Foreclosure Leads Mississippi: The Complete Investor's Guide to the Magnolia State Market (2026)

Foreclosure Leads Mississippi: The Complete Investor's Guide to the Magnolia State Market (2026)

TL;DR: Mississippi is one of the fastest foreclosure states in the country. Non-judicial foreclosures run 60-90 days from default notice to auction sale with no post-sale redemption period. That speed is an edge for investors who know how to move. Hinds, DeSoto, Harrison, and Rankin counties generate the most distressed inventory. County records are your primary signal source, and DistressIQ tracks all of them in one place.

Mississippi does not mess around.

While most states give homeowners 180 days, a year, or longer to cure a foreclosure before the sale, Mississippi can close a non-judicial foreclosure in under 90 days. The borrower's default notice goes out, 30 days pass, the sale is published for three weeks, and the property is auctioned. Done.

That speed is exactly why Mississippi foreclosure leads deserve more attention than they get. Investors who know the timeline can get in and out faster here than almost any other state east of the Mississippi. And unlike some fast-process states, Mississippi does not let the former owner redeem the property after the sale, which means the deal you bid on is the deal you keep.

This guide covers everything you need to know about finding and working Mississippi foreclosure leads in 2026.

Why Mississippi Foreclosure Leads Move Faster Than Almost Anywhere Else

Most investors think "fast foreclosure" means "risky" or "problematic." Mississippi flips that assumption.

The Magnolia State's non-judicial foreclosure process exists because most Mississippi deeds of trust include a power-of-sale clause. When the borrower defaults, the trustee can proceed directly to auction without going through a court case first. No judge. No court hearing. No waiting for a docket number. Just the required notices, the publication period, and the sale.

From the first missed payment to the courthouse steps: 60 to 90 days. Compare that to New York (12-18 months), New Jersey (12-24 months), or even nearby Alabama (60-120 days with a mandatory process server). Mississippi is fast, and fast is an investor's friend when you have the deal flow to keep the pipeline moving.

The practical consequence: pre-foreclosure windows in Mississippi are short. You have less time to find motivated sellers who want to avoid the auction, which means your lead sourcing has to be faster and more accurate. If you are still pulling lists manually or waiting for a county website to update, you are already behind.

The Mississippi Foreclosure Timeline: What Actually Happens

Understanding the stages matters because each one is a different signal type in DistressIQ.

Default and Notice of Sale (Days 1-30): After a borrower misses a payment, the lender sends a default notice. Mississippi law requires at least 30 days' notice before the foreclosure sale can be scheduled. During this window, the borrower can still cure the default and stop the foreclosure by paying the delinquent amount plus costs and fees. This is your prime intervention window.

Publication and Posting (Weeks 2-4): Before the sale, the trustee must publish a notice in a newspaper of general circulation in the county where the property is located and post it at the courthouse door. This has to run for three consecutive weeks.

Investors who monitor public notices can catch properties at this stage.

Investors who monitor public notices can catch properties at this stage.

Foreclosure Auction (Day 60-90+): The property is sold at public auction to the highest bidder. Payment is required in cash or cashier's check at the time of sale. The auction takes place in the county where the property sits, typically at the normal location for sheriff's sales.

No Redemption Period: This is the part that matters most. After the sale, the borrower has no right to redeem the property in Mississippi. In states with redemption periods, the winning bidder at the auction can wait months not knowing if they will actually own the property. In Mississippi, what you bid is what you own. The title transfers immediately upon the trustee's deed being recorded.

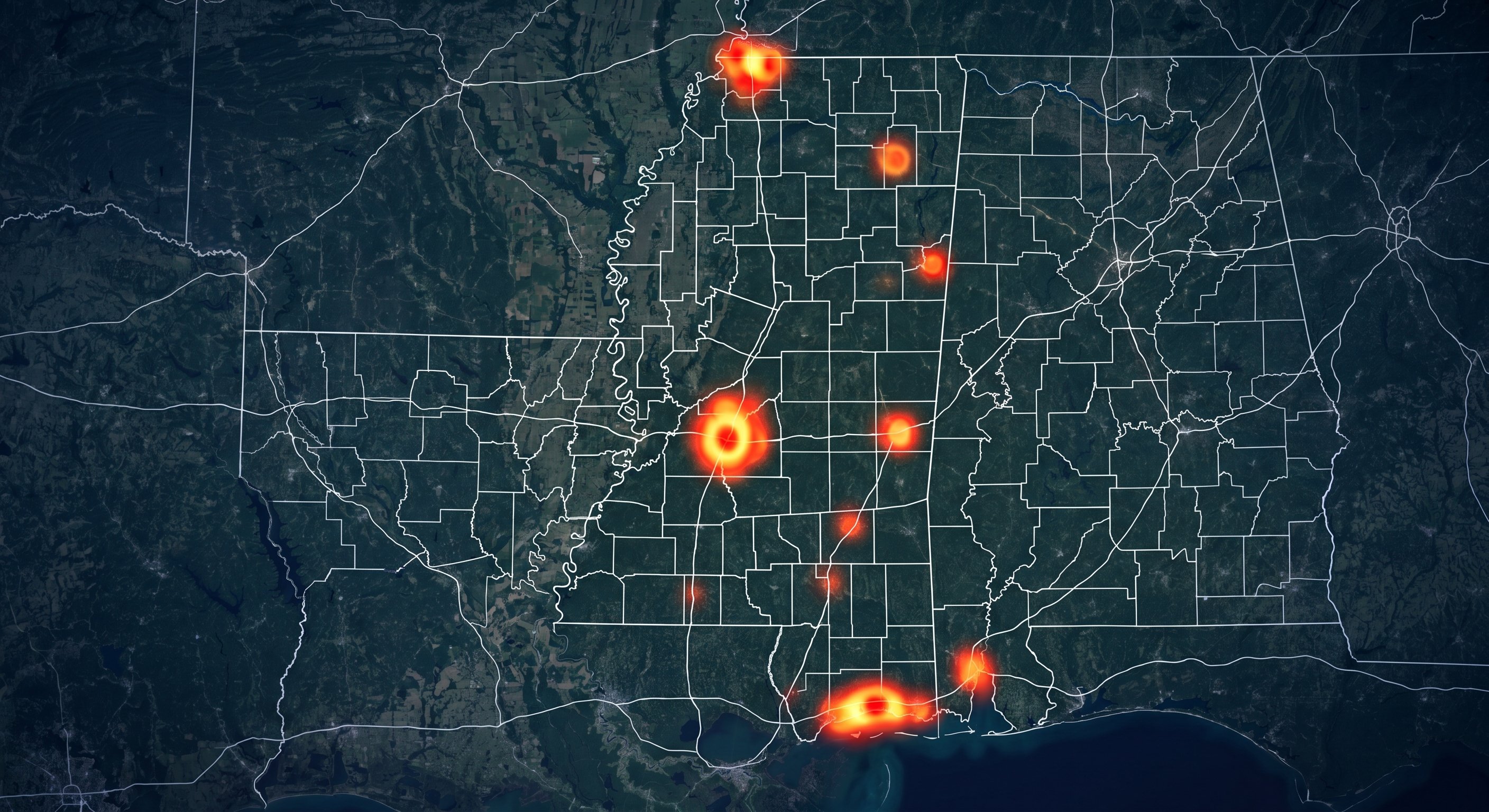

Where to Find Mississippi Foreclosure Leads: Counties That Matter

Mississippi's population is concentrated in a handful of metros, and foreclosure volume follows.

Hinds County (Jackson): The capital city and largest metro in Mississippi. Jackson's housing stock includes a mix of older historic homes, post-war suburbs, and some higher-vacancy areas that attract investors looking for value-add deals. Hinds County chancery court filings are public record.

DeSoto County (Hernando): This is the Mississippi market most Memphis-area investors already know. DeSoto County is the fastest-growing county in the state, directly across the Tennessee border from Memphis. Suburban expansion from Memphis has driven property values up while still keeping entries more affordable than the Memphis metro average. Foreclosures here tend to be primary residence defaults rather than investment property liquidations.

Harrison County (Gulfport/Biloxi): The Gulf Coast market has unique dynamics driven by tourism, casinos, and seasonal housing. Distressed properties here often relate to short-term rental operators, hurricane damage, or investor portfolio corrections rather than pure owner-occupant distress.

Rankin County (Brandon): Suburban Jackson, one of the more affluent Mississippi counties. Rankin County foreclosures tend to be higher-value homes with larger equity positions, which means bigger discounts when they do come to market.

Jackson County (Pascagoula): Eastern Gulf Coast, less populated but with some industrial-related housing distress.

Beyond these, scattered foreclosures occur in Lee County (Tupelo), Lafayette County (Oxford), and Forrest County (Hattiesburg), but volume is lower.

Free Weekly Alerts

See What's Distressed in Your Market

Get free weekly alerts — new distressed properties, motivation scores, and hot neighborhoods in your area. Addresses and contact info available inside DistressIQ.

Free forever · No credit card · Unsubscribe anytime

The Pre-Foreclosure Window: Your Best Opportunity in Mississippi

Because the auction happens fast, the pre-foreclosure stage is compressed. In states with 18-month timelines, you have time to cold-call and mail. In Mississippi, once the notice of default goes out, you have 30 days before the sale is scheduled and another three weeks of publication before the auction.

The actionable window for direct outreach to the borrower is sometimes as short as 45-60 days total.

That means your lead sourcing has to catch properties before or immediately after the default notice, not weeks later.

That means your lead sourcing has to catch properties before or immediately after the default notice, not weeks later.

DistressIQ tracks lis pendens filings and pre-foreclosure signals across Mississippi's county systems, updated daily. Instead of checking five county websites manually, you see every active pre-foreclosure signal in the state ranked by motivation score, with contact information available on demand.

What Makes Mississippi Different: The Legal Details That Actually Matter

Mississippi operates under a deed of trust system rather than a mortgage system. When a borrower finances a home in Mississippi, they almost always sign a deed of trust, which includes the power-of-sale clause that enables non-judicial foreclosure. This is why non-judicial is the dominant process: it is faster, cheaper, and does not require court involvement.

Deficiency judgments: Mississippi allows lenders to pursue deficiency judgments after a foreclosure sale, which is the difference between what the property sold for at auction and what the borrower still owed on the loan. However, lenders must initiate deficiency proceedings within one year of the sale. This creates a legal timeline that knowledgeable borrowers and their attorneys track, but it does not directly affect investors buying at the auction.

Lis pendens: In judicial foreclosures (used when no power-of-sale clause exists), the lender files a lis pendens with the county Chancery Clerk. A lis pendens is a recorded document that puts the public on notice that a lawsuit affecting the property's title is pending. Mississippi Code Title 11, Chapter 47 governs how lis pendens is recorded and indexed. Deeds.com maintains county-specific forms for DeSoto, Hinds, and Rankin counties.

Post-sale tenant rights: If the property has tenants, the federal Protecting Tenants at Foreclosure Act (PTFA) requires 90 days' notice before a new owner can evict. Investors who win at auction need to factor that into possession timelines.

Mississippi Investment Market: What the Data Actually Shows

Mississippi investors bought 24.2% of all homes sold in Q4 2025 at a 27.5% discount to what traditional homeowners paid. Private landlords controlled 73% of investor-held single-family homes in the state, with institutional operators holding just 0.7%. This is a market built on small-scale operators, not Wall Street portfolios.

The Gulf Coast and the I-55 corridor running north from New Orleans through Brookhaven and McComb represent underserved markets where population has grown without a corresponding increase in housing supply. Land costs remain low enough that value-add rehabs still pencil out in these areas.

For fix-and-flip, investors report 15-25% profit margins on total project cost in stronger submarkets within Jackson, the Gulf Coast, and growing DeSoto County suburbs. BRRRR strategies work well in more rural markets where entry costs are low and rents cover debt service.

The bottom line: Mississippi is not a market where you slap a coat of paint on a house and flip it for 60% above purchase. It is a market where you buy right, add the right improvements, and hold or sell with realistic margins. The investors who are winning in Mississippi are doing it because they have the deal flow to be selective, not because they are finding magical discounts.

How to Find Mississippi Foreclosure Leads Today

Manual research is possible but slow. Each county courthouse has its own system for publishing lis pendens and foreclosure notices. The Harrison County Chancery Clerk handles Gulf Coast filings. The DeSoto County Chancery Clerk covers the Memphis suburbs. Hinds County covers Jackson. You are looking at newspaper publication requirements, courthouse door postings, and inconsistent online availability.

The smarter play is working from a platform that pulls from all of these sources daily.

DistressIQ tracks foreclosure signals across every Mississippi county, updated from county-direct records. You see pre-foreclosure leads (properties where a lis pendens has been filed or a notice of default has been recorded), code violation properties, tax delinquent properties, and properties with multiple stacked distress signals. Every lead is scored by motivation so you know which ones to contact first.

See Mississippi foreclosure leads scored by motivation — browse distressed properties in Mississippi free on DistressIQ.

No manual county-by-county searching. No waiting for newspaper publication cycles. Just the data, updated daily, ranked and ready to work.

Frequently Asked Questions

How long does it take to foreclose on a property in Mississippi?

Non-judicial foreclosures in Mississippi typically take 60 to 90 days from the initial default notice to the auction sale. This is one of the faster foreclosure timelines in the country. The process moves faster when the deed of trust contains a power-of-sale clause and the required 30-day notice and three-week publication period are met without delays.

Does Mississippi have a redemption period after foreclosure?

No. Mississippi does not have a post-sale right of redemption for non-judicial foreclosures. Once the property is sold at auction, the winning bidder receives the deed immediately upon recording. This eliminates the uncertainty that comes with redemption periods in other states, where months can pass before the winning bidder actually owns the property.

Can lenders pursue deficiency judgments in Mississippi?

Yes. Mississippi allows lenders to pursue deficiency judgments after a foreclosure sale, representing the difference between the auction price and the outstanding loan balance. Lenders must initiate deficiency proceedings within one year of the sale under Mississippi law. For investors, this does not directly affect auction purchases, but it does factor into the calculus of borrowers who might otherwise try to negotiate a pre-foreclosure short sale.

Which Mississippi counties have the most foreclosure activity?

Hinds County (Jackson), DeSoto County (Hernando), Harrison County (Gulfport/Biloxi), and Rankin County (Brandon) generate the most foreclosure volume. DeSoto County is particularly active due to its proximity to Memphis. Gulf Coast counties see periodic surges tied to tourism economy fluctuations and hurricane-related distress.

What is the difference between a judicial and non-judicial foreclosure in Mississippi?

Most Mississippi foreclosures are non-judicial, enabled by the power-of-sale clause in the deed of trust. The trustee can proceed directly to auction without court involvement. Judicial foreclosures are used only when the mortgage instrument does not contain a power-of-sale clause. In judicial cases, the lender files a complaint with the Chancery Court and a lis pendens is recorded with the county clerk.

The data behind this article

DistressIQ Monitors These Signals in Real Time

Pre-Foreclosures

NOD + NTS filings

Tax Delinquency

County treasurer records

Code Violations

Municipal inspection filings

Probate Filings

Superior Court records

Every lead is scored 0–100 for seller motivation based on signal type, duration, severity, and stacking. Nationwide coverage — every US county, updated daily.

Ready to find deals in your market?

See Live Distress Signals in Mississippi

Stop calling dead leads. Every lead in DistressIQ is scored 0–100 for seller motivation, with verified contact info included. Browse the free tier to see what's active in your market right now.

Browse Free Leads — No Credit Card