Foreclosure Leads Kentucky: What Smart Investors Need to Know in 2026

Foreclosure Leads Kentucky: What Smart Investors Need to Know in 2026

TL;DR: Kentucky's judicial foreclosure process runs 5-12 months from first missed payment to auction, giving investors a longer window to find and work pre-foreclosure leads than most states. The key difference: every foreclosure goes through circuit court, and the minimum bid at the commissioner's sale is two-thirds of the appraised value. Jefferson County (Louisville) holds commissioner sales every other Tuesday. Before you bid, understand the 1-year redemption period that can undo your purchase.

The Kentucky Foreclosure Process Is Different — and That Difference Is an Investor Advantage

Most states use non-judicial foreclosure, which means the bank can sell your house at auction without ever stepping into a courtroom. Kentucky doesn't work that way. Every single foreclosure in the Commonwealth runs through circuit court. The lender files a complaint, the borrower gets 20 days to answer, a judge signs off on the judgment, and only then can the property go to sale.

That's a 5-12 month process from the first missed payment to the auction gavel dropping.

For real estate investors hunting foreclosure leads in Kentucky, that timeline is not a obstacle. It's a pipeline. The longer the process takes, the more time you have to find the distressed homeowner, make contact, and structure a deal before the property hits the commissioner sale. Most investors who lose deals in Kentucky aren't losing to better offers — they're losing because they didn't know the property was available until it was already auctioned off.

The investors who consistently win in Louisville, Lexington, and across Kentucky's secondary markets are the ones who monitor court filings directly. That's where the signal lives.

How Kentucky's Judicial Foreclosure Actually Works

Understanding the stages matters because each stage represents a different type of lead opportunity.

Stage 1 — Missed payment (Day 1): The homeowner falls behind. The servicer begins outreach. Nothing is public yet. This is the quietest stage and the hardest to track.

Stage 2 — Lis pendens filed (Month 2-3): Once the lender files the foreclosure complaint in circuit court, a lis pendens goes on the property record. This is the public signal that a foreclosure is in motion. In Kentucky, the borrower has 20 days to respond. If they don't, the lender seeks a default judgment.

Stage 3 — Court judgment (Month 4-8): The judge signs the order of foreclosure. The property is now legally committed to sale, but the sale date hasn't been set yet. This is the most actionable window — the homeowner knows the house is going, they're likely dealing with the emotional weight of the process, and motivated seller conversations can happen before the auction date is published.

Stage 4 — Appraisal and notice of sale (before auction): Kentucky law requires two appraisers to perform a drive-by inspection before the sale. The opening bid starts at two-thirds of the appraised value. The sale is posted at the property and published in the local newspaper for three consecutive weeks before the auction.

Stage 5 — Commissioner's sale (Month 5-12): The auction happens. In Jefferson County (Louisville), the commissioner's sale runs every other Tuesday. In Fayette County (Lexington), sale notices appear in the Lexington Herald-Leader, typically in the Friday classifieds. The winning bidder gets the property, subject to one significant caveat: the redemption period.

The Redemption Period Is the Detail That Costs Kentucky Investors Deals

Here's the fact about Kentucky foreclosure investing that almost nobody puts in the blog posts: if the property sells at auction for less than two-thirds of its appraised value, the original homeowner has up to one year to buy it back.

One year.

That means you could be the winning bidder at the Jefferson County commissioner sale, wire your deposit, show up to closing, and discover the previous owner just redeemed the property. Your deposit gets returned, but you've spent weeks in due diligence, paid for title search, and have nothing to show for it.

Most investor buyers at Kentucky commissioner sales price in this risk by either bidding above the two-thirds floor or requiring proof that the redemption period has expired before they close. Understanding the redemption calculation is not optional if you're buying at auction.

For investors working pre-foreclosure leads instead of auction purchases, the redemption period creates a different opportunity: motivated homeowners who want to avoid the auction entirely and sell before the commissioner sale date. That conversation, made 60-90 days before the auction, is where the cleanest deals get done.

Free Weekly Alerts

See What's Distressed in Your Market

Get free weekly alerts — new distressed properties, motivation scores, and hot neighborhoods in your area. Addresses and contact info available inside DistressIQ.

Free forever · No credit card · Unsubscribe anytime

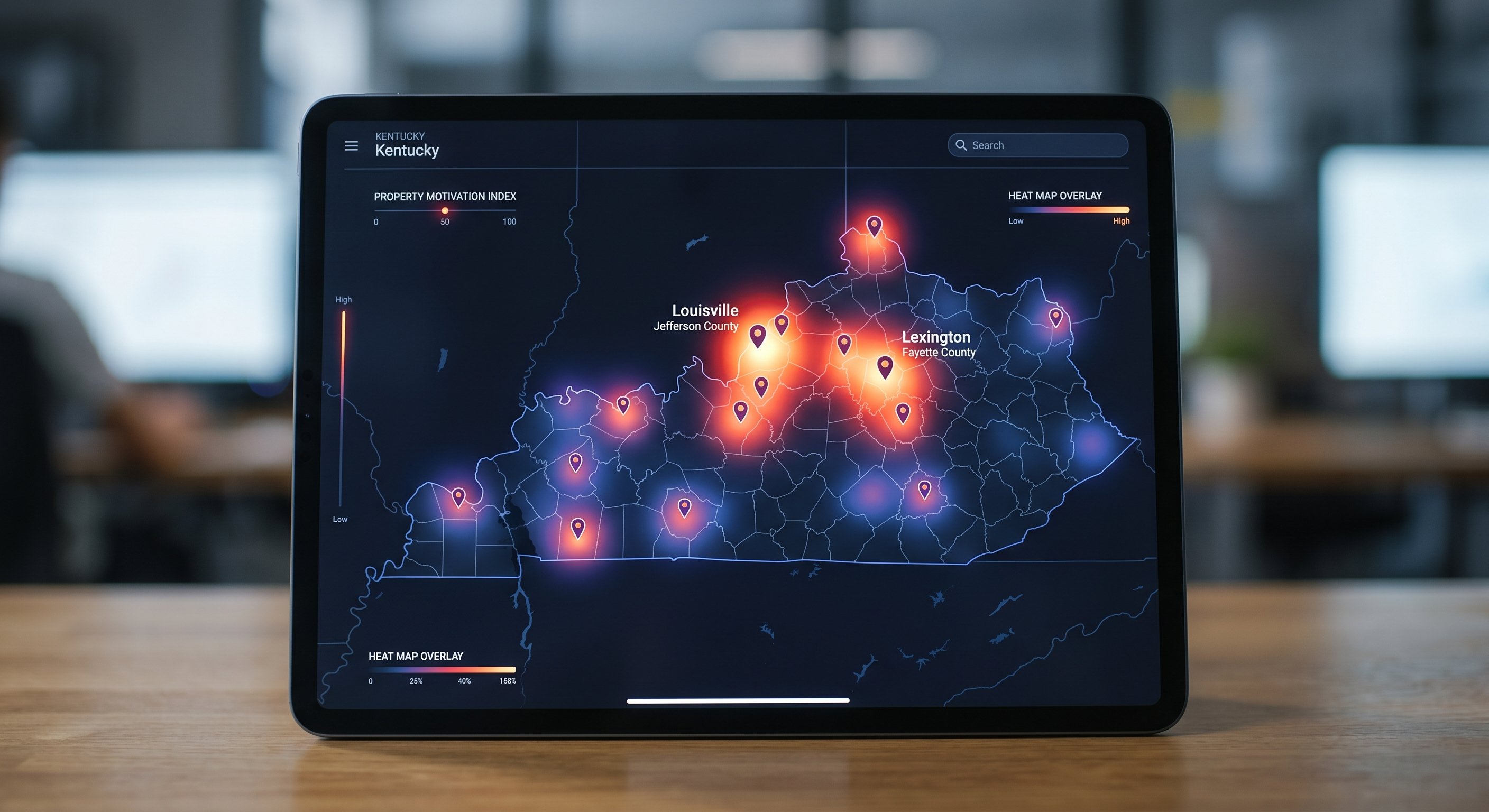

Where to Find Foreclosure Leads in Kentucky's Major Markets

Jefferson County (Louisville)

Louisville is Kentucky's largest city and the epicenter of foreclosure activity in the Commonwealth. The Jefferson County Circuit Court Commissioner holds sales every other Tuesday at the courthouse downtown. The upcoming sales are publicly listed on the Jefferson County government website, and the listings include the property address, the opening bid, and the case number.

The foreclosure activity in Jefferson County is concentrated in specific ZIP codes. As of early 2026, ZIP codes 40215, 40211, 40210, and 40219 show the highest concentration of auction properties, with median estimated values ranging from $65,000 to $250,000. These neighborhoods have older housing stock, which means more distressed properties at lower entry prices — exactly the buy box most fix-and-flip investors are targeting.

Jefferson County also runs an annual delinquent property tax sale. The 2024 sale was held July 18, 2025, at Metro Hall. Third-party purchasers at these sales receive a certificate of delinquency representing a lien on the property. Interest accrues at 12% per year on the unpaid balance. If the homeowner doesn't redeem within one year, the certificate holder can initiate foreclosure.

Fayette County (Lexington)

Lexington's investor concentration is second only to Jefferson County in the state, with 19,749 investor-owned single-family properties as of Q4 2025. The Fayette County commissioner sale follows similar rules to Jefferson County: notices are published in the Lexington Herald-Leader not less than seven days and not more than 21 days before the sale. The sale is typically held at the county courthouse.

Fayette County's property tax sale is also held annually, with the 2025 auction conducted on July 18. Bidders need to register with the Kentucky Department of Revenue at least 60 days in advance if planning to purchase more than $10,000 in certificates of delinquency.

Secondary Markets Worth Watching

Kentucky's highest investor ownership rates are actually found in rural counties, not its major metros. Jackson County leads the state with 47.1% investor ownership rate, followed by McCreary at 46.1% and Leslie at 43.1%. These markets have lower entry costs and lower competition from institutional buyers, but the exit strategies are different — fewer retail buyers, longer days on market, and more依赖 local cash buyers.

For investors working remotely or building a statewide portfolio, combining Jefferson and Fayette county pre-foreclosure leads with rural county tax delinquent properties creates a layered sourcing strategy that covers every price point and exit timeline.

The Distress Signal That Predicts Kentucky Foreclosure Leads

Lis pendens filings are the most reliable leading indicator of foreclosure leads in Kentucky. Unlike some states where pre-foreclosure data is fragmented across multiple county systems, Kentucky's judicial process creates a unified public record. When a lender files a foreclosure complaint, that filing goes on the property's title record and becomes discoverable through the county clerk's office.

For investors, monitoring lis pendens filings in Jefferson and Fayette counties gives you a rolling pipeline of properties that are 3-8 months away from auction. The homeowner is already in distress, they may not know the auction date yet, and a motivated seller conversation right now has a better chance of producing an off-market deal than reaching out after the sale.

Beyond lis pendens, tax delinquency is a parallel signal that tracks alongside foreclosure in Kentucky. Homeowners who fall behind on their mortgage often fall behind on property taxes too. A property with both a lis pendens and a delinquent tax bill is almost certainly a motivated seller with limited options.

How to Work Kentucky Foreclosure Leads Without Going to Every Auction

The investors who build sustainable Kentucky foreclosure businesses aren't showing up to every commissioner sale hoping to get a deal. They're working backwards from the court filing to the motivated seller.

The playbook that works in Kentucky:

Step 1 — Pull the lis pendens list weekly. Both Jefferson County Circuit Court and Fayette County Circuit Court maintain public records of filed foreclosure complaints. This is a weekly monitoring job, not a one-time search.

Step 2 — Cross-reference with property characteristics. A lis pendens on a property with code violations, outstanding liens, and a distressed exterior tells a different story than a lis pendens on a clean single-family home. Filter for the properties where the owner's motivation to sell is highest.

Step 3 — Make contact before the redemption period expires. If the property went to sale and sold below two-thirds of appraised value, the redemption clock is ticking. A fast conversation with the former owner before the one-year window closes may surface a tenant or family member who needs relocation help.

Step 4 — Track the auction results. After every Jefferson County Tuesday sale, review which properties sold, which didn't meet reserve, and which had redemption activity. This builds your market intelligence for the next cycle.

The investors who do this consistently build relationships with the circuit court commissioners' offices, monitor the newspaper listings before they're posted online, and have conversations with distressed homeowners while they're still deciding whether to fight the foreclosure or accept it.

Why Data Freshness Changes the Math on Kentucky Foreclosure Leads

Here's the problem with most approaches to finding Kentucky foreclosure leads: by the time a lead appears on a generic aggregator list, the lis pendens has been on file for weeks. The homeowner has already received 20 days of legal notices. The auction date may already be published in the local paper.

Working from stale data means you're calling a motivated seller who already has three other investors' business cards in their kitchen drawer.

County-direct data — sourced from the actual court filing records and updated daily — gives you a genuine timing advantage. The window between lis pendens filing and the first published notice is narrow, and it's when the homeowner is most emotionally open to a conversation about alternatives.

See distressed properties across Kentucky — including pre-foreclosure leads in Jefferson, Fayette, and every other county — with verified distress signals and motivation scores at DistressIQ. Browse free to see the current pipeline.

Frequently Asked Questions

How long does the foreclosure process take in Kentucky?

Kentucky's judicial foreclosure process typically takes 5-12 months from the first missed payment to the auction sale. The timeline depends on whether the borrower contests the case, court scheduling backlogs, and how quickly the lender moves through the required legal steps. After the court enters judgment, the property must be appraised before the sale can be scheduled.

Is Kentucky a judicial or non-judicial foreclosure state?

Kentucky requires judicial foreclosure. The lender must file a lawsuit in circuit court and obtain a court order before the property can be sold at auction. This creates a longer, more transparent process than non-judicial states, but it also means every foreclosure is a matter of public record once the complaint is filed.

What is the minimum bid at a Kentucky foreclosure auction?

In Kentucky, the opening bid at a commissioner's sale must be at least two-thirds of the appraised value of the property. If the property sells for less than two-thirds, the original homeowner has up to one year to redeem it by paying the full auction price plus interest.

How often does Jefferson County hold foreclosure auctions?

Jefferson County (Louisville) holds commissioner sales every other Tuesday. The sale notices are posted at the property and advertised in the local newspaper for three consecutive weeks before the auction. The current sale listings can be found on the Jefferson County government website.

Can an investor buy a Kentucky foreclosure property before the auction?

Yes. Many of the cleanest deals in Kentucky's foreclosure market happen before the auction date. Investors who monitor lis pendens filings and reach out to distressed homeowners directly can negotiate an off-market sale that avoids the auction process entirely. This is especially valuable given the one-year redemption period that applies to below-two-thirds auction sales.

What is the redemption period for Kentucky foreclosures?

Kentucky law gives the former homeowner one year to redeem a property after it sells at auction for less than two-thirds of its appraised value. If they exercise this right, they must pay the full auction price plus interest. Investors bidding at or above the two-thirds floor face a shorter redemption risk.

The data behind this article

DistressIQ Monitors These Signals in Real Time

Pre-Foreclosures

NOD + NTS filings

Tax Delinquency

County treasurer records

Code Violations

Municipal inspection filings

Probate Filings

Superior Court records

Every lead is scored 0–100 for seller motivation based on signal type, duration, severity, and stacking. Nationwide coverage — every US county, updated daily.

Ready to find deals in your market?

See Live Distress Signals in Kentucky

Stop calling dead leads. Every lead in DistressIQ is scored 0–100 for seller motivation, with verified contact info included. Browse the free tier to see what's active in your market right now.

Browse Free Leads — No Credit Card