Foreclosure Leads Idaho: What Smart Investors Need to Know About the Gem State Market

Foreclosure Leads Idaho: What Smart Investors Need to Know About the Gem State Market

TL;DR: Idaho runs a non-judicial foreclosure process with a 120-day minimum between Notice of Default and trustee sale. Unlike Oregon, Minnesota, or Illinois, Idaho offers no post-sale redemption period once the auction is final. Foreclosure volume is extremely low — roughly 267 statewide filings in Q3 2024 — but Ada County generates the majority of deals, and homes there trade at a median price above $540,000. Less competition per lead means stronger margins for investors who know where to look.

Most real estate investors write off Idaho as a foreclosure market. The numbers look thin. Roughly 267 foreclosure filings across the entire state in a single quarter. Compare that to Florida or Texas, where a single metro area generates that many in a week.

But thin volume is not the same as thin opportunity. Idaho's foreclosure market has structural advantages that sophisticated investors have quietly been exploiting for years: a fast non-judicial process, no post-sale redemption period, and a population so concentrated in the Boise metro that almost every actionable foreclosure lead in the state flows through a handful of counties.

How Foreclosure Works in Idaho: The Non-Judicial Framework

Idaho uses a non-judicial foreclosure process, which means lenders do not need to go through the court system to take possession of a property. Instead, the process operates through the deed of trust recorded with the county recorder. This is faster, cheaper for the lender, and more predictable for investors who understand the timeline.

The process follows a specific sequence under Idaho Code 45-1506:

Notice of Default: After roughly 90 days of missed payments, the lender records a Notice of Default with the county recorder and sends a copy to the borrower. This officially starts the clock.

Reinstatement Window: The borrower has the legal right to reinstate the loan and stop the foreclosure by paying the full default amount plus costs, up until 11 days before the scheduled trustee sale.

Notice of Sale: At least 120 days after the Notice of Default records, the trustee mails a Notice of Sale to the borrower and publishes it in a local newspaper once weekly for four consecutive weeks. The final publication must run at least 30 days before the sale date.

Trustee Sale (Auction): The property goes to the highest bidder at a public auction. The lender typically makes a credit bid up to the total amount owed. The winning bidder takes possession 10 days after the sale.

The entire process typically concludes in 150 to 180 days from the first missed payment. Nationally, states like New York average over 900 days and New Jersey routinely stretches past 18 months. Idaho is one of the fastest Western states for a completed foreclosure.

The Rule That Makes Idaho Pre-Foreclosure Leads More Valuable

Here is the detail that separates Idaho from its neighbors and catches most out-of-state investors flat-footed.

Idaho has no post-sale redemption period for non-judicial foreclosures. Once the trustee calls the auction final, the sale is final. The borrower cannot reclaim the property by paying the full debt after the sale. This is codified in Idaho Code 45-1508.

Compare that to Oregon, where borrowers can redeem within 180 days after the sale. Or Minnesota, where the redemption window stretches to 12 months. In those states, an investor who wins a trustee sale might have to wait up to a year before taking possession.

In Idaho, once the sale clears, the investor takes possession 10 days later. No waiting. No uncertainty.

For investors, this means one thing clearly: the money is made or lost in the pre-foreclosure window, before the auction. That is exactly where DistressIQ focuses its data. Every Notice of Default, every pre-foreclosure filing, every signal that shows a property approaching the auction block is tracked and scored daily from county sources. The borrowers who are still in their reinstatement window are the ones who can still negotiate. They have equity. They may be motivated by a life event rather than pure financial collapse. They are exactly the motivated sellers experienced investors want to find.

Where Foreclosure Leads Cluster in Idaho

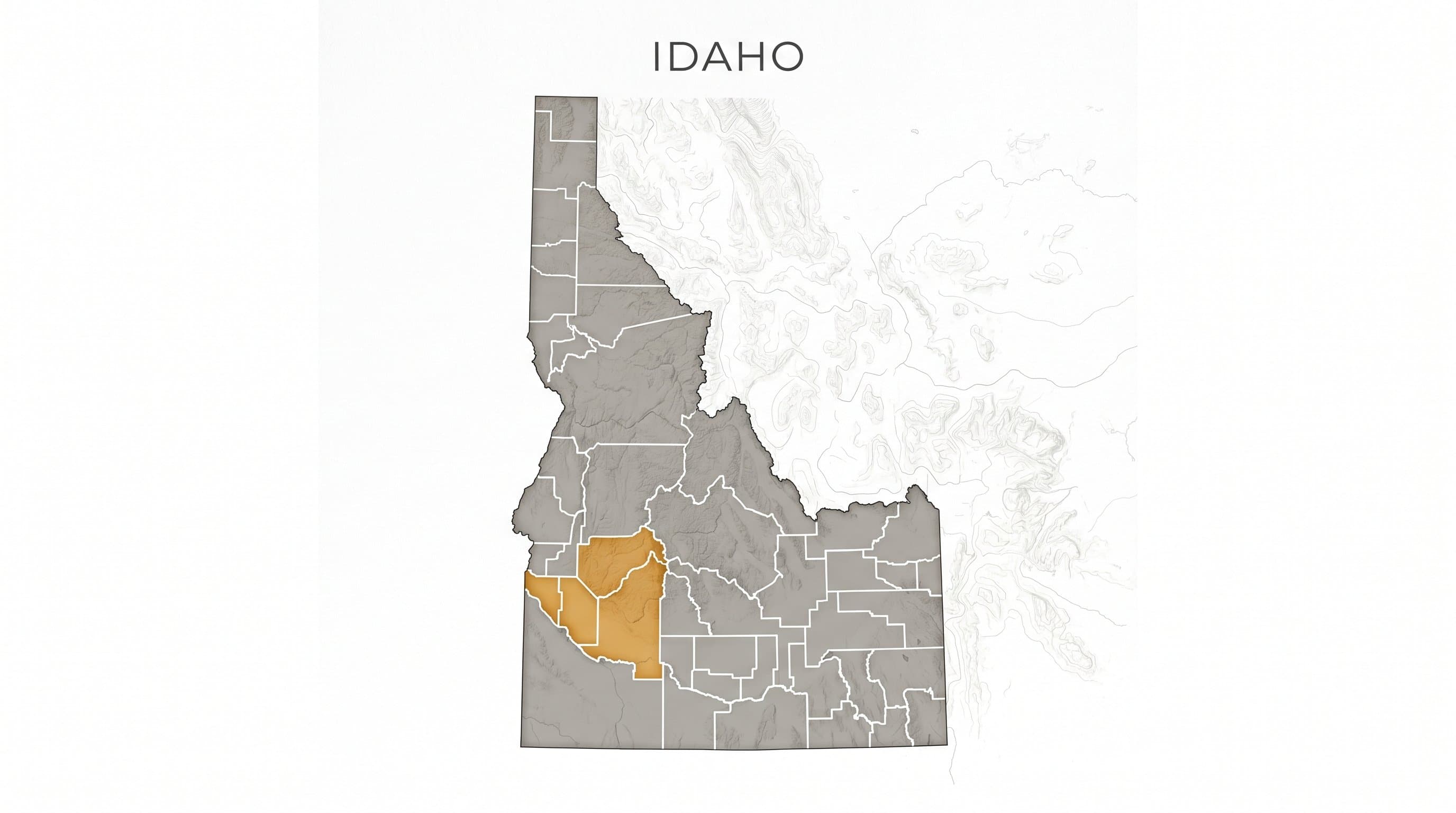

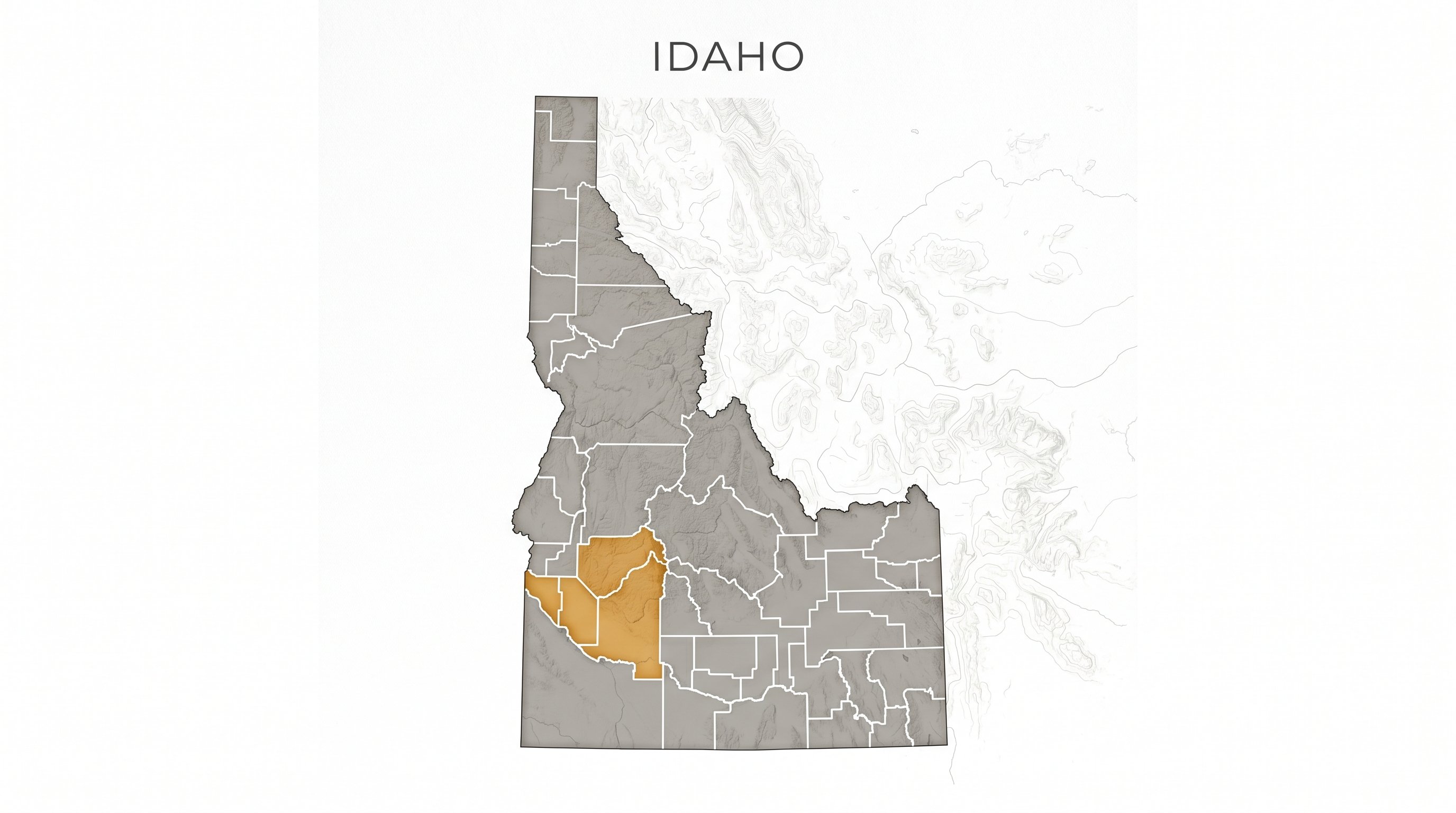

Idaho has 44 counties, but the foreclosure market is essentially a three-county story.

Ada County is the center of gravity. Home to Boise, Meridian, Eagle, and Kuna, Ada County accounts for the largest share of Idaho's foreclosure activity. The Boise metro's growth over the past decade — driven by relocations from California, Washington, and Oregon — created a market where homes routinely sell in 34 to 55 days. That liquidity means borrowers who get into trouble often have equity to work with, making pre-foreclosure resolutions more common and auction skips less frequent. But when a Notice of Default does post in Ada County, it tends to attract attention.

Canyon County is Ada's neighbor to the west, centered around Nampa and Caldwell. More affordable than Ada, Canyon County draws first-time buyers and investors looking for lower entry points. Foreclosure volume is smaller but active, and competition at the trustee sale level is less intense.

Kootenai County in North Idaho — anchored by Coeur d'Alene and Post Falls — represents a distinct market. Lake-driven recreation demand has pushed median prices up significantly, creating a different risk profile. Foreclosure leads here are fewer but tend to involve higher-value properties.

The rest of Idaho is predominantly rural. The concentration of population in the Treasure Valley means investors working statewide will spend most of their time in Ada and Canyon.

Free Weekly Alerts

See What's Distressed in Your Market

Get free weekly alerts — new distressed properties, motivation scores, and hot neighborhoods in your area. Addresses and contact info available inside DistressIQ.

Free forever · No credit card · Unsubscribe anytime

Idaho's Low Volume Is an Investor Advantage Nobody Is Talking About

267 foreclosure filings statewide in Q3 2024, per ATTOM Data. That is roughly one filing for every 2,842 housing units in the state. Compare that to California's one-in-1,100 or Florida's one-in-840.

Most investors see those numbers and move on. That is the mistake.

When foreclosure volume is high, every motivated seller is fielding calls from 20 other investors the same week the Notice of Default posts. When foreclosure volume is low, the same motivated seller in Idaho might receive two calls all month. The investor who shows up with a fair cash offer and a clean close is not competing against a queue.

Ada County median sale prices above $540,000 (March 2026, Boise Regional REALTORS data) mean even a modest discount at trustee sale pricing represents significant equity. A property that sells at auction at 85% of ARV in Ada County still trades at a meaningful discount to comparables in comparable Western metros.

One more structural factor: as of late 2025, new construction represented 51% of all active listings in the Boise metro, per reporting on Realtor.com data. That means existing distressed homes face less competition from new builds than in faster-growing Sun Belt markets.

Finding and Working Foreclosure Leads in Idaho

County recorder databases are the starting point. Every Notice of Default in Idaho gets recorded with the county recorder's office. Ada County and Canyon County both maintain public search interfaces, though data is typically only as current as the last business day of recording. Investors who rely on county search alone are working with a lag.

Trustee sale lists are another layer. Idaho uses independent trustees who manage the foreclosure process for each lender. Building relationships with the trustee companies active in Ada and Canyon County can surface advance notice of upcoming sales.

DistressIQ aggregates these signals across Idaho's 44 counties, pulling Notice of Default recordings, trustee sale postings, and pre-foreclosure activity into a single ranked view. Each lead is scored by motivation indicators and updated daily from county sources. Investors see which properties are still in the reinstatement window, which are approaching the sale date, and which have a trustee sale scheduled within the next 30 days.

The 120-day minimum Idaho window between Notice of Default and trustee sale is the investor's runway. The most productive phase is the first 60 days after the Notice of Default records. The borrower is aware of the problem, has not yet accepted the outcome, and may be actively seeking a way out. That is the contact window.

Frequently Asked Questions

Q: How long does foreclosure take in Idaho?

Idaho's non-judicial foreclosure process typically takes 150 to 180 days from the first missed payment to the completed trustee sale. Idaho Code 45-1506 requires a minimum of 120 days between the recording of the Notice of Default and the scheduled trustee sale date. This is one of the faster foreclosure timelines in the Western United States. The borrower can reinstate the loan and stop the foreclosure up until 11 days before the sale date.

Q: Does Idaho have a foreclosure redemption period?

No. Idaho does not provide a post-sale redemption period for non-judicial foreclosures. Once the trustee sale is completed and the winning bidder pays in full, the sale is final. The borrower cannot reclaim the property by paying the outstanding debt after the auction. This makes Idaho pre-foreclosure leads more valuable since there is no post-sale redemption risk for the buyer. By contrast, Oregon allows 180 days for redemption, Minnesota up to 12 months, and Illinois can stretch even longer.

Q: What counties in Idaho have the most foreclosure activity?

Ada County, centered on the Boise metro, generates the majority of Idaho's foreclosure filings. Canyon County (Nampa, Caldwell) is the second-most-active county. Kootenai County (Coeur d'Alene) produces a smaller but meaningful volume tied to the higher-value lake market. Most other Idaho counties are predominantly rural with very low filing counts.

Q: Can out-of-state investors buy properties at Idaho trustee sales?

Yes. Idaho trustee sales are public auctions open to any bidder. Investors do not need to be Idaho residents to participate. Winning bidders must pay the full purchase price at the time of the sale or within the timeframe specified in the notice. Title insurance is strongly recommended for any trustee sale purchase due to potential title defects that may not appear in the public record.

Q: What is the average days on market for homes in Ada County, Idaho?

Homes in Ada County sold in a median of 34 to 55 days as of early 2026, according to Boise Regional REALTORS data. This is significantly faster than the national average and reflects the Boise metro's continued demand even as the market normalizes. Fast days-on-market in the broader MLS can mask longer marketing times for distressed properties that are not yet listed publicly.

Q: How does Idaho's foreclosure process compare to neighboring states?

Idaho is faster than most neighbors. Oregon requires trustee sale notice plus a 180-day post-sale redemption period. Washington has a 90-day redemption window. Idaho has no redemption period and completes most non-judicial foreclosures in under six months. For investors, this means faster possession and less uncertainty about closing timelines compared to Pacific Northwest neighbors.

Q: Is Idaho a good state for foreclosure investors?

Idaho presents a compelling combination for the right investor: strong median ARV (Ada County median above $540,000), very low competition per lead due to thin foreclosure volume, fast non-judicial process, and no post-sale redemption risk. The primary constraint is limited deal volume. Investors who can source leads systematically and move quickly during the pre-foreclosure window find Idaho's market rewarding. Those expecting a high volume of distressed inventory may want to pair Idaho with higher-volume states.

The low foreclosure volume in Idaho is not a sign that opportunity is absent. It is a signal that competition is sparse. In a market where the average trustee sale in Ada County involves a handful of registered bidders rather than a crowd, the investor who shows up with verified data, a fast close, and a fair offer has a structural edge that is difficult to replicate in higher-volume markets.

See Idaho foreclosure leads ranked by motivation score, filtered by county, signal type, and days-on-clock. Browse every Ada County and Canyon County pre-foreclosure lead with assessor-verified property details, motivation scoring, and built-in Street View and aerial imagery.

Browse Idaho foreclosure leads on DistressIQ

Data sources: ATTOM Data Solutions (Q3 2024 foreclosure filings, https://www.attomdata.com), Boise Regional REALTORS / Intermountain MLS (March 2026 market data), Idaho Code 45-1506 and 45-1508 (https://legislature.idaho.gov/statutesrules/idstat/Title45/T45CH15/), Idaho Statesman / Realtor.com (2025-2026 Boise market forecast, https://www.idahostatesman.com).

The data behind this article

DistressIQ Monitors These Signals in Real Time

Pre-Foreclosures

NOD + NTS filings

Tax Delinquency

County treasurer records

Code Violations

Municipal inspection filings

Probate Filings

Superior Court records

Every lead is scored 0–100 for seller motivation based on signal type, duration, severity, and stacking. Nationwide coverage — every US county, updated daily.

Ready to find deals in your market?

See Live Distress Signals in Idaho

Stop calling dead leads. Every lead in DistressIQ is scored 0–100 for seller motivation, with verified contact info included. Browse the free tier to see what's active in your market right now.

Browse Free Leads — No Credit Card