state. This distinction matters significantly for investors because it determines the investment vehicle, the risk profile, and the exit strategy.

When a property becomes tax delinquent, the county holds a public auction where investors purchase tax lien certificates. The certificate represents the investor's right to collect the delinquent taxes plus interest from the property owner during a redemption period. In Colorado, that redemption period runs for three years from the date of the sale.

Bidders compete by offering the lowest interest rate they will accept on their investment. This is a reverse auction. If the county sets the minimum acceptable rate at 8 percent, an investor who bids 5 percent wins the lien. The winning bid rate becomes the rate the property owner must pay to redeem, within statutory caps that vary by property type. For residential properties, the maximum rate is typically 12 percent per year on the delinquent amount.

Once an investor holds a tax lien certificate, they have a secured interest in the property. If the property owner redeems during the three-year period, the investor receives the delinquent taxes plus the bid interest rate. If the owner does not redeem, the investor can apply for a tax deed on the property, which transfers ownership after the county confirms no other parties have a redemption right.

Colorado law requires counties to offer surplus proceeds sales in many cases where the tax lien exceeds the property's assessed value. This means investors sometimes acquire properties with meaningful equity even after paying delinquent taxes in full.

Where the Action Is: Colorado's Most Active Counties for Tax Delinquent Properties

Not all Colorado counties generate the same volume of tax delinquent opportunities. The Colorado Division of Property Taxation oversees assessment for all 64 counties, but each county manages its own tax sale process, with timing and procedures varying slightly. Investors who understand the geographic concentration of opportunities can allocate their research time more efficiently.

Denver County processes a high volume of tax delinquent properties given its urban density and significant investment property market. The annual sale typically occurs in December at the Denver County Administration Building. Properties range from single-family homes in neighborhoods like Park Hill and Stapleton to small multi-unit buildings in established urban corridors. The Denver assessor's office publishes delinquency lists approximately 60 days before the sale, giving investors a meaningful research window.

El Paso County (Colorado Springs) represents one of the most active markets for tax sales outside the Denver metro. The county's large geographic footprint, military community, and growing population generate consistent delinquency volume. The El Paso County Treasurer's office conducts sales in early December, and properties in the Black Forest, Mountain View, and central Colorado Springs areas appear regularly.

Arapahoe, Jefferson, and Adams counties round out the Denver metropolitan tax sale circuit. These suburban counties often have shorter redemption periods in practice due to higher property values and more active real estate markets. Properties that do not redeem frequently result in tax deed applications within 18 to 24 months of the original sale.

Larimer County (Fort Collins) and Boulder County offer opportunities in Northern Colorado's tech and university-adjacent markets. Larimer County's sale typically occurs in late November or early December, with good representation from college-area rental properties and residential homes.

Mesa County (Grand Junction) and Pueblo County provide exposure to Western Slope and Southern Colorado markets where property values are lower but cap rates on tax lien investments can be more attractive. These counties see more agricultural and small residential property delinquency.

Investors using a platform with county-direct data integration can monitor delinquency filings across all Colorado counties simultaneously, surfacing opportunities weeks before the public sale list is formally published. The research window matters: properties that appear on formal sale lists are visible to every other investor paying attention.

Free Weekly Alerts

See What's Distressed in Your Market

Get free weekly alerts — new distressed properties, motivation scores, and hot neighborhoods in your area. Addresses and contact info available inside DistressIQ.

Free forever · No credit card · Unsubscribe anytime

How to Research Tax Delinquent Properties Before the Auction

Successful tax lien investors in Colorado do not show up at the sale blind. The research process involves three distinct phases, each addressing a different source of risk.

Phase one is verifying the property details. The county assessor's record confirms the parcel number, legal description, assessed value, and current owner of record. This information is publicly available through the Colorado Property Assessment and Taxation system (PAR据) and through individual county assessor websites. Investors confirm whether the property matches what they expect and identify any discrepancies that could affect title.

Phase two is reviewing the delinquency history. A property that is one year delinquent behaves differently than one with three years of accumulated taxes. The delinquency amount, the number of years delinquent, and any prior redemption attempts all affect the investment calculus. Properties with multiple years of delinquency often indicate either an unresponsive owner or an title issue that needs resolution.

Phase three is evaluating the property itself. This means pulling any available property characteristic data, reviewing recent sales in the neighborhood to estimate after-repair value, and checking for code violations, open building permits, or other distress signals that might affect the property's value or the owner's motivation to redeem. Google Street View and satellite imagery provide a first-level view, but platforms that integrate assessor data with visible distress indicators give a more complete picture.

The Redemption Risk: What Happens When Property Owners Pay Back

The redemption mechanism is central to the tax lien investment model, and investors in Colorado should understand both the opportunity and the risk it represents.

When a property owner redeems a tax lien certificate, they pay the investor the full delinquent tax amount plus interest at the rate specified by the winning bid. This is a guaranteed return within the bounds of the bid rate and the redemption timeline. On a residential property with a three-year redemption period and an 8 percent bid rate, the investor earns a total return of approximately 26 percent over the holding period on the tax amount invested.

The risk is straightforward: if the property owner redeems quickly, the investor's capital is tied up until redemption occurs. If the investor needs capital for other deals, a three-year lock-up can constrain overall returns. Colorado does not allow for early certificate assignment in all circumstances, which limits the secondary market for these instruments.

Properties that do not redeem within the three-year period transition to the tax deed stage. At that point, the investor has a legal pathway to ownership, but additional steps are required, including public notice periods and potential challenges from other lien holders.

DistressIQ surfaces properties with tax delinquency signals alongside other distress indicators, allowing investors to build a portfolio view of opportunities across Colorado counties without tab-switching between individual county websites. The after-repair value calculation, the delinquency stack, and the estimated time to title resolution all inform whether a specific property fits an investor's acquisition strategy.

Tax Deed Opportunities: The Next Stage After the Lien Sale

Properties that fail to redeem become tax deed properties, which counties offer at public auction or private sale. The tax deed represents full ownership transfer, but investors should be aware of title risks that can accompany these transactions.

Colorado law requires counties to provide notice to affected parties before issuing a tax deed, but junior lien holders who fail to respond may lose their interests. The county deed is generally considered a clean conveyance, but an investor acquiring a tax deed should budget for a title insurance policy to protect against any undiscovered prior claims.

Tax deed properties in Colorado's mountain resort counties (Aspen, Vail, Telluride) occasionally surface with assessed values in the hundreds of thousands of dollars while delinquent taxes represent only a fraction of that amount. These opportunities are rare but worth watching for investors with access to the capital required to compete at auction.

Building a Colorado Tax Delinquent Property List Workflow

Experienced investors who work tax delinquent properties in Colorado tend to follow a consistent workflow that they refine with each cycle.

The research phase begins eight to twelve weeks before the anticipated sale date. Investors pull the county assessor's pre-sale list, filter for properties matching their acquisition criteria (location, property type, assessed value range, delinquency amount), and build a shortlist. This is the phase where platforms that aggregate county-direct data save the most time.

The shortlist phase involves physical and digital reconnaissance. Satellite imagery, street-level photos, and neighborhood sales data all feed into an after-repair value estimate. Properties whose ARV significantly exceeds the likely total investment (delinquent taxes plus purchase price at auction plus holding costs) move to the active list.

The auction phase requires careful attention to registration requirements, bidding procedures, and payment terms at the specific county conducting the sale. Each county has slightly different rules about payment methods, deposits, and bidding increments. Investors who have not attended a specific county's sale should contact the county treasurer's office in advance to confirm procedures.

The holding phase spans the three-year redemption period. Investors track redemption activity on their certificates, maintain contact records for property owners who may be working toward redemption, and watch for anyLis Pendens filings or bankruptcy proceedings that could affect their position.

The deed acquisition phase, for certificates that go unredeemed, involves filing an application with the county, publishing legal notice, and attending any required auction if multiple parties claim the deed right. Most investors who hold certificates to redemption or deed acquisition report the entire cycle takes three to four years from initial purchase.

How DistressIQ Surfaces Tax Delinquent Opportunities in Colorado

The public sale list is only part of the picture. Colorado counties generate ongoing delinquency data throughout the year, not just at the annual sale. Properties fall behind on taxes continuously, and investors who wait for the formal pre-sale list are competing with everyone else who was paying attention.

DistressIQ aggregates tax delinquency signals from county assessor and treasurer records across 3,200-plus counties nationwide, including all 64 Colorado counties. The platform updates property records daily and flags new tax delinquent activity as it surfaces. A property that becomes 90 days delinquent in Arapahoe County in February is visible to DistressIQ users before the formal list for the December sale is even compiled.

The platform stacks tax delinquency signals alongside other distress indicators, including open building permits, bankruptcy filings, code violations, and ownership transfer records. This multi-signal approach helps investors identify properties with compounding distress signals, which often present stronger acquisition opportunities than single-signal properties.

Street View and aerial imagery are included on every property record, allowing investors to assess property condition and neighborhood context without driving the block. The assessed value from county records provides a baseline for ARV calculations. When the county assessor data and the visible property condition diverge significantly, that gap is worth investigating.

Property data on DistressIQ comes directly from county assessor records, not MLS. MLS data is compiled by listing agents for marketing purposes and frequently contains estimated or inaccurate square footage, bedroom counts, and lot dimensions. County assessor records are the legal basis for property taxation and carry different accuracy standards.

What Investors Should Know Before the Next Colorado Tax Sale

Colorado's tax sale season runs from late November through December across most counties. The specific dates vary, and investors should confirm timing with each county treasurer's office. For the 2026 sale cycle, most counties will publish preliminary lists in October and November.

The key variables that determine whether a tax delinquent property is worth pursuing are the delinquency amount relative to assessed value, the property type and condition, the neighborhood comps, and the owner's known circumstances. A property assessed at $400,000 with $8,000 in delinquent taxes represents a very different opportunity than a property assessed at $400,000 with $45,000 in delinquent taxes. The ratio matters more than the absolute dollar amount.

Colorado's legal framework for tax liens and deeds is mature and investor-friendly relative to many states. The three-year redemption period is statutory, the interest rate caps are clear, and the county deed process is well-established. For investors who do the research and follow the process, the system produces genuine off-market acquisition opportunities with clean title pathways.

The main constraint for most investors is capital availability and holding capacity. Tying up investment capital for three years requires planning. Investors running this strategy alongside other acquisition approaches should model the capital flow implications before committing to a large certificate portfolio.

For investors ready to move beyond county websites and individual sale lists, the combination of a structured research process and a platform that aggregates county-direct data across Colorado's most active counties represents the current standard for tax delinquent property analysis in the state. The Colorado Department of Revenue oversees property tax administration statewide, and the Colorado Division of Property Taxation provides assessment guidelines that govern how counties calculate and collect delinquent taxes. Investors can verify sale dates and procedures through individual county treasurer's offices, with the Denver Treasurer's Office providing a model for how urban county sales are conducted.

See distressed properties with tax delinquency signals across Colorado counties, updated daily from county assessor records. Browse free on DistressIQ.

Frequently Asked Questions

Q: How does the Colorado tax lien auction work?

Colorado counties hold annual tax lien sales where investors purchase certificates by bidding downward on interest rates. The investor who accepts the lowest rate wins the lien. Property owners then have three years to redeem by paying the delinquent taxes plus interest at the winning bid rate. If they do not redeem, the investor can apply for a tax deed.

Q: What is the redemption period for tax liens in Colorado?

The standard redemption period in Colorado is three years from the date of the tax lien sale. During this period, the property owner can repay the delinquent taxes plus interest at the rate specified by the winning bid and reclaim clear title to the property.

Q: Are tax deed properties in Colorado riskier than tax lien certificates?

Tax deed properties involve full ownership transfer rather than a lien, which means different title risks. Properties acquired via tax deed should be covered by title insurance given the possibility of undiscovered junior liens. However, tax deeds also represent a cleaner path to ownership if the certificate holder follows the statutory process correctly.

Q: Which Colorado counties have the most tax delinquent properties?

Denver, El Paso (Colorado Springs), Arapahoe, Jefferson, and Adams counties consistently generate the highest volume of tax delinquent properties due to population density and investment property concentration. Mesa and Pueblo counties offer opportunities in Western and Southern Colorado with generally lower property values.

Q: Can out-of-state investors participate in Colorado tax sales?

Yes. Colorado's tax sale process does not restrict participation to state residents. Investors must register with the specific county treasurer's office before the sale, understand the payment requirements, and be prepared to hold the certificate for the full redemption period or pursue the deed if unredeemed.

The data behind this article

DistressIQ Monitors These Signals in Real Time

Pre-Foreclosures

NOD + NTS filings

Tax Delinquency

County treasurer records

Code Violations

Municipal inspection filings

Probate Filings

Superior Court records

Every lead is scored 0–100 for seller motivation based on signal type, duration, severity, and stacking. Nationwide coverage — every US county, updated daily.

Ready to find deals in your market?

See Live Distress Signals in Your County

Stop calling dead leads. Every lead in DistressIQ is scored 0–100 for seller motivation, with verified contact info included. Browse the free tier to see what's active in your market right now.

Browse Free Leads — No Credit Card