Double Close Real Estate: How Simultaneous Closings Work in 2026

Double Close Real Estate: How Simultaneous Closings Work in 2026

TL;DR: A double close in real estate is two separate transactions that happen simultaneously at the same title company. The investor buys the property from the motivated seller, then immediately sells it to the end buyer, using the end buyer's funds to fund the first purchase. This approach lets wholesalers acquire properties without using their own capital or relying on an assignment of contract.

The assignment of contract has been the backbone of real estate wholesaling for decades. Find a motivated seller, get under contract, assign that contract to an end buyer for an assignment fee, collect a check. Simple in theory. But traditional assignment has grown riskier. More states are scrutinizing whether assignment deals constitute brokering without a license. Some end buyers specifically refuse to accept assigned contracts. And in a tight lending environment, cash buyers and institutional investors increasingly want direct title in their name, not a transferred contract.

The double close solves both problems. Two simultaneous transactions at one title company, one right after the other. The seller deals with the investor. The investor deals with the end buyer. Clean title passes directly from seller to end buyer, and the investor walks away with a spread. No license required. No assignment clause required. No risk of the deal falling apart mid-transfer because the end buyer refused to close through an assignment.

How a Double Close Works: Step by Step

A double close is two separate purchases and sales that happen in sequence at the same title company, typically within the same day or across consecutive days. Here is the sequence as it actually unfolds.

Step 1: The investor secures a purchase contract with the motivated seller. The investor negotiates a purchase and sale agreement directly with the seller, typically at a significant discount reflecting the seller's need for speed or the condition of the property. The contract specifies a closing date that gives the investor time to locate an end buyer, usually five to fourteen days out. The investor puts down an earnest money deposit, typically held by the title company.

Step 2: The investor finds an end buyer before the closing date. This is the critical constraint. The double close does not work if the investor cannot secure an end buyer before the scheduled closing. Most investors locate buyers through their existing network, wholesale buyer lists, or real estate investor communities before signing the initial contract. Some investors use a first-look arrangement with their best cash buyers before going to a broader market.

Step 3: Both transactions close at the same title company on the same day. The title company prepares two sets of settlement statements. The first transaction closes: the investor buys from the seller and receives title. The second transaction closes immediately after: the investor sells to the end buyer at a higher price. The end buyer's funds cover the investor's purchase of the first transaction. The investor retains the difference between the two prices as gross profit.

The key mechanic is that the end buyer's funds flow through the title company and cover both transactions. The investor never needs to bring significant capital to the table in a pure cash double close. If the end buyer is getting financing, the investor typically uses a transactional lender or hard money lender to fund the gap between the purchase price and the end buyer's loan amount.

A Real Example: Numbers That Actually Work

A homeowner in a Phoenix suburb needs to sell fast because of a job relocation. According to the Consumer Financial Protection Bureau, most mortgage agreements include a due-on-sale clause giving lenders the right to call a loan due when the property transfers. The property needs about $22,000 in cosmetic repairs. The after-repair value is $285,000. The seller needs to net $198,000 after all closing costs to make the relocation work. The investor agrees to buy at $205,000 with a ten-day close.

The investor markets the property to their buyer network. A fix-and-flip investor in the same market agrees to buy at $245,000 cash, closing in seven days.

At the title company, the two transactions close back-to-back. The seller receives $198,000 net at the first closing. The investor's cost basis is $205,000 purchase price plus $3,200 in closing costs and title insurance for the first transaction, totaling $208,200. The investor sells to the end buyer for $245,000. Closing costs and title insurance for the second transaction run another $3,800. The end buyer's cash covers the investor's full acquisition cost of $208,200 plus the investor's $5,000 assignment-equivalent fee. The investor nets $33,000 gross profit on the double close.

The numbers work because the spread between the purchase price and the end buyer's price covers the investor's closing costs twice, the title company's fees, and still leaves meaningful profit. In a high-volume market like Phoenix, Dallas, or Atlanta, experienced wholesalers running ten to twenty double closes per quarter generate $300,000 to $600,000 in gross revenue from this strategy alone.

What the Title Company Needs to Run a Double Close

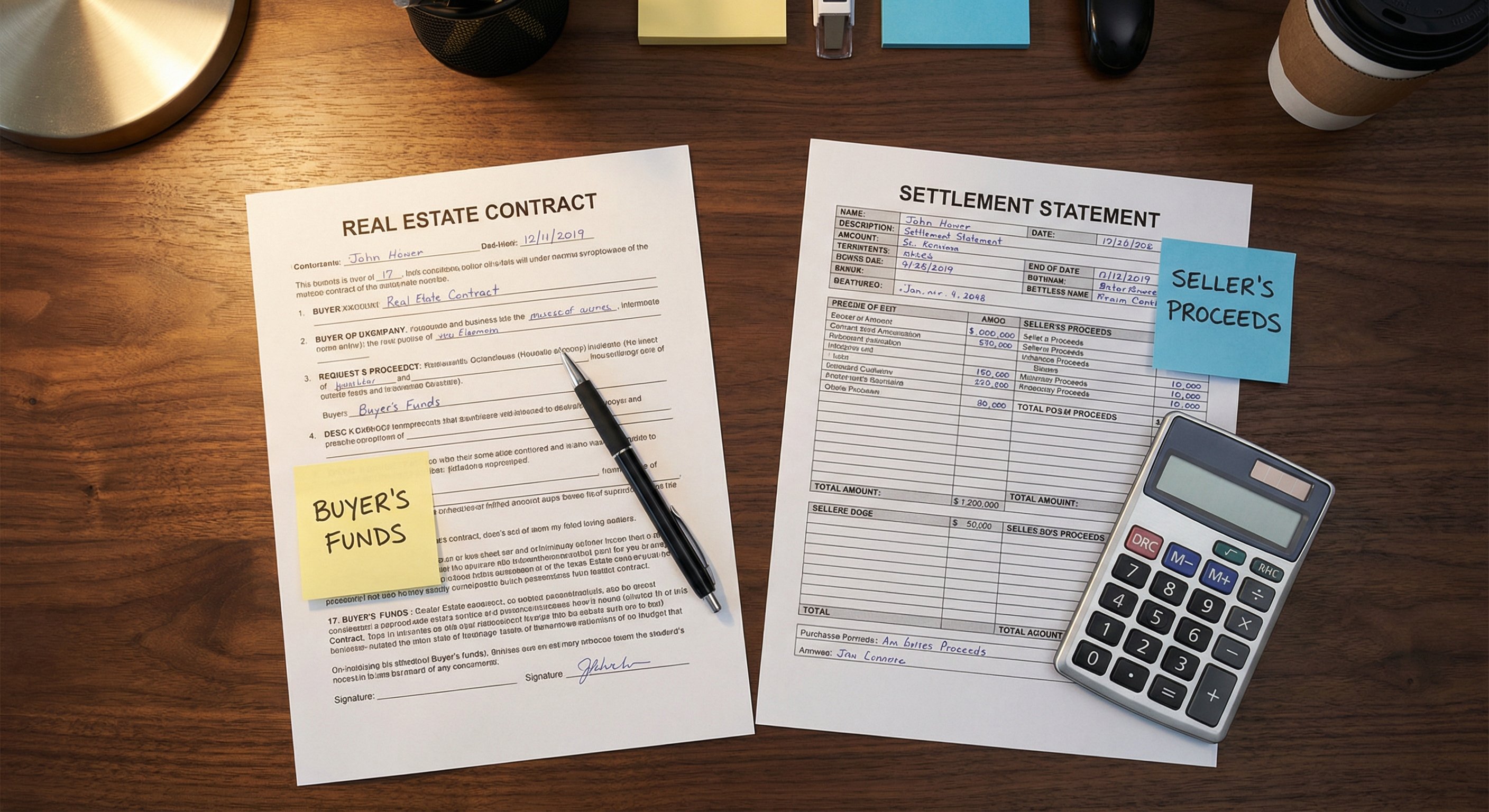

The title company is the operational core of a clean double close. Not every title company is comfortable running simultaneous transactions, and the ones that do not regularly handle wholesale deals can create delays or errors that blow up the timing.

The investor should brief the title company at least three days before closing. They need to provide the purchase and sale agreement for the first transaction, the purchase and sale agreement for the second transaction, the earnest money checks for both deals, and proof of funds or a lender's loan letter for any portion of the end buyer's purchase that involves financing.

The title company will prepare two sets of settlement statements, one for each transaction, itemizing the purchase price, closing costs, title insurance premiums, and any other charges. In most states, the investor needs to appear on both sets of settlement statements as the buyer in the first transaction and the seller in the second.

Some title companies charge a higher title insurance premium on double closes because they insure two separate transactions. Others charge a flat fee plus an additional transaction fee. The investor should get a written estimate of all title and closing costs before scheduling the double close to avoid surprises at the settlement table.

Free Weekly Alerts

See What's Distressed in Your Market

Get free weekly alerts — new distressed properties, motivation scores, and hot neighborhoods in your area. Addresses and contact info available inside DistressIQ.

Free forever · No credit card · Unsubscribe anytime

Exit Strategies and Deal Flow for Double Close Investors

The double close is only as strong as the investor's buyer network. Without a confirmed cash buyer in hand before the initial contract is signed, the investor is carrying the earnest money deposit at risk. Most experienced double close investors maintain an active buyers list of fifty to two hundred verified cash buyers and institutional buyers who regularly purchase wholesale deals.

The most reliable deal flow sources for double close candidates are properties with verified distress signals that create urgency.

A homeowner who is pre-foreclosure needs to close within thirty to sixty days to stop the foreclosure process. A probate heir who wants a clean exit from an inherited property is highly motivated to accept a quick close. A tax-delinquent property owner facing an upcoming sheriff sale needs to close before the auction date.

A homeowner who is pre-foreclosure needs to close within thirty to sixty days to stop the foreclosure process. A probate heir who wants a clean exit from an inherited property is highly motivated to accept a quick close. A tax-delinquent property owner facing an upcoming sheriff sale needs to close before the auction date.

DistressIQ tracks these situations across 3,200-plus counties, flagging properties with verified distress signals and motivation scores that help investors prioritize which leads to pursue. An investor searching for pre-foreclosure leads in Harris County, Texas, can filter for motivated sellers with sheriff sale dates within their buying window and focus their outreach on properties where a double close timeline is realistic.

For investors who prefer a more consistent deal flow without the constant pressure of finding an end buyer before closing, a hybrid approach works well. Use assignment of contract as the primary exit for deals where the end buyer is confirmed and the assignment language is clean. Reserve the double close for situations where the end buyer requires direct title, where state law or local custom makes assignments problematic, or where the spread is large enough to absorb the additional closing costs comfortably.

Key Risks and How to Manage Them

Timing collapse. If the end buyer cannot close on the scheduled date, the first transaction may need to be extended or cancelled. Extending requires renegotiating with the seller, which is difficult when the seller is already at the closing table. The earnest money deposit is at risk if the investor cannot perform. Mitigation: never sign a purchase contract without a confirmed buyer or a very strong verbal commitment backed by a proof-of-funds letter.

Due-on-sale clause. If the property being purchased has an existing mortgage with a due-on-sale clause, the lender can technically call the loan due when the property transfers. Most investors avoid this risk by targeting properties that are either free and clear or where the existing loan is being paid off at closing from proceeds. Properties with existing financing are generally not good double close candidates unless the loan is being paid off at the first closing.

Additional closing costs. Each transaction carries its own title insurance premium, settlement fees, and potentially recording fees.

On a $200,000 property, these costs can run $3,000 to $5,000 per transaction, meaning $6,000 to $10,000 in combined costs. The spread between the purchase price and the end buyer's price must be wide enough to absorb these costs and still leave meaningful profit. A deal that works as an assignment may not work as a double close once the additional costs are factored in.

On a $200,000 property, these costs can run $3,000 to $5,000 per transaction, meaning $6,000 to $10,000 in combined costs. The spread between the purchase price and the end buyer's price must be wide enough to absorb these costs and still leave meaningful profit. A deal that works as an assignment may not work as a double close once the additional costs are factored in.

Licensing requirements. Several states have moved to restrict real estate wholesaling activity if the investor is not licensed. The double close is generally viewed more favorably by regulators than an assignment of contract because the investor takes title and then sells, which mirrors a traditional purchase and sale. However, investors should consult a real estate attorney in their state before relying on the double close as a primary strategy.

Frequently Asked Questions

How long does a double close take?

Most double closes are completed within one to five business days from the initial purchase contract signing to the second closing. Same-day double closes are possible when the end buyer's funds are confirmed and the title company has experience running simultaneous transactions. Transactions involving transactional lenders or hard money typically require three to five days to fund.

Does the seller know about the double close?

In most double close transactions, the seller is unaware that the investor is immediately reselling the property. The seller has agreed to sell at the negotiated price and does not need to know what happens after title transfers. The investor purchases as a principal, not as an agent. Some investors prefer to disclose the strategy upfront, particularly when the seller has an existing relationship with the investor or when disclosure is required under state law.

What happens if the end buyer backs out after the first closing?

If the first closing completes and the end buyer fails to close, the investor is now the owner of the property and must either finance holding costs out of pocket, find a new buyer quickly, or list the property for sale. The earnest money deposit the investor put down with the seller at contract signing is at risk. This scenario is why experienced investors never close the first transaction without a confirmed buyer and a strong proof-of-funds letter in hand.

How is a double close different from an assignment of contract?

In an assignment, the investor transfers their rights under the purchase contract to an end buyer for a fee. The investor never actually takes title. In a double close, the investor takes title at the first closing and then sells that title to the end buyer at the second closing. Assignment is faster and cheaper because there is only one transaction. Double close is more legally defensible in states restricting assignments and allows the investor to work with buyers who require direct title.

Do double closes require all-cash buyers?

Not necessarily, but cash buyers simplify the process significantly. When the end buyer is paying cash, the investor knows the funds will be available at the second closing to cover the first transaction costs. When the end buyer is using financing, the investor typically uses a transactional lender to bridge the gap between the purchase price and the loan amount. Transactional lenders fund quickly but charge premium rates, which eat into the spread.

Finding motivated sellers who will accept the purchase terms that make a double close profitable requires both the right leads and the right buyer network. DistressIQ provides the first half of that equation across every US county, with verified distress signals that identify motivated sellers before they list publicly. Investors who combine strong buyer networks with quality deal flow consistently outperform those relying on generic marketing lists or cold outreach.

See distressed property leads in your market on DistressIQ. Browse free, no credit card required.

DistressIQ tracks distressed property signals across every US county. Learn more at DistressIQ.

The data behind this article

DistressIQ Monitors These Signals in Real Time

Pre-Foreclosures

NOD + NTS filings

Tax Delinquency

County treasurer records

Code Violations

Municipal inspection filings

Probate Filings

Superior Court records

Every lead is scored 0–100 for seller motivation based on signal type, duration, severity, and stacking. Nationwide coverage — every US county, updated daily.

Ready to find deals in your market?

See Live Distress Signals in Your County

Stop calling dead leads. Every lead in DistressIQ is scored 0–100 for seller motivation, with verified contact info included. Browse the free tier to see what's active in your market right now.

Browse Free Leads — No Credit Card