How to Find Pre-Foreclosure Leads in Indiana (2026 Investor Guide)

How to Find Pre-Foreclosure Leads in Indiana (2026 Investor Guide)

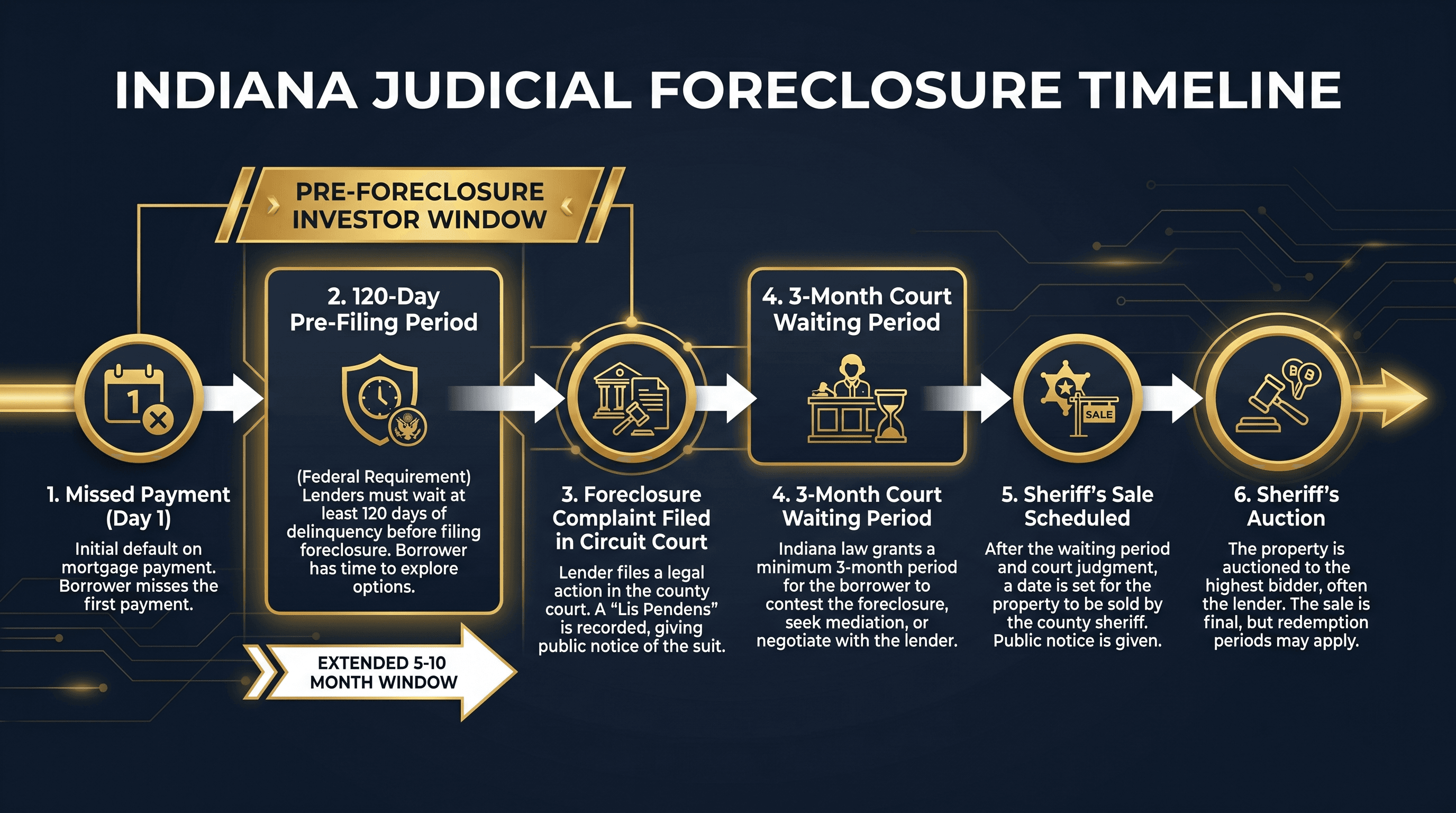

Most real estate investors hear "Indiana" and assume the state runs on the same fast-timeline model as neighboring Texas or Ohio. It does not. Indiana is a judicial foreclosure state, which means every foreclosure must clear the court system before a sheriff's sale can happen. The result: a pre-foreclosure window stretching five to ten months from the first missed payment to auction day.

That extended timeline is not a disadvantage. It is an invitation.

While investors in faster-moving states scramble to make contact within 60 to 90 days, Indiana homeowners in distress have months to weigh their options. They are reachable. They are negotiable. They want a way out that does not end with a public auction. The investor who understands Indiana's court-driven process and knows where to pull county-level filing data can work a wider, less crowded window than the national averages suggest.

This guide covers the mechanics of Indiana pre-foreclosure, where the data lives, how to prioritize leads by urgency, and what separates a productive Indiana pre-foreclosure workflow from a generic cold-calling operation.

Why Indiana's Judicial Foreclosure Timeline Is Actually an Investor Advantage

The standard investor concern about Indiana goes like this: judicial states take longer, so fewer deals happen. That reading misses what a longer timeline actually produces.

A homeowner with 90 days of runway before auction is in crisis mode. They are not evaluating offers. They are surviving. A homeowner with five months of runway has time to think, compare options, and make a rational decision about whether selling before sheriff's sale is worth it. That homeowner answers the phone. That homeowner negotiates.

Indiana Code Title 32 governs the foreclosure process, and it builds in deliberate waiting periods at every stage. Federal mortgage servicing rules require lenders to wait at least 120 days after a missed payment before filing a foreclosure complaint in court. During that window, homeowners are actively behind on payments but have not yet entered the formal legal process. This is the period most investors miss entirely, because it does not show up as a public court filing yet.

Once the foreclosure complaint is filed, the court imposes a mandatory three-month waiting period before a sale date can be set. After the court enters judgment, the sheriff's sale must occur within 60 to 120 days. The total elapsed time from first missed payment to completed sale typically runs five to ten months.

The pre-foreclosure phase that matters most for investors spans from that initial 120-day pre-filing period through the court judgment stage. Homeowners in this window are formally in distress, have received official notices, and are emotionally and financially motivated to find an alternative to auction. But they are not yet locked into a sale date that forces a rushed decision.

Where Indiana Pre-Foreclosure Records Are Actually Filed

A critical distinction that trips up Indiana investors: lis pendens notices are filed with the Clerk of the Circuit Court, not the county recorder.

This matters because many investors assume they should monitor county recorder databases the way they would in Texas or Arizona. Indiana's system is different. Lis pendens notices, foreclosure complaints, and court orders are all filed with the county clerk's office. The Indiana Office of Court Services maintains that these are clerk records, not recorder records, and the legal effect is different too.

For investors, this means the data source for pre-foreclosure leads in Indiana is the county circuit court clerk's office, not the assessor's website. The Indiana Foreclosure Prevention Dashboard, maintained by The Polis Center at Indiana University, aggregates statewide foreclosure filing data and is a useful public reference point. But for live, actionable leads, direct access to county circuit court filings produces fresher data than any aggregated dashboard.

Each of Indiana's 92 counties maintains its own circuit court clerk records. The quality and accessibility of those records varies significantly:

Marion County (Indianapolis) — The state's most active foreclosure jurisdiction by volume. The Marion County Clerk's office provides online case search for civil filings including foreclosure complaints. Lis pendens are indexed by party name and property address, making targeted searches practical.

Lake County (Gary, Hammond) — Second-highest volume county. Proximity to Chicago creates a distinct market dynamic, with distressed properties attracting both local investors and cross-state buyers from Illinois.

Allen County (Fort Wayne) — Third-largest market. The Allen County Clerk provides online case records. Steady economic base means less dramatic price swings but consistent pre-foreclosure volume.

St. Joseph County (South Bend) — Home to Notre Dame and a mix of university-adjacent and urban distressed properties. Older housing stock drives consistent renovation plays.

Vanderburgh County (Evansville) — Largest southwestern Indiana market. Less investor competition than Indianapolis or Lake County, creating better ratio of lead quality to outreach volume.

Smaller counties (DeKalb, Steuben, Warrick, and others) often have minimal digital access but lower investor saturation. A motivated investor willing to work county clerk offices directly can find motivated sellers in markets where no other investors are looking.

The 120-Day Pre-Filing Window Most Investors Never See

The period between the first missed payment and the formal foreclosure complaint filing is the most overlooked phase of Indiana pre-foreclosure, and the one where the best deals are often found.

Federal regulations under 12 C.F.R. Section 1024.41 require mortgage servicers to wait at least 120 days before initiating foreclosure after a missed payment. During this period, the homeowner is already in financial distress, already receiving notices from the lender, and already feeling the pressure. But because no lawsuit has been filed yet, no lis pendens appears in court records.

Investors who rely solely on court filings to find leads never see this window. They start paying attention when lis pendens appears, which is typically 120+ days into the homeowner's distress. By then, professional investor calls may already be arriving.

The investors who work this window most effectively use DistressIQ's pre-filing distress signals — tax delinquency records, code violations, prolonged mortgage delinquency patterns — to identify homeowners who are likely already receiving default notices from their servicer, even before the formal legal process begins.

Free Weekly Alerts

See What's Distressed in Your Market

Get free weekly alerts — new distressed properties, motivation scores, and hot neighborhoods in your area. Addresses and contact info available inside DistressIQ.

Free forever · No credit card · Unsubscribe anytime

How to Build an Indiana Pre-Foreclosure Lead Workflow

Step 1: Pull County Court Filings Daily

Set a daily reminder to check new foreclosure complaint filings in your target counties. In Marion County, this means the Clerk's online case search. In smaller counties, a phone call to the circuit court clerk's office each morning is often faster than waiting for third-party data aggregators to update weekly.

The goal: identify new lis pendens filings within 24 to 48 hours of being recorded. Speed matters. The homeowner in Indiana has months of runway, but that does not mean they will wait months to answer calls. First contact within the first 30 days of the lis pendens filing consistently outperforms later outreach, because homeowners have not yet built defensive barriers against investor calls.

Step 2: Cross-Reference Distress Signals

A lis pendens filing alone tells you the homeowner is in formal legal distress. To understand how urgent the situation is and how motivated they are likely to be, cross-reference the filing against:

Tax delinquency records — A homeowner who has also fallen behind on property taxes is facing compounding pressure. These homeowners are typically the most motivated, because tax delinquency can trigger a separate accelerated sale process that leaves them with no equity.

Code violations — Properties with open building code violations signal deferred maintenance and often indicate a landlord or absentee owner who has already walked away from the property. Absentee-owner situations are cleaner to negotiate because there is no occupant to relocate.

Assessor data — Check current assessed value against outstanding loan balance. A property where the loan balance approaches or exceeds assessed value means the homeowner has little to no equity, which paradoxically makes them more likely to accept a below-market offer: they are already underwater and just want the debt resolved.

Step 3: Assess Property Condition Remotely

Before calling, use Street View and aerial imagery to evaluate the property. In Indiana's older urban cores (IndianapolisNear Eastside, Gary, South Bend), deferred maintenance is visible from public imagery and lets you calibrate offer price before the first conversation. In suburban markets (Hamilton County, Carmel, Fishers), condition tends to be better, which means less renovation cost but also less discount from distressed pricing.

This step takes three minutes per lead and prevents the most expensive mistake in pre-foreclosure investing: making an offer on a property you cannot rehab profitably.

Step 4: First Contact Within 48 Hours

Call the homeowner directly, not through a third-party intermediary. The script that works in Indiana pre-foreclosure is not a sales pitch. It is an information exchange:

"I work with homeowners who have received notice about their property and I help them explore options before the sheriff's sale. Have you had a chance to look at what your options are at this point?"

This opener acknowledges the situation without being pushy. It opens a dialogue rather than a negotiation. Indiana homeowners facing judicial foreclosure have usually been dealing with their lender for months before the lawsuit was filed. They have already been through loss mitigation discussions, payment plans that did not hold, and increasingly formal notices. They are not surprised to receive a call. They may be relieved to receive one from someone who is not their lender.

Step 5: Follow-Up Sequence for Mid-Funnel Leads

Not every pre-foreclosure homeowner is ready to sell in week one. Build a four-touch follow-up sequence:

Touch 1 (Day 1): Initial call. Voicemail if no answer. Leave a callback number and name, nothing more.

Touch 2 (Day 7): Second call. If no answer, send a text with a simple message: "Hi [Name], I reached out about your property on [street]. I work with homeowners in situations like this and I may be able to help. Happy to talk whenever works for you."

Touch 3 (Day 21): Letter to the property address. A handwritten envelope outperforms a business envelope in response rates. Include a simple one-page description of what you do and a phone number.

Touch 4 (Day 45): Final call. By this point, the court proceedings are progressing and the homeowner is closer to a sale date. The urgency is real, and they know it. This call often converts more than the first three combined.

Why Most Indiana Pre-Foreclosure Strategies Underperform

Relying on Sheriff Sale Lists Instead of Court Filings

The most common mistake: waiting for the sheriff's sale calendar. By the time a property appears on the sheriff's sale list, the homeowner has already been in default for six to twelve months. They have already negotiated with their lender, explored short sale options, and in many cases already left the property. The sheriff sale list is the end of the pre-foreclosure process, not the beginning. Investors who work the sheriff sale list are competing at auction against cash buyers who have done no prior outreach and do not care about condition. That is a different game than pre-foreclosure investing.

Missing the Pre-Filing Window

As noted above, the 120-day federal pre-foreclosure window is the period when homeowners are most open to creative solutions. Investors who only monitor court filings are arriving 120 days late.

Ignoring Secondary Counties

Marion and Lake counties get all the attention. Allen, St. Joseph, Vanderburgh, and the smaller counties often have more motivated sellers per investor contact, because there is less institutional capital competing in those markets. A focused investor working 15 counties in northern Indiana will often close more deals than one blasting leads across all 92 counties without a prioritization system.

Not Understanding Indiana Deficiency Judgment Rules

Indiana allows lenders to pursue deficiency judgments after sheriff's sale if the property sells for less than the outstanding loan balance. This matters for pre-foreclosure negotiations because it gives homeowners an additional incentive to sell before auction: a pre-foreclosure short sale resolves the debt without triggering a potential deficiency claim. Investors who understand this can structure deals that benefit both parties in ways that auction buyers cannot offer.

Indiana Pre-Foreclosure Market Conditions in 2026

Indiana ranked fourth nationally for foreclosure rates in ATTOM Data's most recent quarterly report, with one foreclosure filing for every 976 housing units statewide. That rate represents a 13% year-over-year increase, driven by economic pressures in legacy industrial markets in the northwest corridor and steady volume in the Indianapolis metro.

The median list price for Indiana foreclosure properties sits around $120,000, well below the national median, making Indiana one of the most accessible Midwest markets for new investors seeking cash-flow-positive rental properties. Properties in the $60,000 to $90,000 range in Lake County and Marion County consistently show after-repair values that support $700 to $900 per month in gross rent, supporting a buy-and-hold strategy even with cash purchases at auction or pre-foreclosure.

Hamilton County, north of Indianapolis, presents a different profile: higher property values, lower foreclosure volume, but stronger appreciation potential. Investors seeking renovation plays in higher-end markets focus here. Investors seeking yield and monthly cash flow focus on Lake, Allen, and St. Joseph counties.

Frequently Asked Questions

What is the pre-foreclosure process timeline in Indiana?

Indiana is a judicial foreclosure state, which means the process runs through the court system. After a homeowner misses payments, federal law requires the lender to wait at least 120 days before filing a foreclosure complaint. Once filed, Indiana law requires a three-month court waiting period before a sale date can be set. After court judgment, the sheriff's sale must occur within 60 to 120 days. The full timeline from first missed payment to sheriff's sale typically runs five to ten months, though contested cases or court backlogs can extend it further. This extended timeline gives investors a wider window to reach motivated sellers than faster non-judicial states.

How do I find pre-foreclosure properties in Indiana?

Pre-foreclosure records in Indiana are filed with the Clerk of the Circuit Court in each county, not the county recorder. Monitor the county circuit court clerk's office for new foreclosure complaints and lis pendens filings. In Marion County, this is searchable online through the clerk's case search system. Smaller counties may require direct contact with the clerk's office. For comprehensive statewide coverage, DistressIQ aggregates filings from all 92 Indiana counties into a single searchable feed, updated daily from court sources, with distress signal cross-referencing to help prioritize which leads to contact first.

Is Indiana a judicial or non-judicial foreclosure state?

Indiana is a judicial foreclosure state. The lender must file a lawsuit in circuit or superior court and obtain a judgment before the property can proceed to sheriff's sale. This differs from non-judicial states like Texas or Colorado, where the lender can proceed directly through a trustee without court involvement. Indiana's judicial process adds time to the overall timeline but creates a longer pre-foreclosure window where homeowners are more accessible to investors.

What is lis pendens and how does it work in Indiana?

Lis pendens in Indiana is filed with the Clerk of the Circuit Court pursuant to Indiana Code Section 32-30-11. It provides legal notice that a property is subject to pending litigation, in this case a foreclosure action. Once recorded, it puts subsequent purchasers on notice that their title may be affected by the outcome of the lawsuit. For investors, a recorded lis pendens signals that the homeowner is in formal legal distress with a court-monitored timeline. The lis pendens is indexed by party name and property address, making it searchable in county court records.

Which Indiana counties have the most pre-foreclosure activity?

Marion County (Indianapolis) leads Indiana in pre-foreclosure volume, followed by Lake County (northwest Indiana, near Chicago), Allen County (Fort Wayne), St. Joseph County (South Bend), and Vanderburgh County (Evansville). These five counties account for the majority of statewide filings. However, secondary markets like Delaware, Tippecanoe, and Johnson counties offer lower investor competition per lead, making them attractive for focused investor outreach. A comprehensive Indiana pre-foreclosure strategy should include all 92 counties, not just the major metros.

What is the redemption period after a sheriff's sale in Indiana?

Indiana does not have a post-sale redemption period for the homeowner in most cases. Once the property sells at sheriff's sale, the sale is final. This makes pre-foreclosure purchase particularly valuable in Indiana: the homeowner has a window to sell before auction that disappears permanently once the sheriff's sale occurs. Investors who can reach homeowners during the pre-foreclosure period are offering something the auction market cannot: a voluntary sale with homeowner cooperation, clean title negotiation, and no competition from other bidders at the moment of agreement.

How does DistressIQ track Indiana pre-foreclosure leads?

DistressIQ monitors Indiana circuit court clerk filings across all 92 counties, capturing new lis pendens and foreclosure complaints as they are recorded. Each lead is cross-referenced against tax delinquency records, code violation databases, and assessor data to build a composite urgency score. The platform provides owner contact information, property details, and visual context for each lead. Daily updates mean you are working current filings rather than weekly batches that may miss the optimal contact window in Indiana's months-long pre-foreclosure timeline.

Start Finding Pre-Foreclosure Leads in Indiana

Indiana's judicial foreclosure process rewards patience and preparation. The five-to-ten-month timeline from missed payment to sheriff's sale gives you something fast-timeline states cannot: enough runway to find the right leads, make first contact at the right moment, and negotiate a deal that works for both sides.

The investors who perform best in Indiana treat pre-foreclosure as a workflow, not a list. Daily court filings, cross-referenced distress signals, fast first contact, and consistent follow-up across a four-touch sequence. That process, applied consistently, produces deals in Indiana markets that out-of-state investors flying through on generic national lists never see.

Browse pre-foreclosure leads across all 92 Indiana counties on DistressIQ.

DistressIQ updates Indiana filings daily from county court sources. Urgency scores, owner contact information, assessor-verified property details, and visual context for every lead. Starting at $89 per month for founding members with 30% lifetime discount locked in.

The data behind this article

DistressIQ Monitors These Signals in Real Time

Pre-Foreclosures

NOD + NTS filings

Tax Delinquency

County treasurer records

Code Violations

Municipal inspection filings

Probate Filings

Superior Court records

Every lead is scored 0–100 for seller motivation based on signal type, duration, severity, and stacking. Nationwide coverage — every US county, updated daily.

Ready to find deals in your market?

See Live Distress Signals in Your County

Stop calling dead leads. Every lead in DistressIQ is scored 0–100 for seller motivation, with verified contact info included. Browse the free tier to see what's active in your market right now.

Browse Free Leads — No Credit Card